While federal election watchers will be avidly fixed on the Reserve Bank of Australia’s decision to alter the cash rate decision today, economists are more interested in global factors and signs of weakness in the domestic economy.

The outlook for the global economy continues to look uncertain; it appears as though only the US economy has potential to surprise on the upside.

Domestically, the unemployment rate is edging up. Inflation is currently well contained but as the Australian dollar has continued to depreciate, there are concerns in the medium term that this will put upward pressure on inflation due to higher import prices. However, in the near-term the stimulus from the lower dollar and the historically low cash rate has yet to be fully transmitted to the real economy.

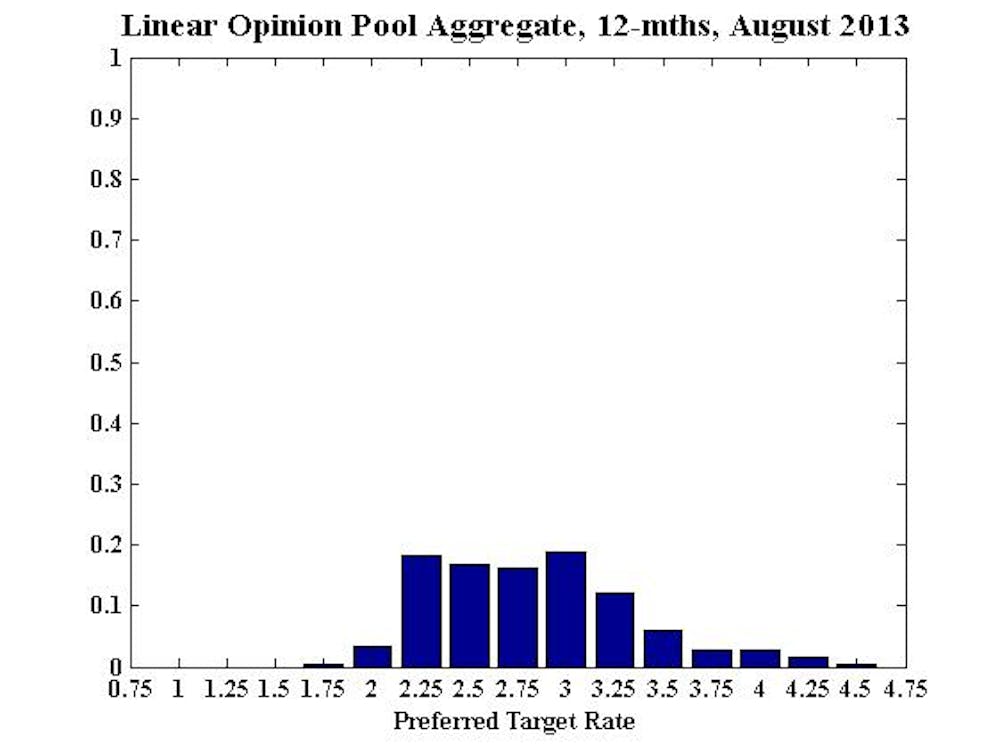

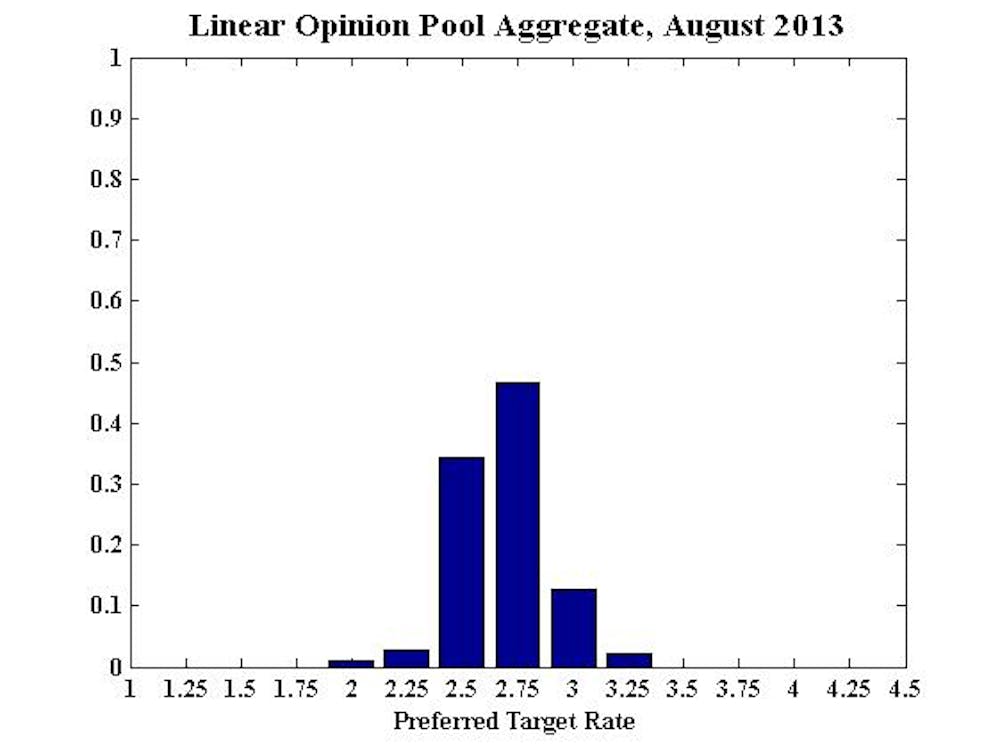

The consensus of the nine shadow board members for keeping the cash rate unchanged at 2.75 percent has dropped from nearly 70% in July to 47% in August. Members are nearly 40% confident that a reduction of the cash rate by 25 basis points is the most appropriate policy.

