Many economists think the RBA Board will cut the cash rate this month. With commodity prices projected to be weakening, financial markets suggest a rate cut is likely. Mind you, many practitioners suggested a cut was coming last month too, and it didn’t materialise.

The nine experts on the Shadow Board, a mix of practitioners and academics, give their views on what the interest rate should be, rather than predicting actual RBA Board behaviour. The novel construction of the Shadow Board permits analysis of the individual opinions both across a range of interest rate settings and through time.

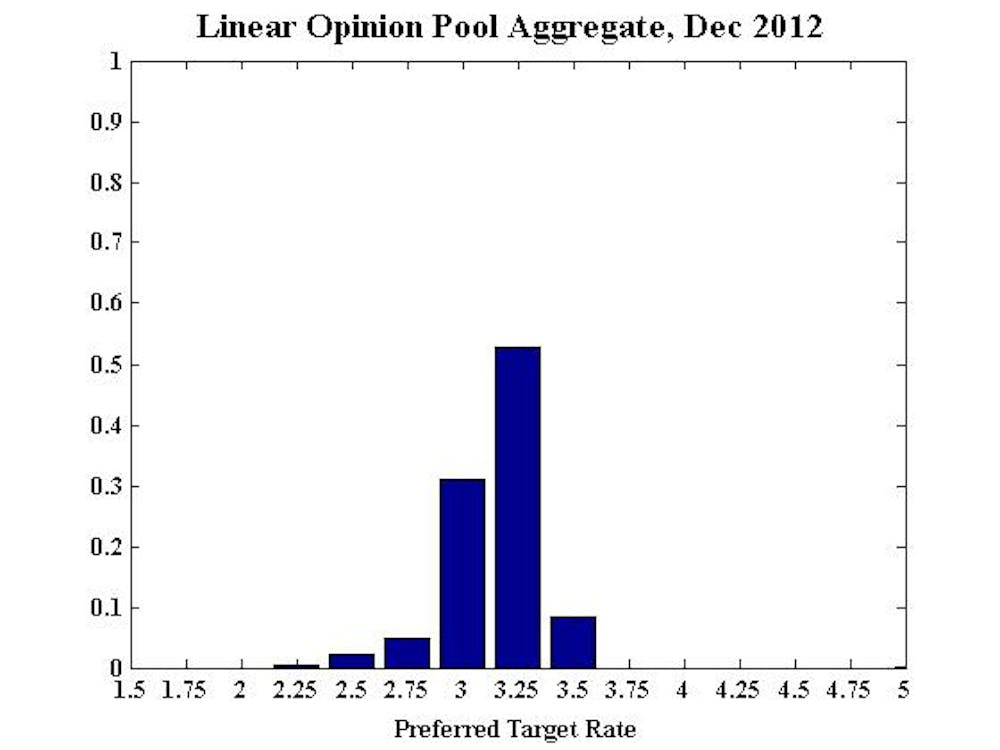

Overall, the Shadow Board strongly supports leaving rates unchanged in December at 3.25%, with around 55% weight. A decrease to 3.00% receives approximately 30% weight.

