Companies have finished reporting results for the financial year so it’s time to take stock of how the different business sectors of Australia are fairing. In our company results wrap series we take a step back from the short-term focus of quarterly profit and loss statements and examine what big picture factors are at play.

The energy sector is dealing with a complex mix of relationships between consumer trends, global commodity markets, and state, federal and industry regulation. Because large established companies in electricity generation and distribution and coal and natural gas export have a lot of influence in this process, Australian energy regulations reflect more traditional energy provision rather than global trends where renewable energy is becoming more prevalent.

State governments are currently coming to terms with the regulatory changes needed to accommodate public support for disruptive technology. One example is the ongoing adoption of ride-sharing company Uber. However this same pragmatism needs to be reflected in preparations for the provision and consumption of energy in Australia. The energy companies that are prepared for this disruption will survive and flourish, while those that cling to traditional structures will struggle.

Evidence of disruption

Globally energy companies are already showing signs of being affected by the looming disruption. Coal miners have been subjected to multiple forces over the last decade, but the changing landscape associated with new forms of energy, is a strong influencer of their performance. Coal companies in the US are facing dwindling share prices or bankruptcy like Peabody Energy and Arch Coal.

Tesla’s share price, which increased from US$28.52 in August 2012 to US$220 in August 2016, is more than double that of more traditional vehicle company Toyota. Toyota has experienced moderate growth from US$79.62 in August 2012. With electric vehicles forcing themselves into the motor vehicle market, technological disruptors like Tesla are seen as more likely to succeed than traditional motor vehicle companies like Ford.

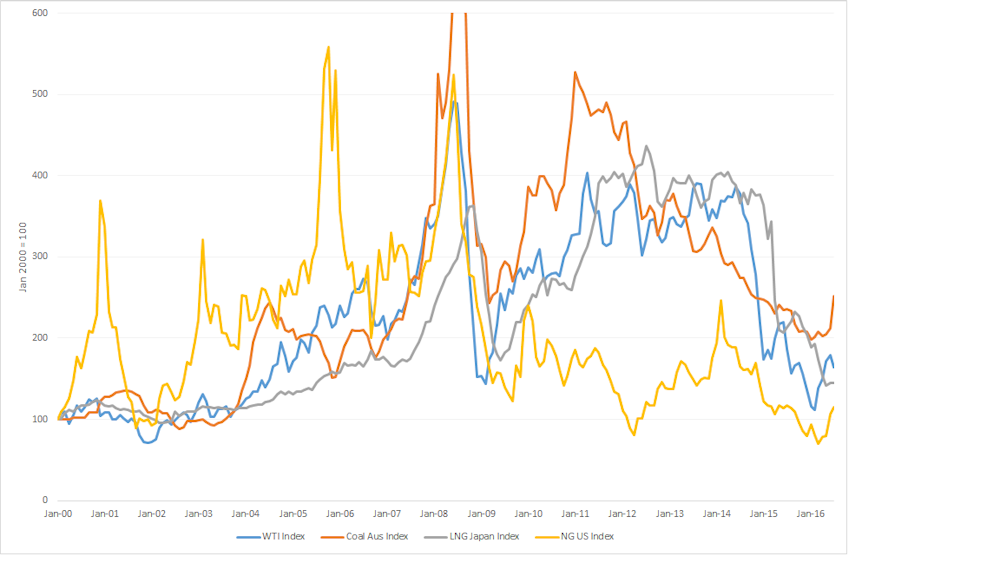

West Texas Intermediate, a benchmark international oil price, declined from US$133 a barrel in July 2008 to US$45 a barrel in July 2016. This followed a slowdown in global growth after the global financial crisis and increased production of oil in Saudi Arabia, which some claim is to gain market share. Coal prices for export from Australia have fallen from A$180 a tonne in July 2008 to A$63 a tonne in July 2016 as China’s voracious appetite for coal has declined.

International natural gas prices have also declined because in Europe the natural gas price has been referenced to the oil price. Separate to this, the US price of natural gas declined as a result of new drilling technologies which released huge quantities of natural gas onto the US market, dragging down the price.