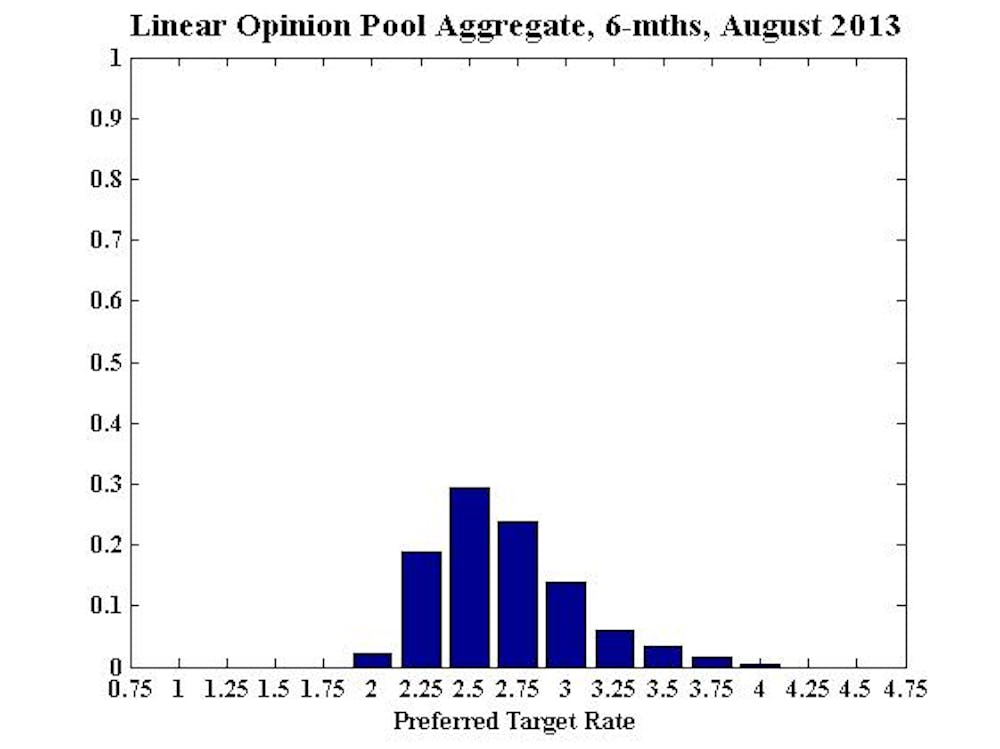

The shift towards a rate cut clearly shows up at the six-month horizon: the probability that rates will need to rise in the next six months has dropped from 30% to 25%, while the probability that rates ought to be lower than the current rate has increased to 50%. A year out, the shadow board members continue to attach about a 45% probability to the need for an increase in the cash rate and approximately a 40% probability to the need for a decrease in the cash rate.

The Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set.

The project is designed to test and improve transparency of central bank deliberations by revealing the opinions of individual members, emphasising the underlying macroeconomic uncertainties.