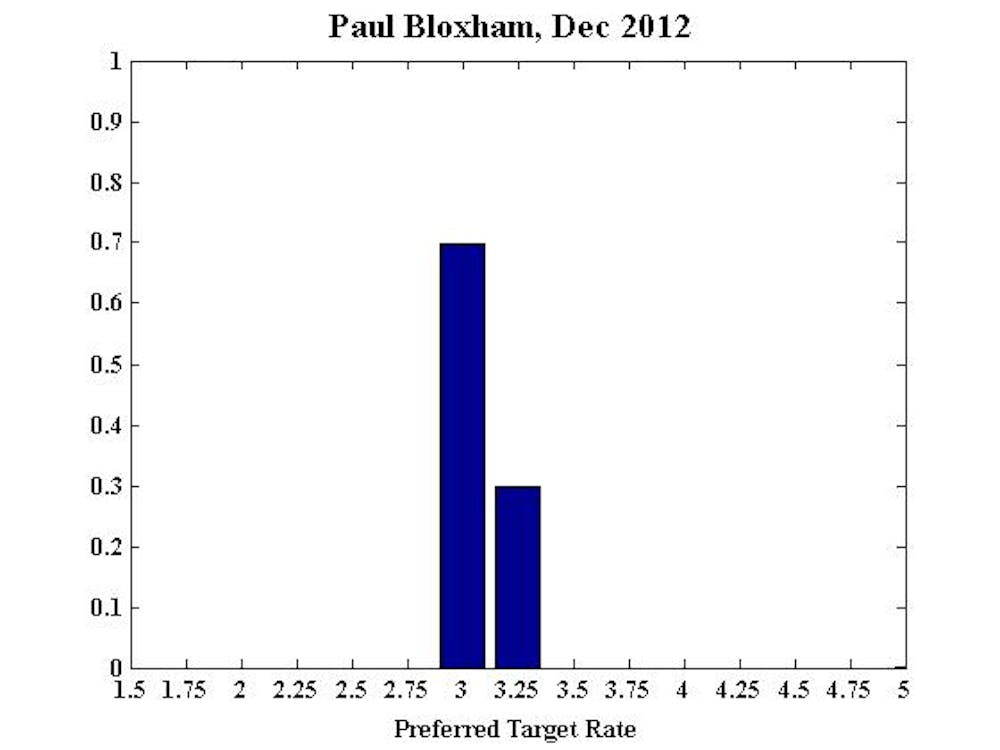

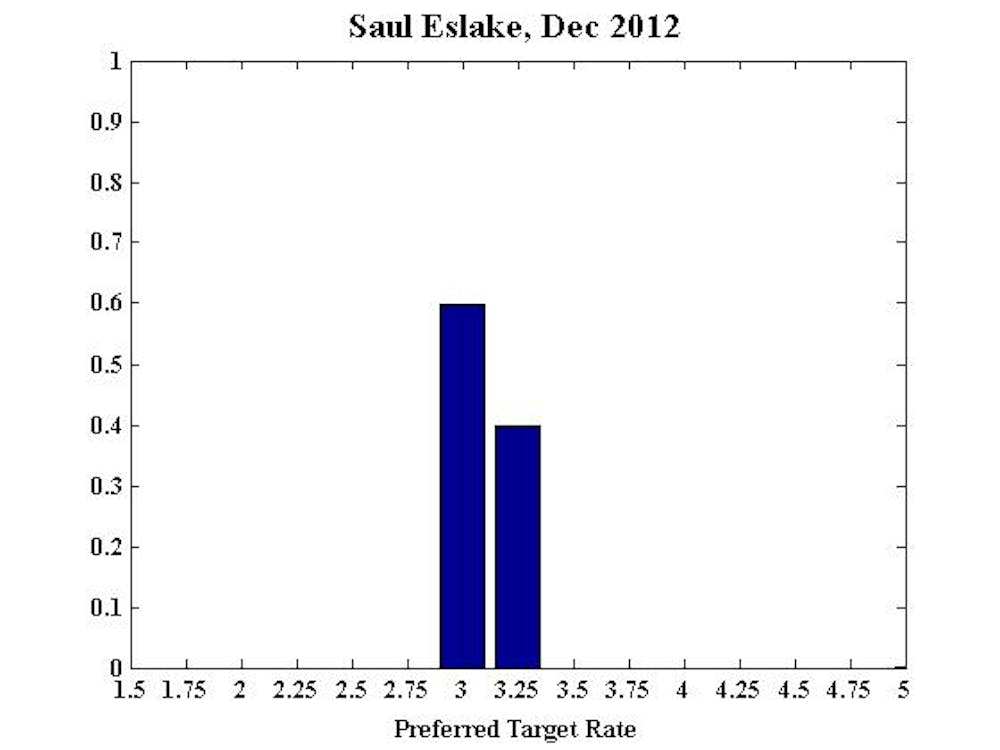

However, there is a split in views between academics and practitioners, with HSBC Chief Economist Paul Bloxham and Bank of America Merrill Lynch Chief Economist Saul Eslake both preferring a cut in the cash rate to 3.00%.

Mr Eslake calls for more support for the the non-mining sector to help combat “headwinds” such as a persistently strong Australian dollar, cautious consumers, low business confidence and fiscal consolidation.

Mr Bloxham says it appears investment intentions for the next year have been revised down, with only “modest” signs that previous rate cuts are having an effect.

