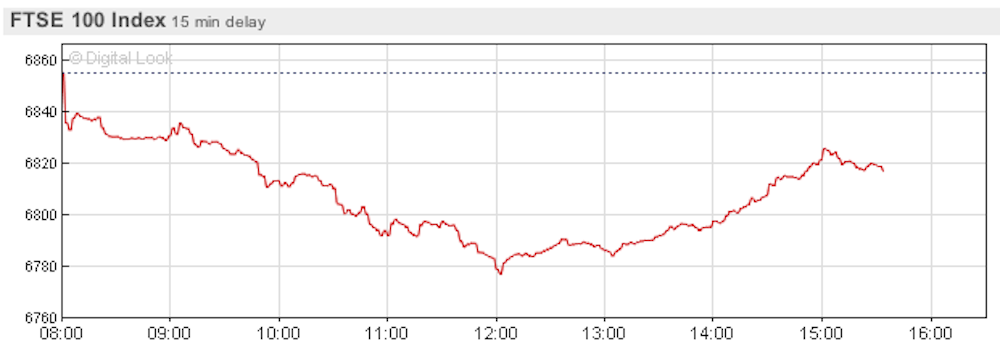

On the back of the rising prospects for a Scottish Yes vote to independence next week, the markets have taken a hit. The FTSE100 and FTSE250 posted drops that were markedly worse than performances in other stock markets. Sterling fell to its lowest level in 10 months, while UK gilts were affected too. One important question that needs to be asked is whether market uncertainty could reach a level where it affects how the Yes and No asides conduct their campaigns and any subsequent negotiations in the event of a Yes vote.

Until Monday, the stock market had not seen much impact from rising Yes momentum, but this may now be changing. Among fallers, a fair few of them have been Scottish companies. Royal Bank of Scotland was one Scottish stock that had fallen somewhat since the opinion polls began suggesting a lift in the pro-independence vote last week, down between 3% and 4% overall. It fell another 2%. Other Scottish companies that had so far defied the drift downwards, such as industrial group Weir, lost ground.

The same thing happened to Aberdeen Asset Management, another player that had been on the rise in a sector where it would perhaps be expected that it would be more affected by independence and the uncertainty created by the vote. After all, the financial sector is very important to Scotland and arguably more linked to the rest of the UK through the financial regulatory bodies than other parts of the economy. Standard Life, Scotland’s other big financial player, also drifted down after a sharp rise last week.

Currency jitters

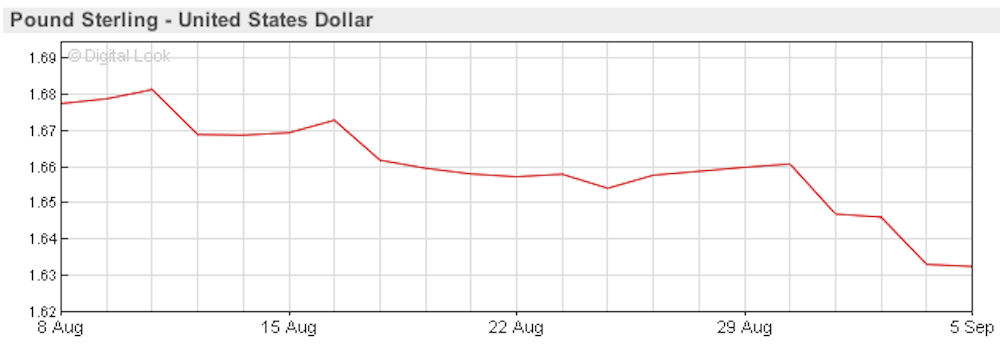

The upheaval in the foreign exchange markets is also to be expected. In truth, it is difficult to know the extent to which Scotland is causing this decline, as events in the Ukraine and the eurozone may have played a part. For instance, Russian investors hold substantial levels of assets in the UK, so the imposition of sanctions on Russia recently may have had an effect. Sanctions raise the prospect of Russians moving their capital out of the UK and flooding the markets with sterling.

Yet it also makes sense for the foreign exchange markets to be unsettled by the uncertainty over the pound. The situation would mirror the problems in the eurozone over the potential for its members to leave the euro.

There is some recent empirical evidence that as the possibility of a country leaving the euro increases, so the euro falls in value. So the recent improvement in the opinion polls for the supporters of independence is likely to have contributed to recent falls in the pound against other major currencies. And we have also seen direct effects on the cost of hedging currency holdings in the event of a Yes vote in the past couple of weeks.

The other two asset classes that you might most expect to see affected are government bonds and credit default swaps, which in effect offer insurance policies for both company bonds and government bonds. Credit default swap prices have so far been flat. Movement in government bonds – aka gilts – has been more inconclusive than currency or stocks so far, but certainly the yield on 10-year bonds increased to 2.49% in September from 2.37% in August – meaning the bonds became less valuable.

Although as with foreign exchange markets this could be due to problems elsewhere in the world, this is one of the markets that could be most directly impacted by independence. This is because the yield reflects the chances of the debt being repaid and there is a suggestion that if Scotland can’t retain the pound, it will not accept any of the UK’s debt. The rise in this interest rate affects the cost to the UK government of raising new funds through the bond markets, so potentially it could affect the UK’s fiscal position.

If the markets were to become excessively volatile as a result of any market fears regarding the outcome of the vote, it may be necessary to reach temporary agreements between the relevant parties regarding a potential currency union before the vote takes place. This could involve agreeing to some form of temporary currency union after the vote until some agreement on a permanent solution is reached. There isn’t much evidence to suggest this scenario will occur in the near future, but if the markets become sufficiently volatile either before or after a Yes vote, it could yet affect the courses of action chosen by the politicians.