Many of these global trends are apparent in Australia too. Coal export prices have caused concerns for existing companies to the extent that new mine development has been shelved since 2008. Coal mine profits have dwindled and job losses abound.

Ambitious plans for coal seam and natural gas extraction for export to Asian markets have been curtailed with some experts predicting still further price declines in response to oversupply.

While there have been recent small upticks in prices, the trend for Australian primary energy company share prices since early 2014 has been downwards.

Challenges facing the Australian electricity generation sector

The electricity sector in Australia is facing multiple challenges. Electricity consumption has declined since 2009 and is forecast to increase only slightly by 2035/6. The closing of large energy users like the Kurri Kurri aluminium smelter and the Clyde Oil refinery, and a shift by residential consumers to the consumption of electricity from solar panels have contributed to this trend.

This is coupled with increasing supply of energy from low marginal cost wind power which, if the Australian National Energy Market is working as designed, reduces the spot price for electricity.

Many electricity generators have launched or acquired retail businesses to market directly to customers. AGL and Origin are the two largest of these “gentailers”, with a combined 56% of the small customer market in the eastern states. However, there is potential for disruption to this existing industry model. 1.57 million households now have solar panels on their roofs, and residential batteries are expected to increase consumer control of residential electricity.

Startups like Sunverge, Reposit and Powerledger are looking to connect households with spare energy to households buying spare energy. Mojo Power is offering customers fixed price packages that are more reminiscent of mobile phone offers than electricity. At this stage it is unclear whether the National Electricity Market will play a part in, or hinder, these new business models.

A few retail companies, like Red, Lumo, Powershop and Infinite spruik their renewable energy credentials. Renewable energy is viewed very favourably by the public.

Recent polling suggests that 71% of respondents would favour a government that facilitated greater support for solar panels and batteries. Energy giant AGL has a larger renewable energy portfolio than Origin making it slightly more attractive to consumers with environmental concerns, but it is exposed to the risk of owning a large coal generation fleet.

Infigen is the only renewable, publicly listed company. Infigen faced torrid times during the multiple back-to-back reviews of the Renewable Energy Target, but since the target has been set at 33GWh, Infigen’s share price has been recovering.

Of note, is the share prices of domestic energy companies AGL and Origin who are both in the business of generating and retailing electricity and previously were both engaged in the development of coal seam gas. Origin has continued its coal seam gas investment while AGL exited the market. AGL has instead focused more on diversifying its electricity generation portfolio. Part of this strategy has involved formulating innovative plans for virtual power stations of consolidated rooftop solar panels and residential batteries.

Origin’s foray into the export of Liquid Natural Gas (LNG) has not been good for its share price. Concern over debt related to the investment in LNG and exposure to declining LNG prices has worried investors.

Electricity distribution also faces multiple challenges

Electricity distribution companies in Australia are regulated monopolies. Distribution companies in NSW and QLD have been government owned and as a result of hefty investment plans, large electricity price rises were passed through to customers after 2009. This was at the same time as environmental charges were being included in electricity tariffs.

Customers were angered by the rise in electricity prices, but the NSW and QLD governments have enjoyed the profits that have flowed back into state coffers.

The NSW government is now seeking to sell a large share of its distribution businesses, although the most promising buyers have been knocked back by the federal government due to security concerns. With the popularity of solar panels and the expectation about the benefits of battery storage to meet demand after sundown, investors buying into the electricity distribution sector will be facing disruption.

Origin and AGL have gambled on different strategies to face a future with carbon constraints and technological disruption. Origin has bet on natural gas being a transition fuel to a cleaner energy future, while AGL is betting on electricity from renewable sources with batteries as the preferred path.

Energy distribution companies need to wrestle with the technological disruption that is looming from decentralised, distributed generation from solar panels, batteries and peer-to-peer energy transactions. Coal miners should seriously consider diversification to face a carbon-constrained future. The energy sector is in a state of transition; profits and share prices may be volatile for a few years to come. It would be advantageous if regulation did not get in the way of the shifts already evident.