“While the interest rate cuts that have occurred so far are providing some tentative support for the housing market, retail spending and consumer sentiment, business confidence is still below average.”

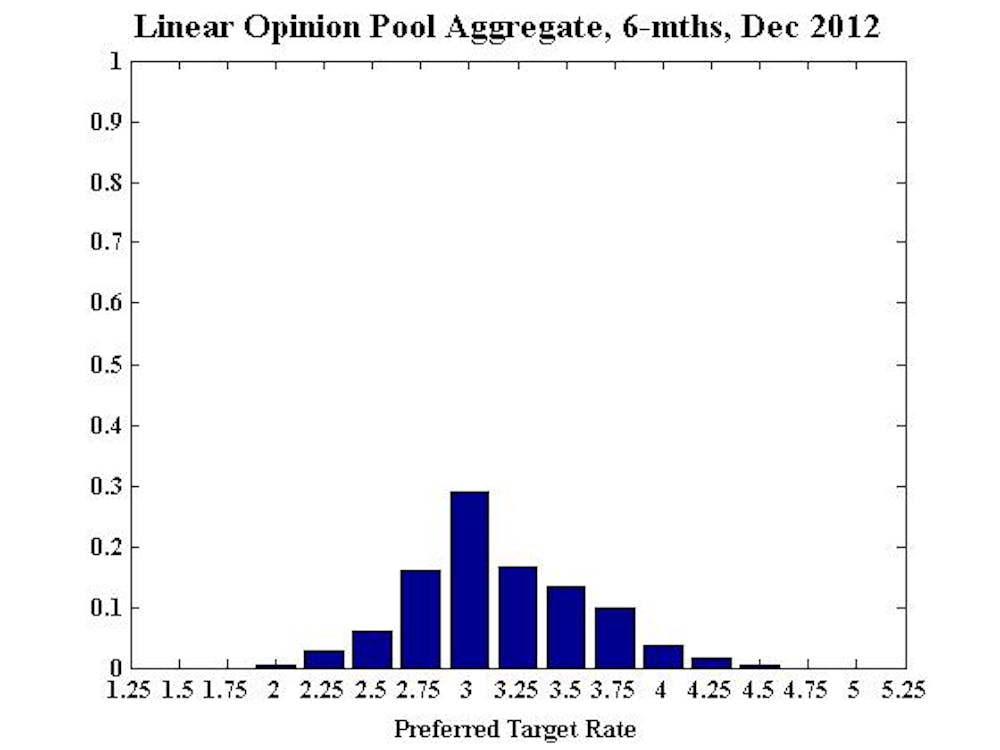

Although many of the academics see weakening inflationary pressures over the next six months, most prefer a slower path of adjustment for interest rates.