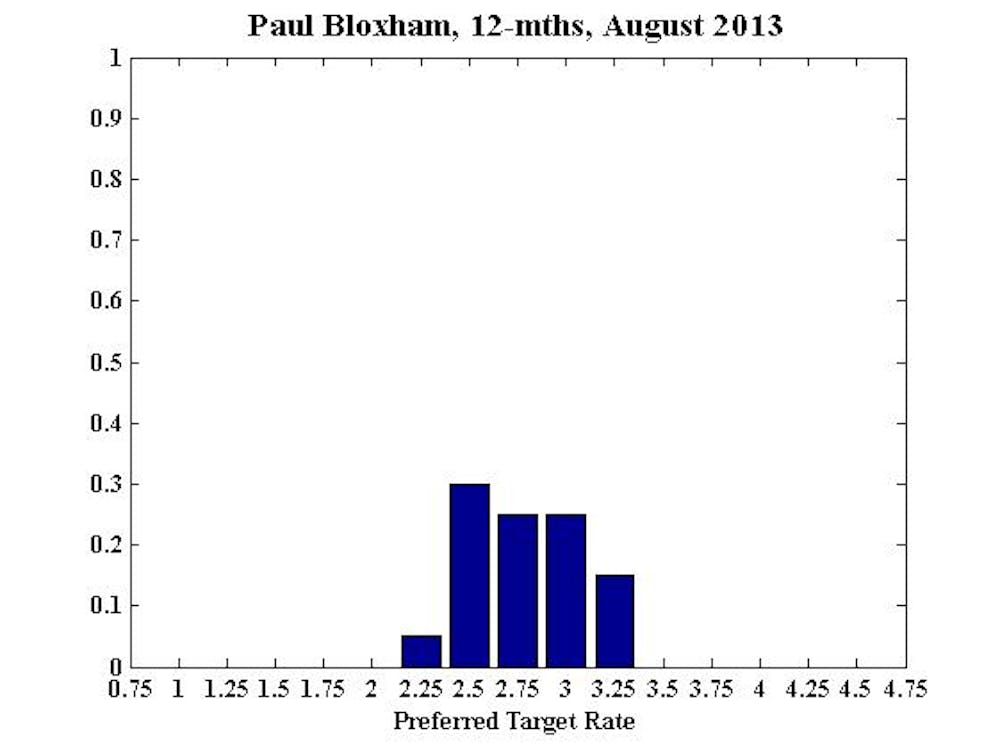

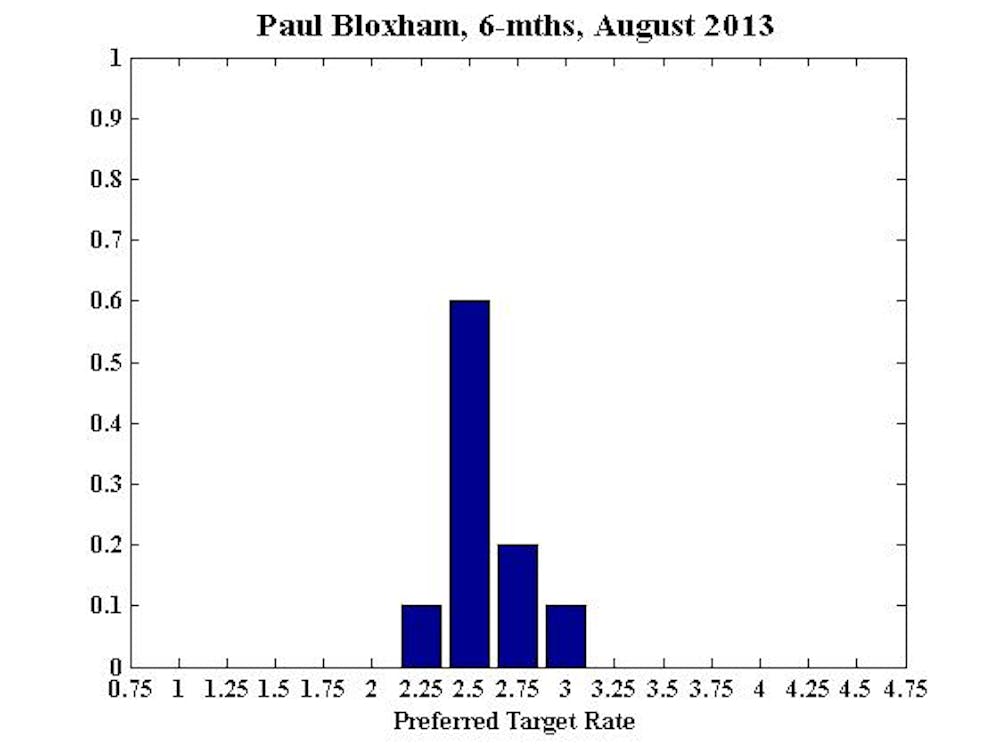

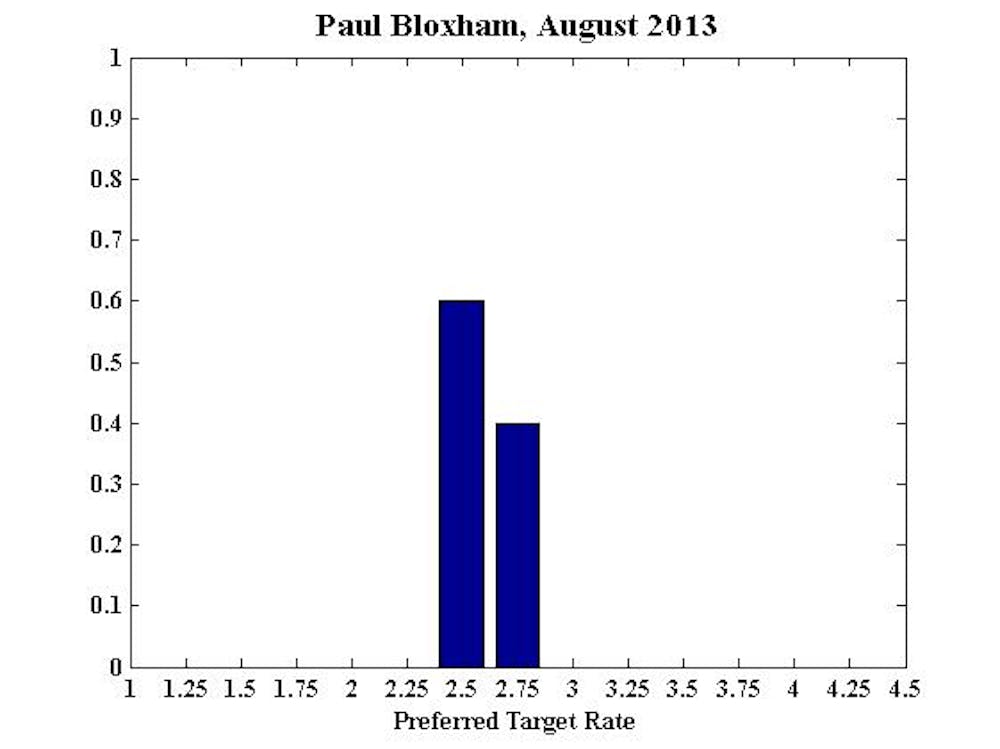

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

Inflation is comfortably in the lower half of the target band and even though the recent decline in the Australian dollar should be expected to see a pick‐up in imported goods prices, the current looseness of the labour market is likely to keep wages pressures at bay. Growth is also a bit below trend, with low rates still only getting significant traction in the housing market. Given low inflation and below trend growth the RBA could consider cutting rates a bit further. I recommend the cash rate is cut by 25 basis points to 2.50%.

My medium-term view for rates has shifted a bit, however, reflecting the recent depreciation of the Australian dollar. With the dollar now at a lower level, inflation should be expected to rise modestly in coming quarters, which may start to limit the extent to which further rate cuts can be delivered.

The outlook for the AUD is critical in this regard and is, of course, highly dependent on offshore developments. There are growing signs that the US economy is recovering and as a result the Federal Reserve may begin to slow its asset purchase program soon. This would put downward pressure on the AUD which could deliver more inflation in Australia.

With the economy currently operating below capacity this inflationary impulse would not be a concern as it is unlikely to see rising wage pressures. However, if local growth does start to pick up soon, the upside risks to inflation may start to emerge, limiting the scope for rate cuts and perhaps implying that rates may have to start heading back towards neutral.

