Baby boomers have a greater share of the UK’s wealth than any previous generation in the modern era. And unlike their parents and grandparents, the boomer generation also holds a much higher share of this wealth in housing. Meanwhile, with house prices high relative to their incomes, many younger people and families are are unwilling or unable to accrue wealth through home ownership. Increasingly, 25 to 34-year-olds rent.

This housing wealth inequality between the generations seems unfair. But can we blame the housing wealth of the boomers for preventing younger generations from getting on the property ladder? While baby boomers have generally profited from rising property values, the real reason for the UK’s housing problem is a lack of supply.

Boomer beneficiaries

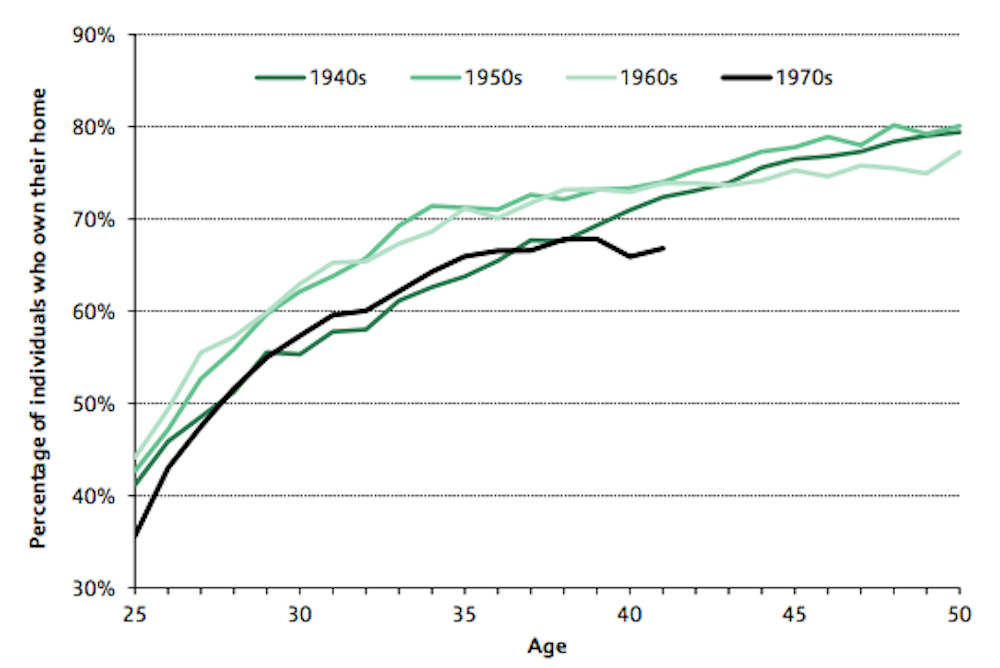

The boomer generation mostly owned their homes already before the housing boom started around 2001, as shown in the chart below. So they got to enjoy the wild ride in house values with relatively little debt to pay off. Meanwhile, wealth inequality across generations increased during this period.

Younger households either managed to buy when prices were high with the help of large mortgages only to see their house value drop, perhaps, during the subsequent bust that began in 2008. Or, if they hadn’t got on the ladder yet, the falling earnings and rising credit standards of the post-financial crisis years meant they were then unable to climb onto the ladder at all.

Not the boomers’ fault

Now, with house values again rising faster than earnings around London, it is perhaps irritating to some that so many older households sit in underused homes, while younger generations struggle to find affordable housing. The Intergenerational Foundation is particularly upset. But for the most part, this isn’t the boomers’ fault.

The relatively large climb in home values is mostly the result of a restricted supply of housing combined with demand factors that are largely unrelated to the ageing of Britain’s population. While older households have benefited from this confluence, they share only perhaps some indirect blame for it.

House prices rose sharply across England from 1996 to 2005, hugely benefiting the many boomers that had bought their homes during the previous decade. This turn of the millennium boom was the result of rising demand for a limited supply of housing stock. This was in turn fuelled by a number of smaller national trends including relaxed lending standards, increased immigration and, at least initially, widespread growth in household incomes and wealth. Perhaps underneath all this were “exuberant expectations” of continued out-sized capital gains. Changing demographics, a much lower-frequency phenomenon, probably contributed little to the demand-side push on house prices.

Geographic evidence

Since the subsequent housing bust, London has claimed the lion’s share of the increase in English house prices. Much of England north of London has seen relatively little – if any – increase in prices since then. This does not match up with where the majority of baby boomers are – they have been ageing in the wrong place to be the cause of this southerly tilt in the housing recovery.

Outside of London, England and Wales are getting older:

The young are moving in droves to London. If anything, those grandparents with all their superfluous bedrooms in the villages in the north are the only ones keeping the lights on (and keeping house values from collapsing). Instead, the London-based recovery in house values relies on youth and foreigners. The young want to live in London and foreigners want to invest in it.

All the above factors have been shifting housing demand. If Britain would simply build more houses, prices needn’t have responded so drastically to this rising demand. Of course, the British housing supply problem has long been known.

Moreover, if Britain built more houses, it could build them in the places most needed and with the specifications most demanded. Supply should expand more rapidly in London and the south-east, where demand is highest. Plus, Britain’s ageing population and shifting social norms has created an ever larger demand for housing better suited to the needs of older households. Older households would be far more likely to downsize if this kind of retirement housing were built.

Supply blockers

Of course, older households, who are more likely to vote as well as to own, probably do bear some responsibility politically for blocking supply. Voting homeowners, and disproportionately so older homeowners, tend to disapprove of politicians that approve new building in their neighbourhoods. This has led to brazen political cycles in construction, which perverts the planning process, misallocates housing and raising prices.

Picture a retired couple in their mid-60’s, with children who’ve long since moved out and grandchildren who may just be old enough to visit the odd week during the summer, an empty bedroom or two still furnished with their parents’ childhoods dustily waiting for them. Barring a large change in circumstance, this couple will likely stay in their family home for many years. They know their neighbourhood. The furniture they’ve collected over the years fits just so in their present space. And if they own the average house in England, its value has grown a bit under 4% (in real, inflation adjusted, terms) on average for the last 20 years.

Over the next decade, as the boomer generation slowly ages into its golden years, the UK will have more and more of these households. Given the many risks they face and the relatively few housing choices available to them, clinging on to a house that is too large for their everyday needs is mostly rational.

Besides their pension, a house is far and away the largest store of wealth for those in their 60’s and beyond. Releasing equity by downsizing to a smaller home in a new location may be attractive in theory but there are high transaction and psychological costs in these moves. And, besides, with house prices generally growing again, the returns to be had from staying are too tempting.

Rather than using economic incentives (such as capital gains and stamp taxes) to lever boomers into smaller houses, Britain should look to correct the misaligned political and economic incentives that local councils have to block new housing from being built.

A healthy housing market with the right policies would channel the huge foreign desire to invest in English housing towards building homes for younger (and older) households. House prices would be less buoyant. Retirees with “too much house” would downsize of their own volition, in turn releasing equity for their own consumption and putting a family home back into the market for a new generation to enjoy.

This article is part of a series on What’s next for the baby boomers.