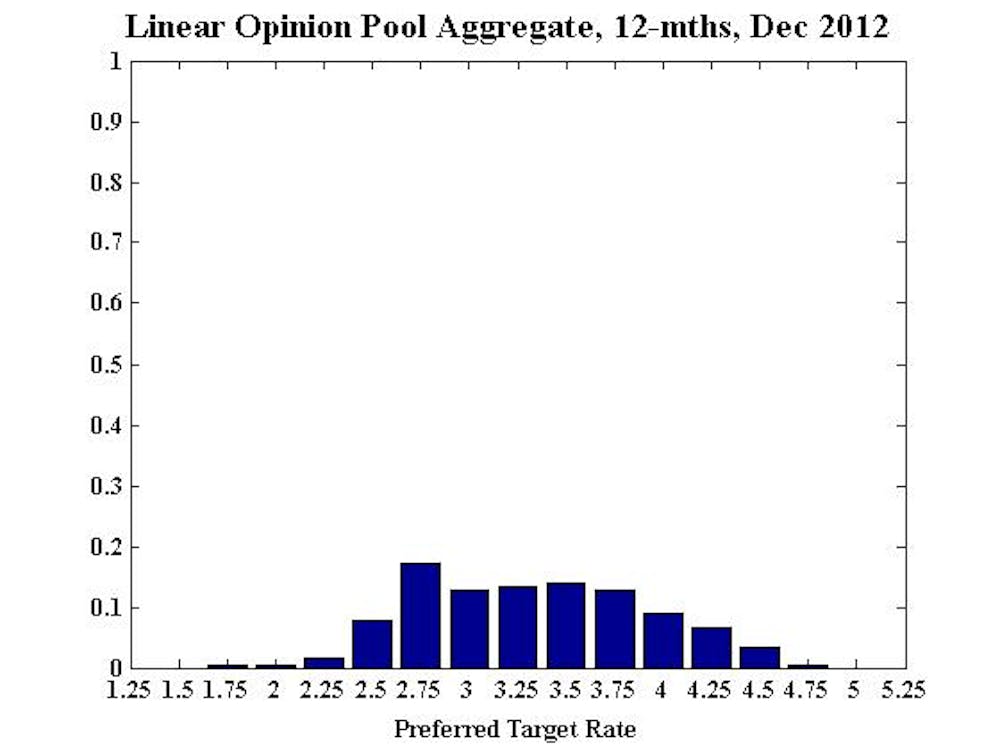

Longer term, several experts anticipate that rates will have to rise.

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd

Inflation remains contained and indicators released during the month suggest a further loosening in labour market conditions, limiting the chances that future wages growth will be excessive. The continued high level of the Australian dollar also reduces the upside risk to inflation. At the same time, information received during the month suggests that investment intentions have been revised downwards for 2012/13.

While mining investment is still expected to rise, the outlook for investment by the non-mining sectors of the economy remains weak. While the interest rate cuts that have occurred so far are providing some tentative support for the housing market, retail spending and consumer sentiment, business confidence is still below average. With upside risks to inflation diminishing, weakening investment intentions and only modest signs that monetary policy is driving rebalancing of growth as yet, I recommend the cash rate is cut by a further 25 basis points this week.“

Also see Paul’s six month and 12 month projections.

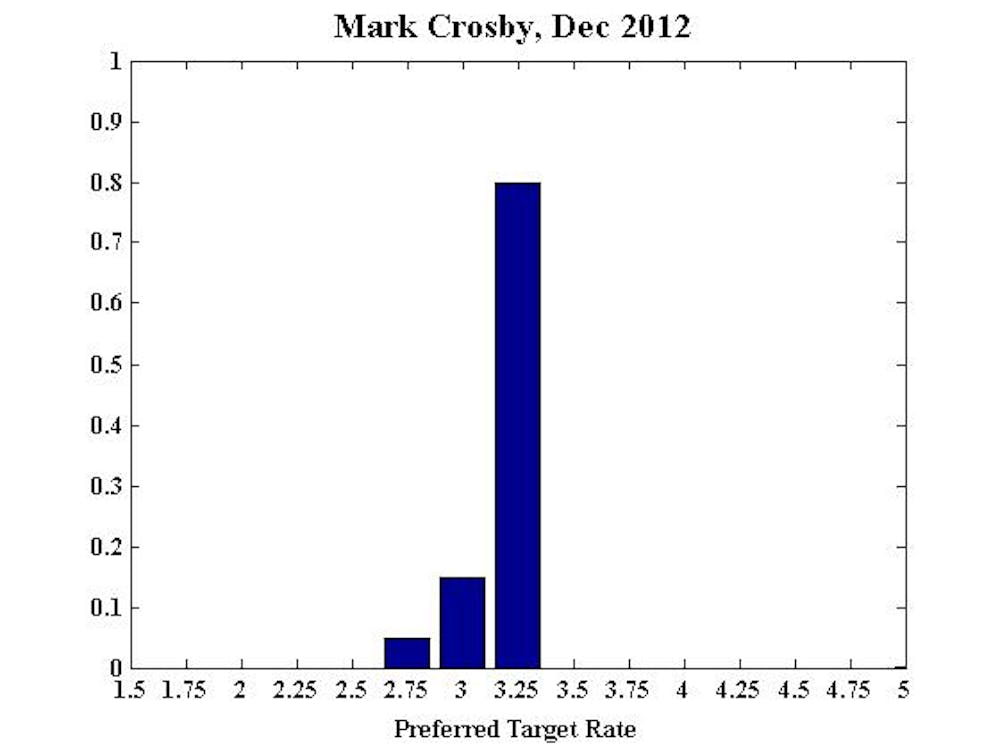

Mark Crosby, Dean of the Global MBA Program, Acting Dean of the Global BBA Program, and Professor of Economics, SP Jain Center of Management in Singapore

The global outlook has not changed much in the past month. Europe continues to plan to have a solution to the insoluble. US debt and housing markets aren’t changing in any significant manner and Asia continues to bubble along. Much focus in Australia has been on a China slowdown, but a more worrying outcome is the sluggish growth and political difficulties with further reforms in India. There would still be a risk to downside shocks during the next 12 months, but also a reasonable likelihood of muddling through. The muddling through outcome would necessitate increasing rates from currently very low levels at some point in 2013.