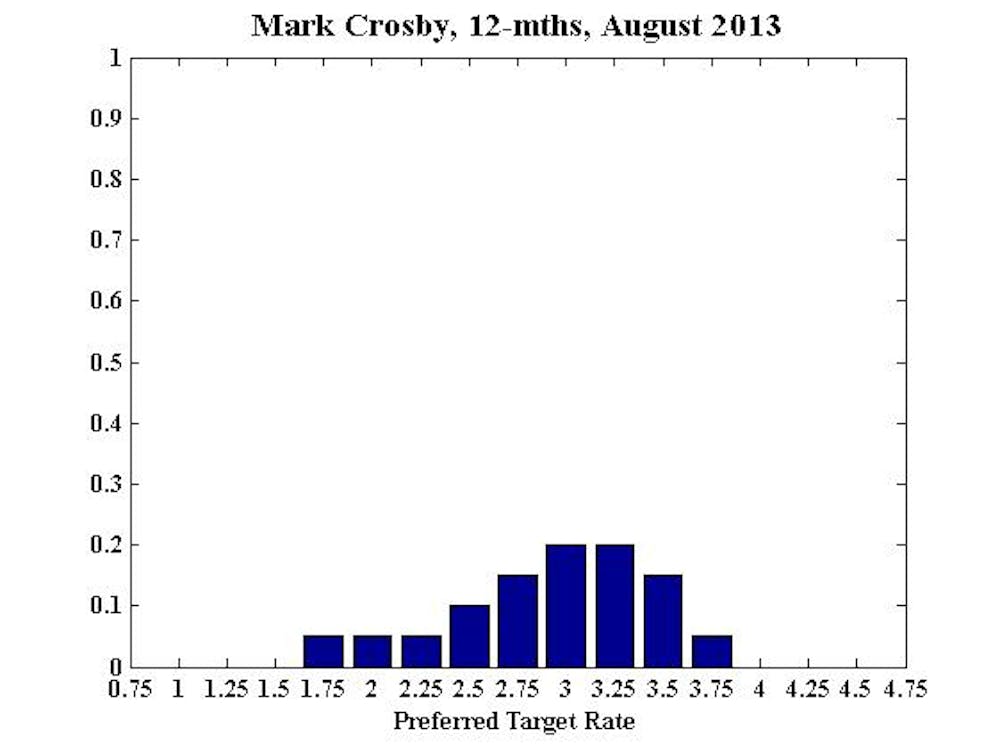

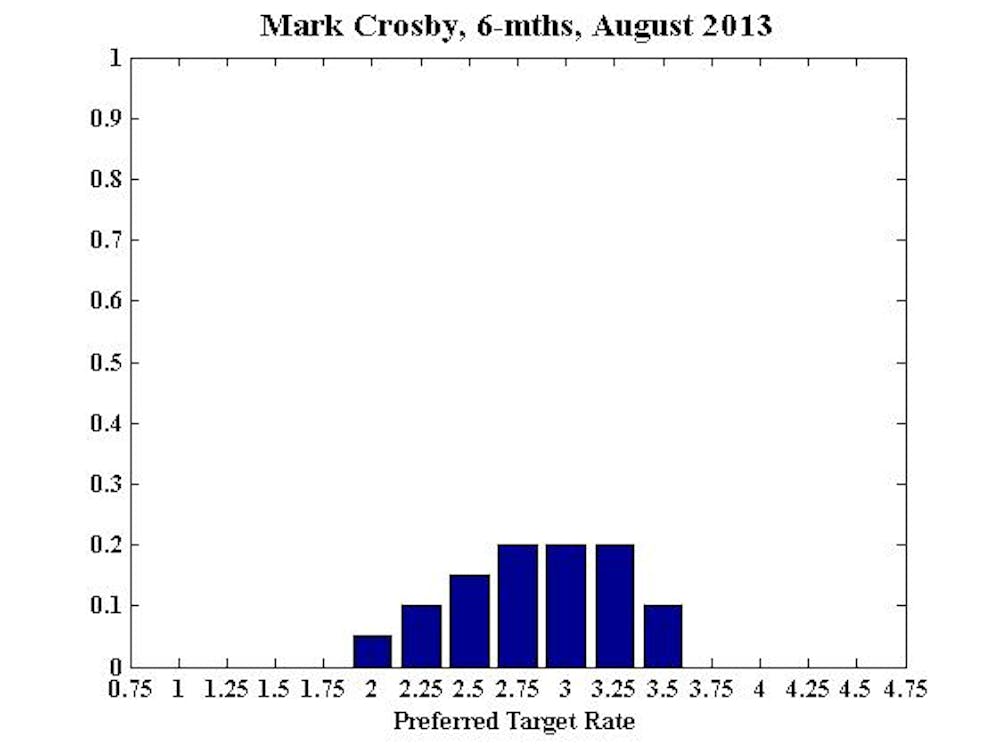

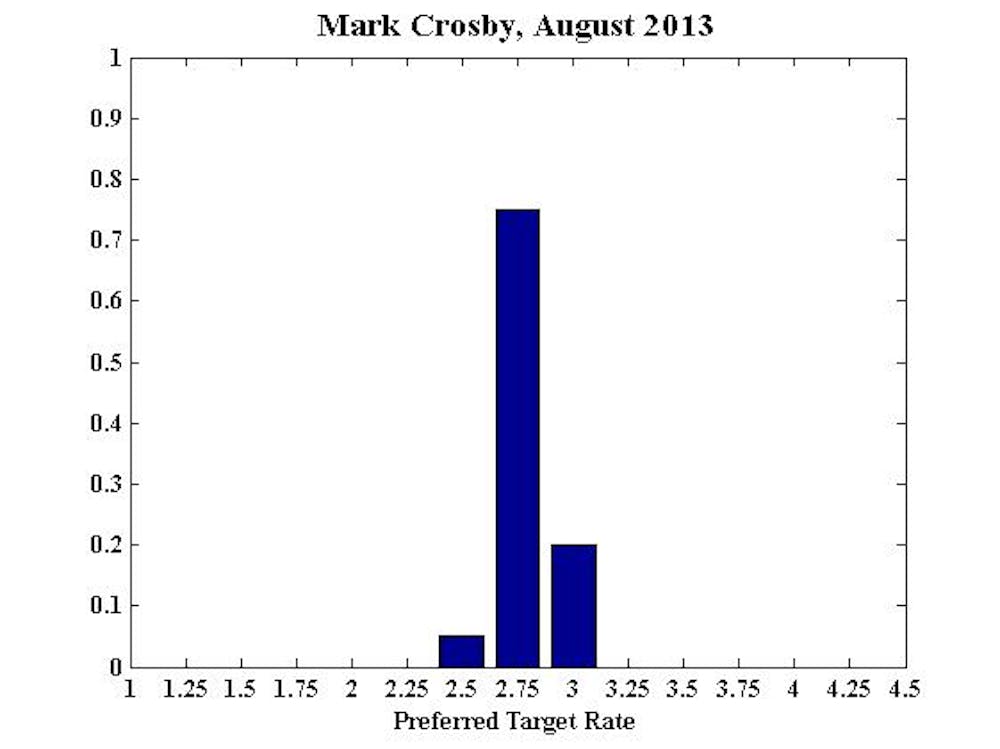

Mark Crosby, Associate Professor, Melbourne Business School:

There are further signs of weakening in the local economy and mixed signals from global economies. However, recent rate cuts would be yet to have their full effect on the local economy, suggesting a “wait and see” approach rather than cutting this month, particularly given helpful weakness in the AUD. In future months the global outlook is still very uncertain, with equal probability of ongoing recovery and slowdown arising from any of a number of key countries.

