A company tax cut has been a divisive feature of pre-budget commentary. Business lobby groups have reacted strongly to modelling produced by Victoria University’s Centre of Policy Studies, which shows that a company tax cut will stimulate growth in GDP and pre-tax real wages, but will cause a fall in domestic income.

Yet a closer look is warranted at the business and industry impacts of a cut to company tax that should be kept in mind as policymakers finalise the May 3 federal budget.

I have argued that a company tax cut presents a windfall gain to foreign investors, while the much vaunted benefits to workers constitute an uncompensated cost to local employers, including many small and medium businesses, and government.

This real concern has been dismissed by the representatives of large business as “highly theoretical”. But the key is that a cut to company tax changes the relative treatment of local and foreign investors in Australia.

Local owners of unincorporated businesses are taxed at their personal tax rate. Because of Australia’s dividend imputation system, Australian shareholders in incorporated business are also taxed at their personal rate, not the company tax rate.

I can’t put it better than Paul Keating, who earlier this year wrote:

Australia’s dividend imputation system works such that the company tax is, in effect, a withholding tax – a tax temporarily held by the Commonwealth which is returned to shareholders when their dividends are paid. So, whether the company tax is withheld by the Commonwealth at a rate of 30% or 25% is immaterial – the Commonwealth is going to return the money to shareholders anyway, regardless of the rate. But the shareholders who will receive a benefit are foreign shareholders.

The forgotten losers: Australian owners of capital

A cut to company tax favours foreign owners of capital, so it favours large corporations at the expense of small business. Some 98% of small businesses (employing four or fewer people) are wholly Australian owned and therefore indifferent to the company tax rate. On the other hand, 30% of large businesses (employing more than 200 people) have some component of foreign ownership. Foreign shareholders in these businesses will be beneficiaries of a cut to company tax.

An increase in foreign investment is generally understood to be a driver of wage growth. This is the basis for the argument that at least half of the benefit of a cut to company tax flows to workers. However, it conceals some important concepts, and it is misleading in the sense that it implies that the benefit to foreign investors is limited to other half of the total growth in GDP.

We find that benefit to foreign investors will exceed the total increase in GDP. In the domestic economy, benefits to workers will be more than offset with a negative impact on domestic investors and the need to address additional government deficit.

Why? Labour moves around the economy, so wages will eventually increase everywhere, not just at foreign-owned companies. This adds to wage costs for domestically owned businesses and government. While foreign investors effectively fund wage increases out of their tax cut, a wage increase will be unambiguously bad for domestic investors, whose tax rate is unchanged.

The potential government deficit created by this policy stems from both the loss of company tax revenue and the increase in wage costs to government. Whatever way it is rectified – through GST, personal taxation, or reductions in government services – it will detract from the benefit to workers.

Industry impacts

Drivers of industry impacts are: changes in the composition of the nation’s expenditure, the capital intensity of industry, and the initial proportion of foreign ownership.

Domestic consumption, linked to incomes, will grow slowly relative to output when company taxes are cut. It follows that the composition of output will gradually evolve in favour of export and investment oriented industries.

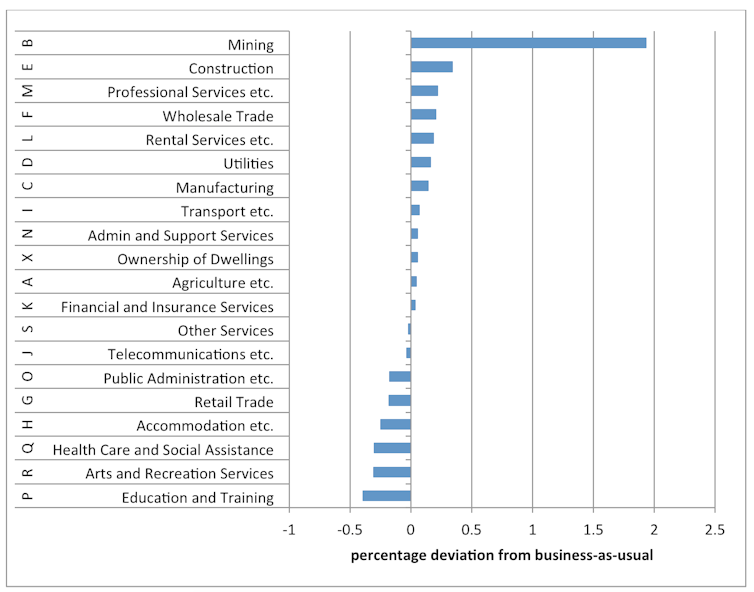

Mining is a winner on all counts: it is capital intensive, mostly foreign owned, and export oriented. The construction sector also expands.

At the bottom end of Figure 1 are the industries that rely on domestic private and public consumption.

Many of these industries, such as retail, accommodation (including restaurants and bars) and health care and social assistance (including child care, residential care and aged care), are important employers of people in relatively low-wage occupations, women, and part-time workers.

It’s easy to see why a company tax cut polarises opinion, as it generates clear winners and losers. Foreign investors will receive a windfall gain at the expense of Australian residents. Economic growth induced by differential treatment of foreign and local investors merely creates the illusion of a benefit for all.