Also see Mark’s six month and 12 month projections.

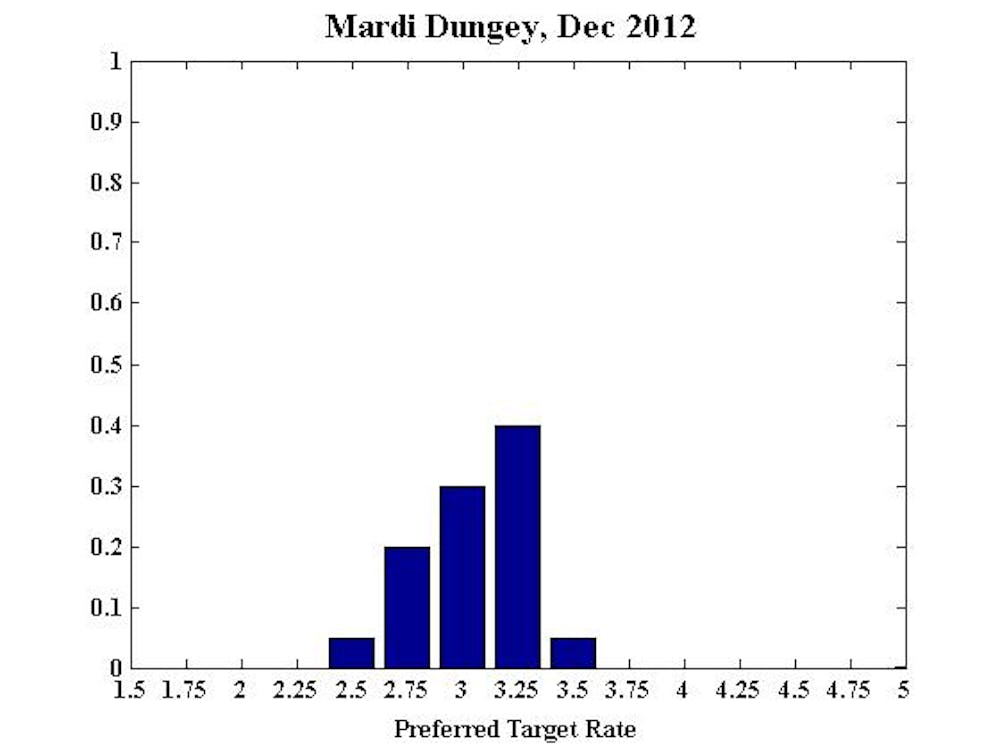

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA

My outlook is unchanged from last month. Given the massive uncertainties still present in the international economy and the potential need to retain flexibility for easier monetary policy in the future, it seems appropriate to retain the current short term setting for monetary policy.

Also see Mardi’s six month and 12 month projections.

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia

Monetary policy needs to provide more support to growth in the non-mining sectors of the economy in order to maximise the prospects of overall growth remaining close to trend as the mining investment boom approaches and passes its peak, especially given the "headwinds” which the non-mining sectors continue to confront (a persistently strong Australian dollar - increasingly a problem for the mining sector as well), cautious consumers, low business confidence and “fiscal consolidation”.

Also see Saul’s six month and 12 month projections.