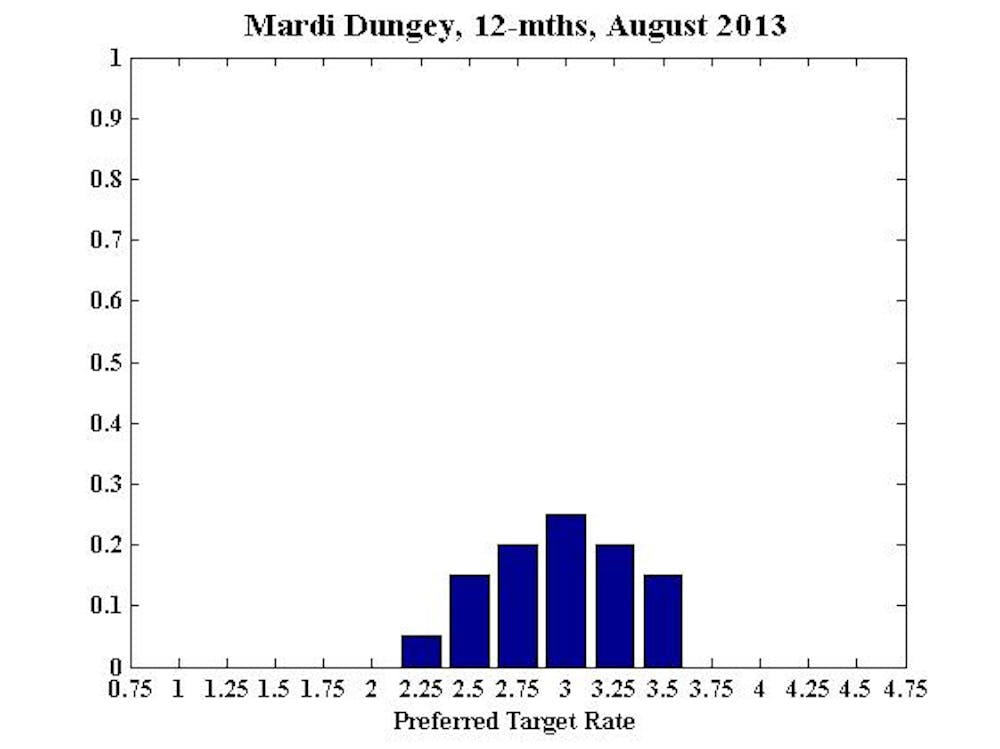

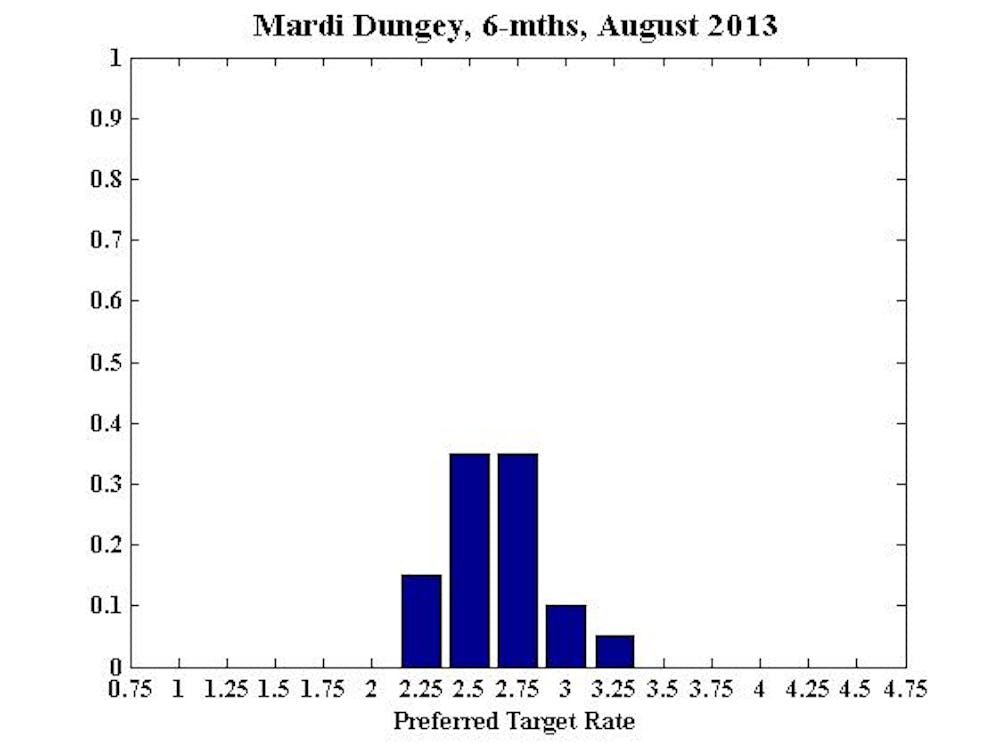

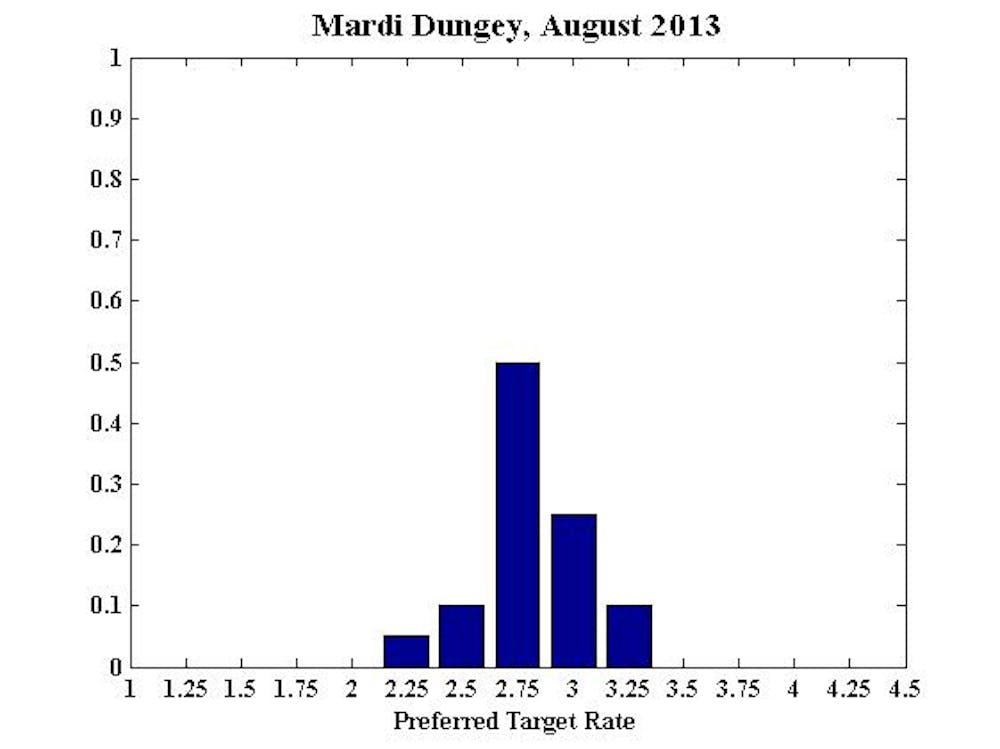

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA:

No comment.

