Trump’s fiscal policies could mean commodities rally in the short term, boosting the Australian government’s budget, but this could be undone in the long term as his trade policies are bad news for base metals and energy commodities.

Global growth and movements in commodity prices have important implications for the Australian economy. A significant component of economic growth and tax receipts derives from the sale of commodities, and so generally rising commodity prices are a positive for Australia.

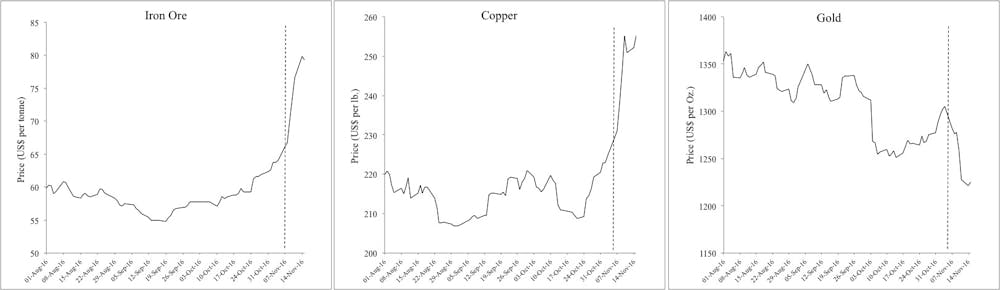

The recent 2016-17 Federal Budget assumed an iron ore price of US$55 per tonne (currently US$79) and a thermal coal price of US$52 per tonne (currently US$105). Treasury also forecast that a US$10 per tonne increase in the iron ore price would raise nominal GDP by US$6.1 billion, and provide an additional US$1.4 billion in tax receipts over the next year. As a result, the government will receive a significant budget boost in the near term.

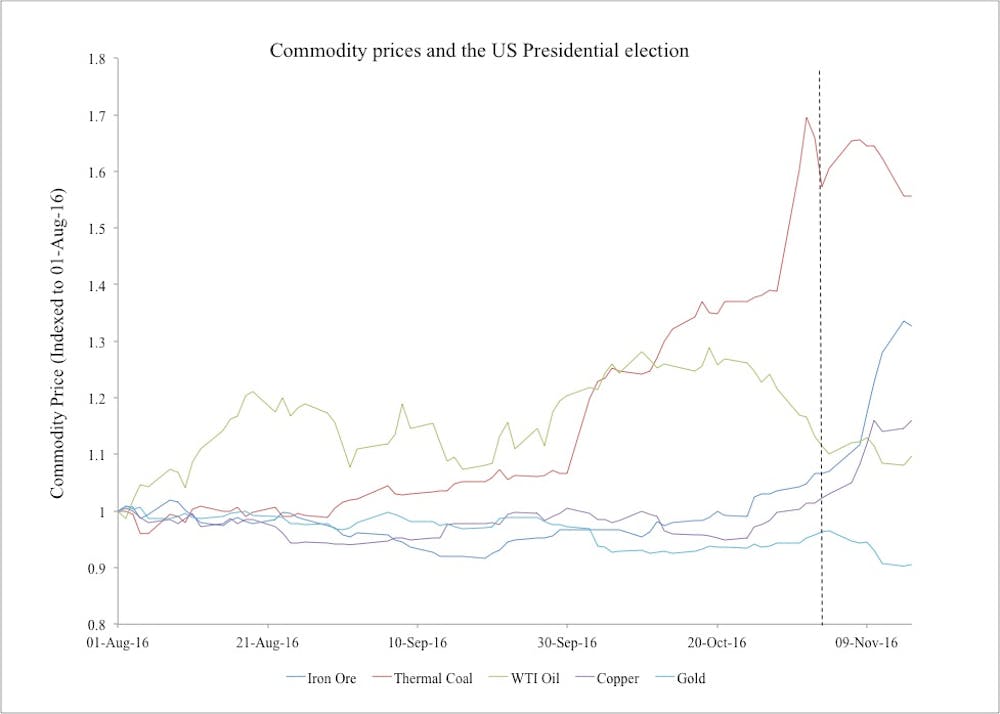

As a Donald Trump victory became increasingly likely, investors were initially cautious. Risky assets, such as stocks, were sold and funds flowed into safe havens such as government bonds and gold. Within hours this reaction was reversed as investors considered the broader repercussions of the result.

Gold has proven to be one of the more volatile assets; the Trump victory initially pushing prices almost 5% higher, but falling 9% from a peak a week before. The price of commodities that are typically related to economic output, such as base metals and energy, have surged as markets hope that Trump will enact a fiscal expansion to boost growth.

Copper (nicknamed Dr. Copper owing to its status as an economic bellwether), which is used in pipes and wiring, has increased in price by more than 7%. More impressively, iron ore has risen nearly 19%.

However these gains could be short lived as volatility sets in, in the long term.

Trump policies and commodities

Much of the volatility in commodity prices relates to uncertainty surrounding what economic polices President-elect Trump will actually seek to implement once he is inaugurated in January 2017. This task is made all the more difficult by the lack of honesty during the campaign and backtracking on policies in the days since. Until there is some resolution regarding Trump’s specific plans this market uncertainty will last – likely benefiting the gold “safe haven”.

Trump has already signalled that he will bring an end to fiscal restraint. He has vowed to drastically reduce taxes, increasing the federal debt by US$7.2 trillion in the process, and pledged to invest US$550 billion in infrastructure. Both measures are meant to boost growth, and both would be positive for base metal prices.

Trump is also not a believer in climate change and is intent on using more fossil fuels. This could be a positive for commodities such as coal (the price of which has more than doubled since the start of the year) and crude oil. However, the outcome is not clear as the promised removal of environmental regulations may also serve to increase oil & gas drilling in the US and produce a price depressing glut.

Greater demand for coal would clearly be beneficial for Australian coal miners (if not the environment). Although the prospect of lower oil prices would not be good news for operators of major LNG projects still struggling to break even, at least households would gain from lower fuel prices.

The more important factor for long term commodity prices is the risk that a Trump Presidency provides for global trade should his policy of protectionism be enacted. If this happens, then global growth will be adversely affected which would be bad news for base metals and energy commodities.

In Australia, this could push the Federal budget further into deficit, reduce economic growth, and increase unemployment (or at least ensure that wages continue to stagnate). Clearly, this would not support the Turnbull mantra of jobs and growth.

A “trade war” also could mean geopolitical tensions will increase, particularly between the US and China, and this would be positive for precious metals such as gold.

At the very least, the coming period will provide greater geopolitical uncertainty that may delay corporate investment, hamper economic growth and put pressure on commodity prices.