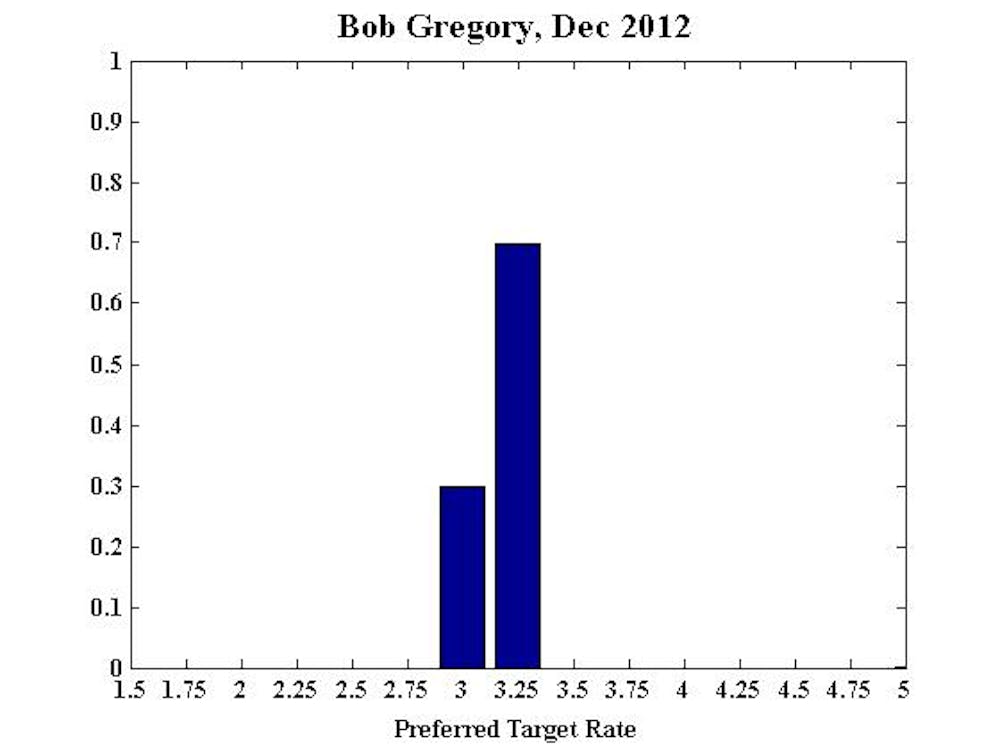

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology

No comment.

Also see Bob’s six month and 12 month projections.

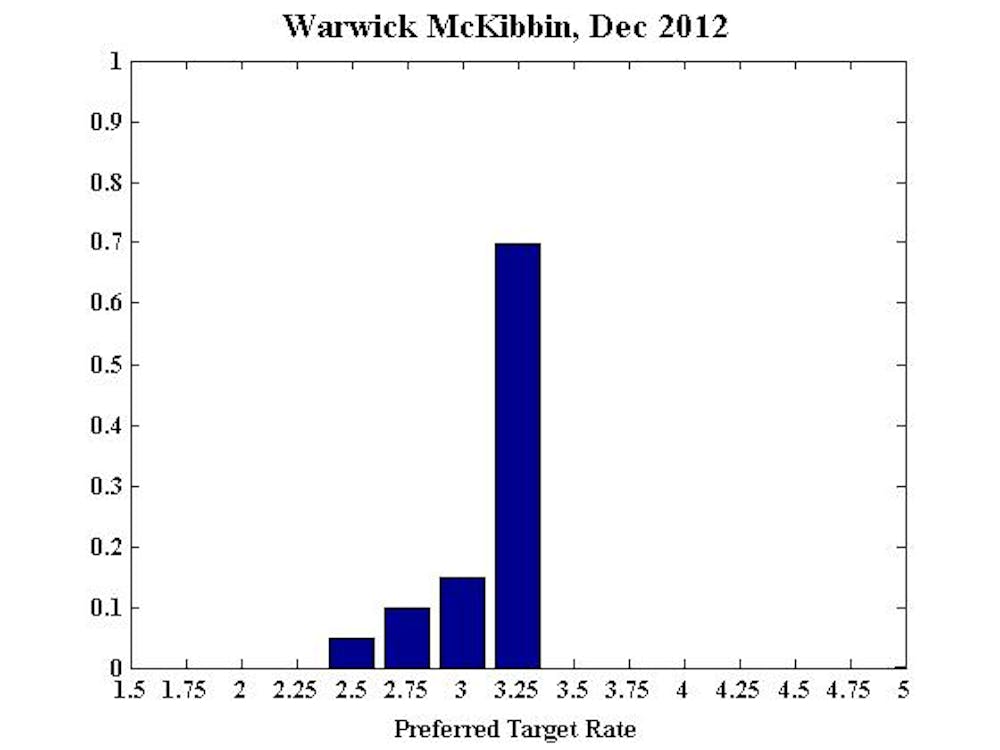

Warwick McKibbin, Professor, RSE, ANU, CAMA

No comment.