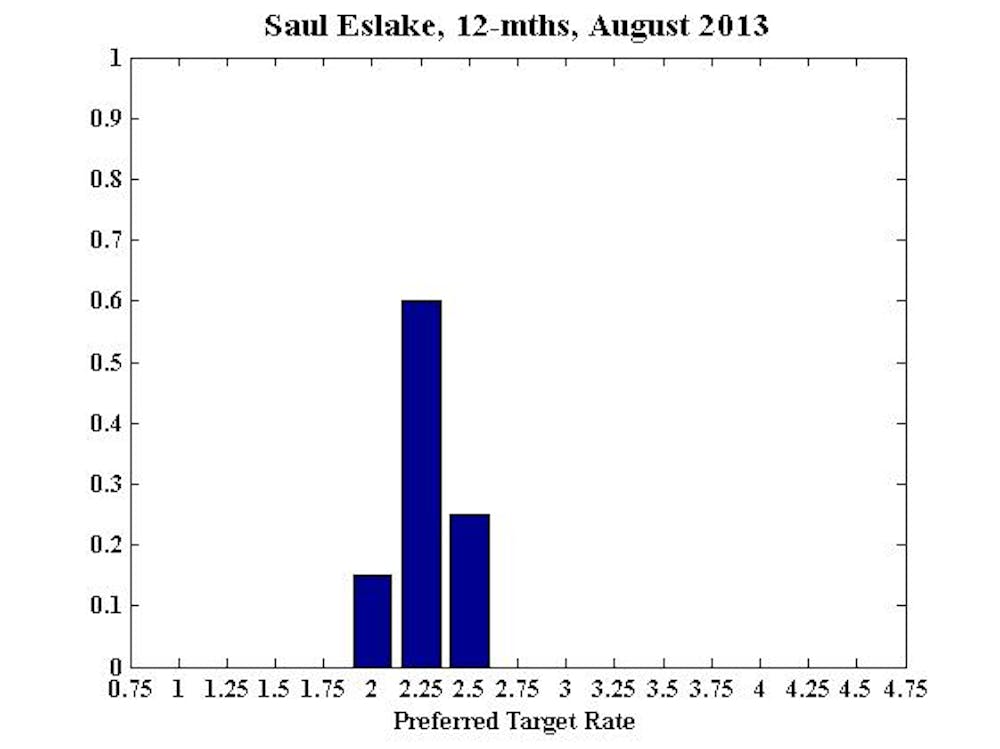

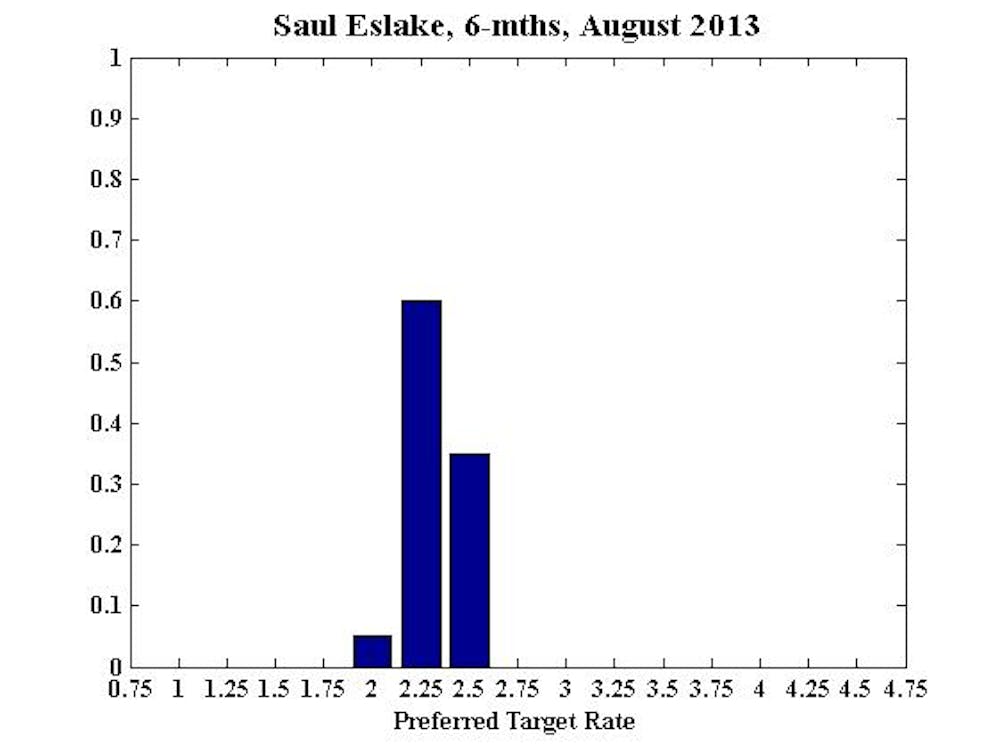

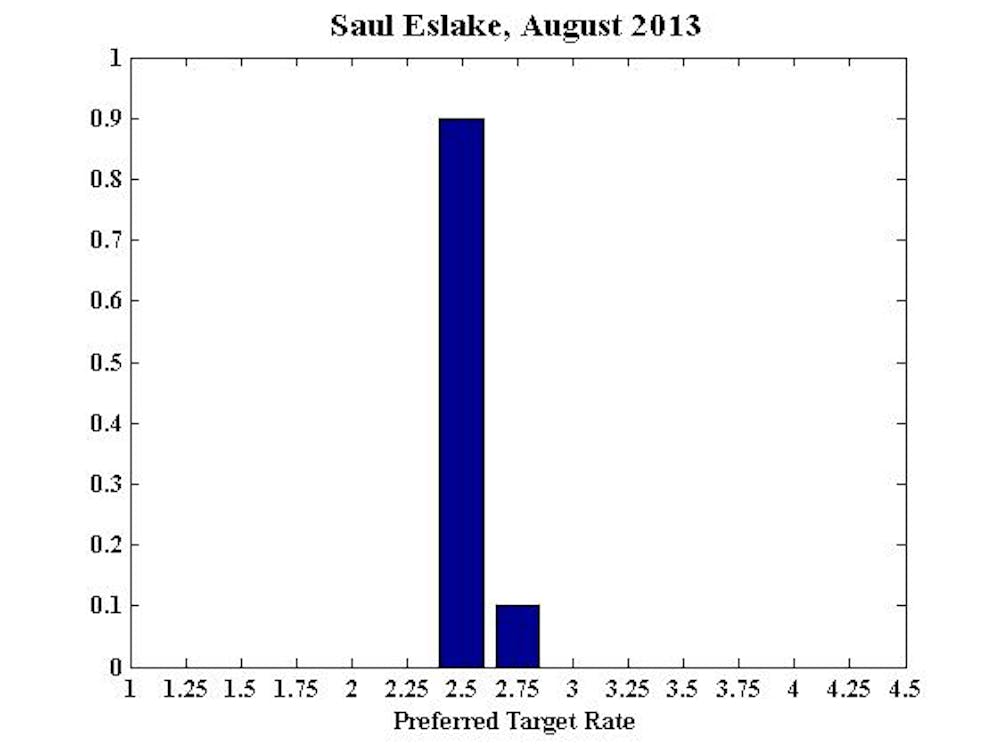

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia:

No comment.