Also see Warwick’s six month and 12 month projections.

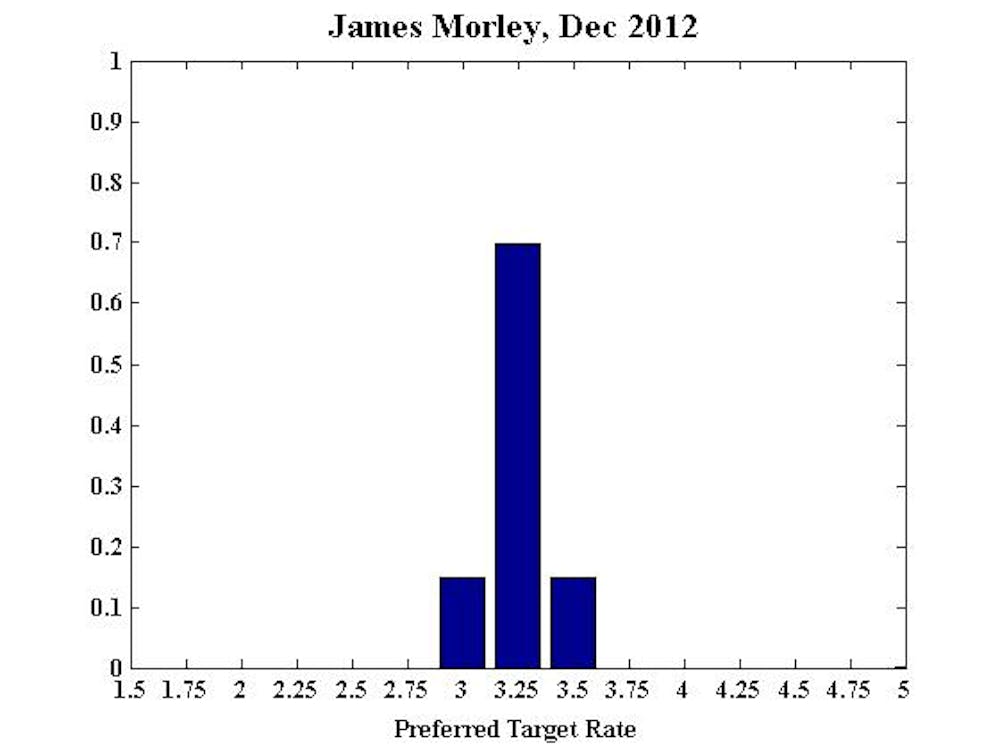

James Morley, Professor, University of New South Wales, CAMA

Given little change in economic conditions (the unemployment rate stabilised in October after an uptick in September) and no new information on inflation or growth, the current stance of somewhat loose monetary policy remains appropriate. Inflation can be expected to remain within the target range in the near term, while developments in China, the United States, and Europe will likely continue to cancel each other out, implying ongoing moderate growth of international demand in 2013.

Also see James’s six month and 12 month projections.

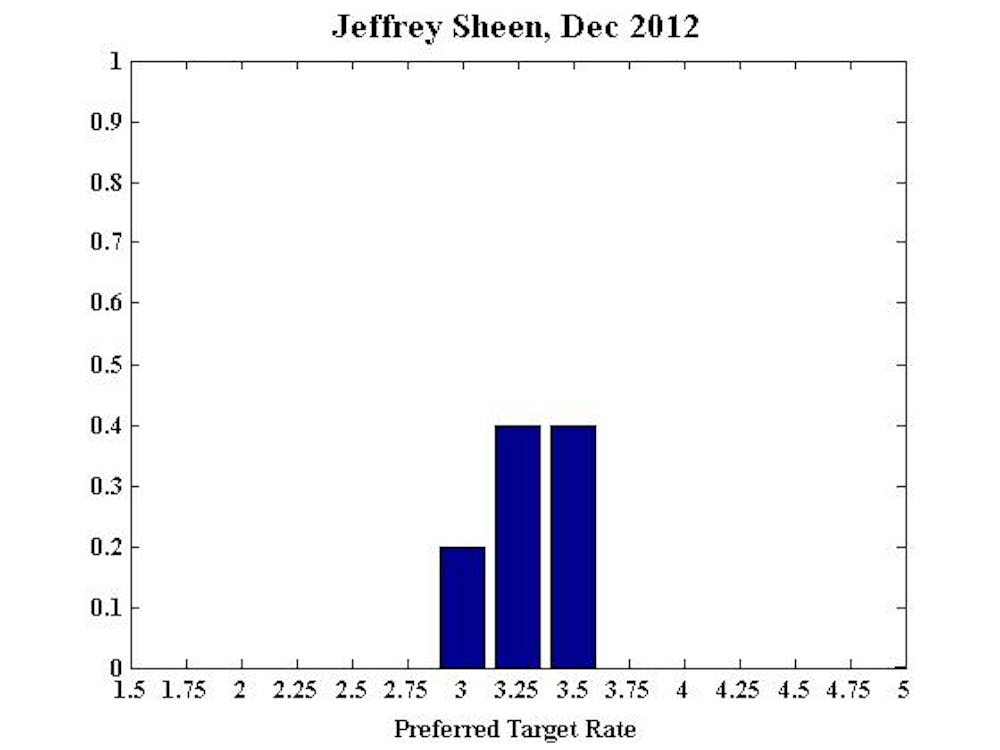

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA

The current Australian cash rate is one notch above the rate that was reached in the depth of the financial crisis, and I do not think the current risks for the Australian economy are anything close to those then. Since there has been little information in the last month to change my view about the current state of the Australian economy, my recommendations remain unchanged. Investment intentions data, though not actual investment data, have weakened. However monetary policy should not be fine-tuned to such uncertainties. Obama’s election in the US does not resolve the fiscal cliff risk, but it does reduce the likelihood of an inappropriately large fiscal consolidation. The prospects in China and Europe are not much different to last month.

Also see Jeffrey’s six month and 12 month projections.

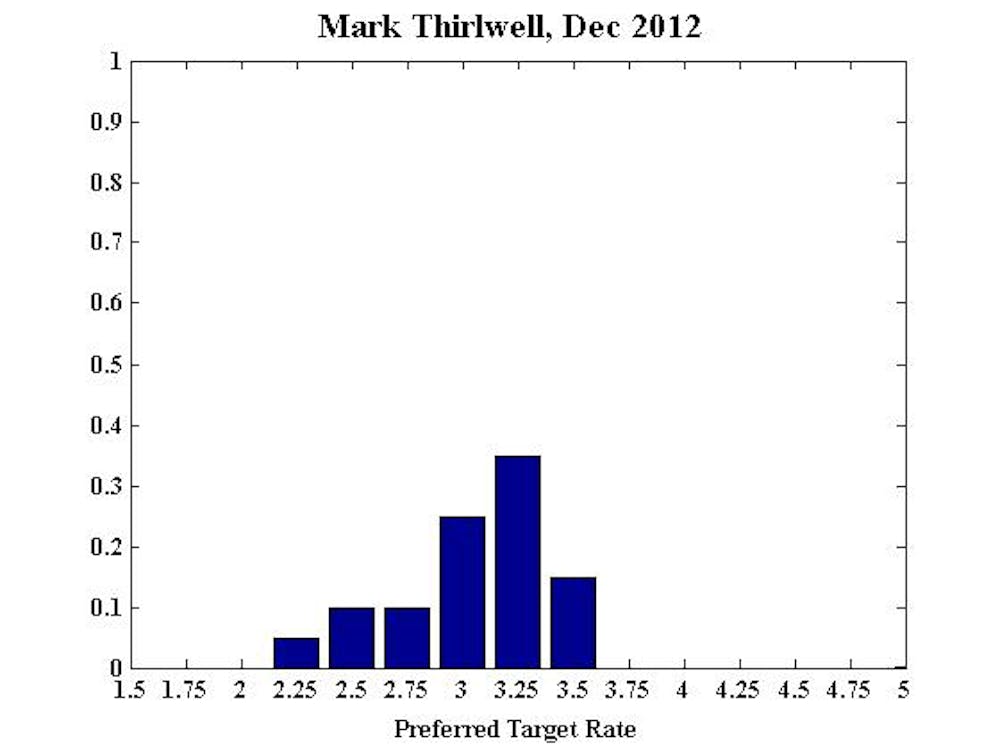

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy

No comment.