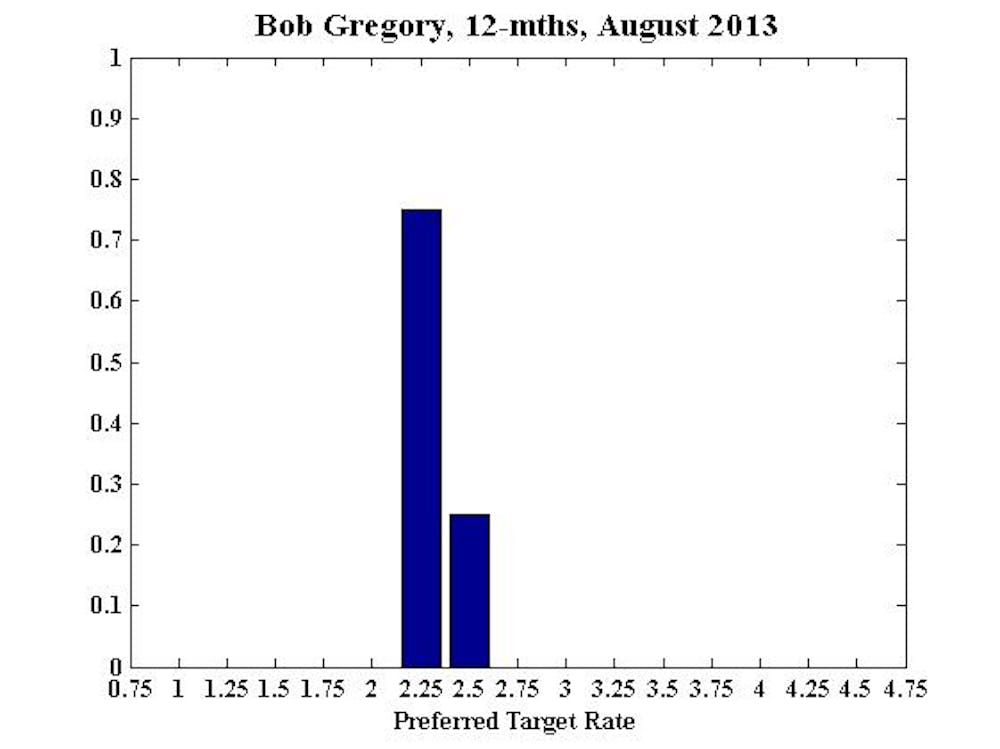

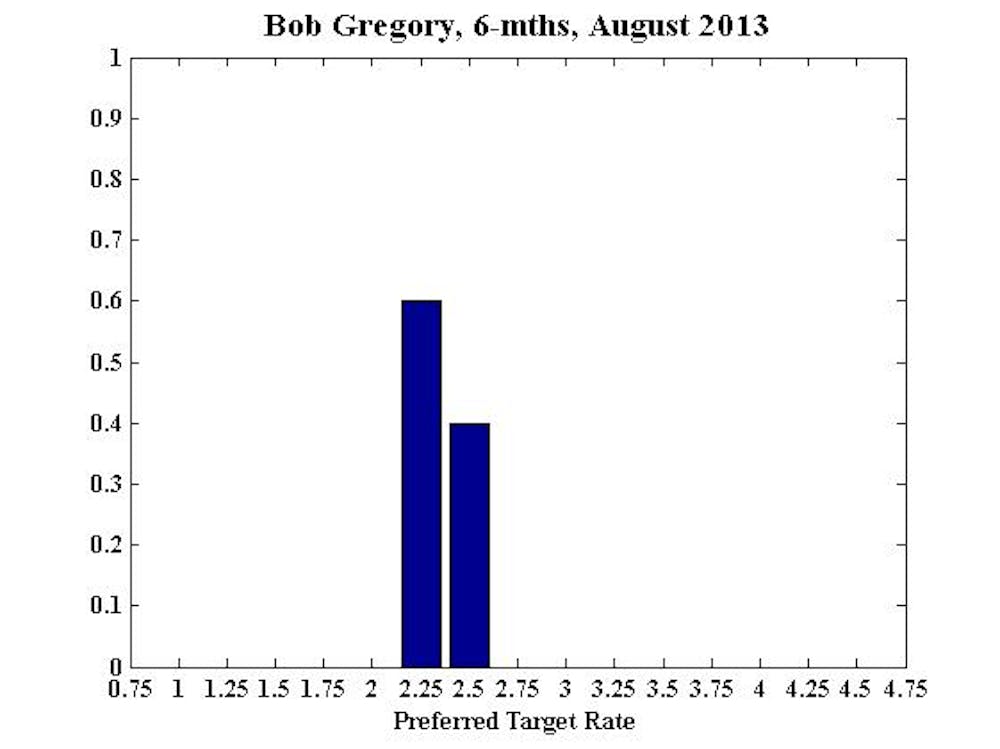

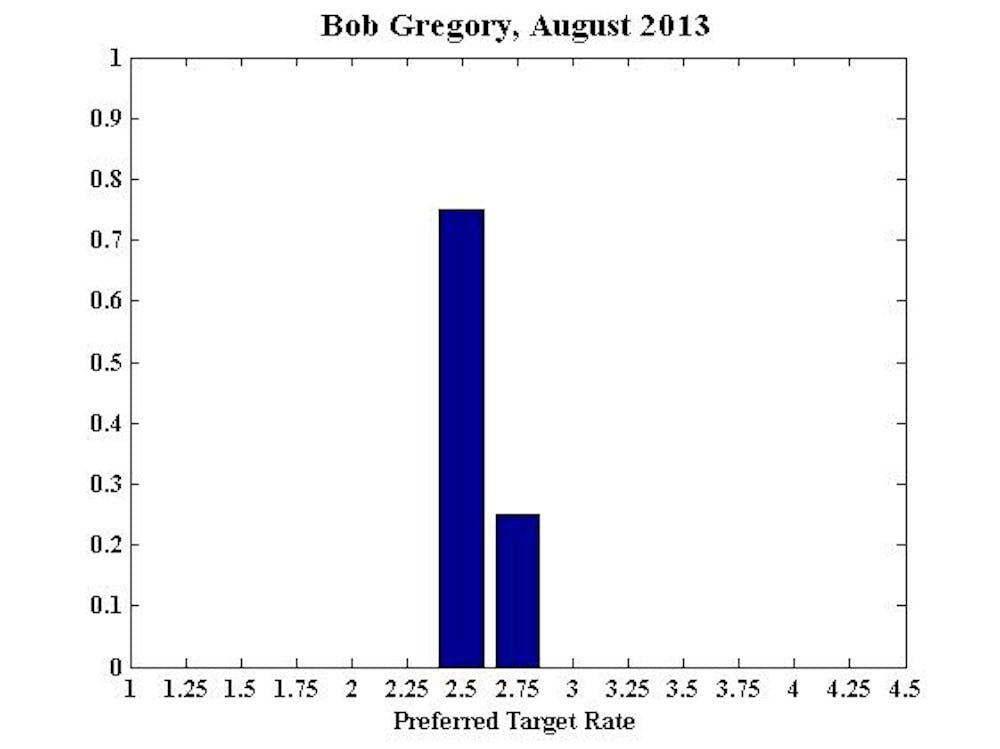

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology:

No comment.

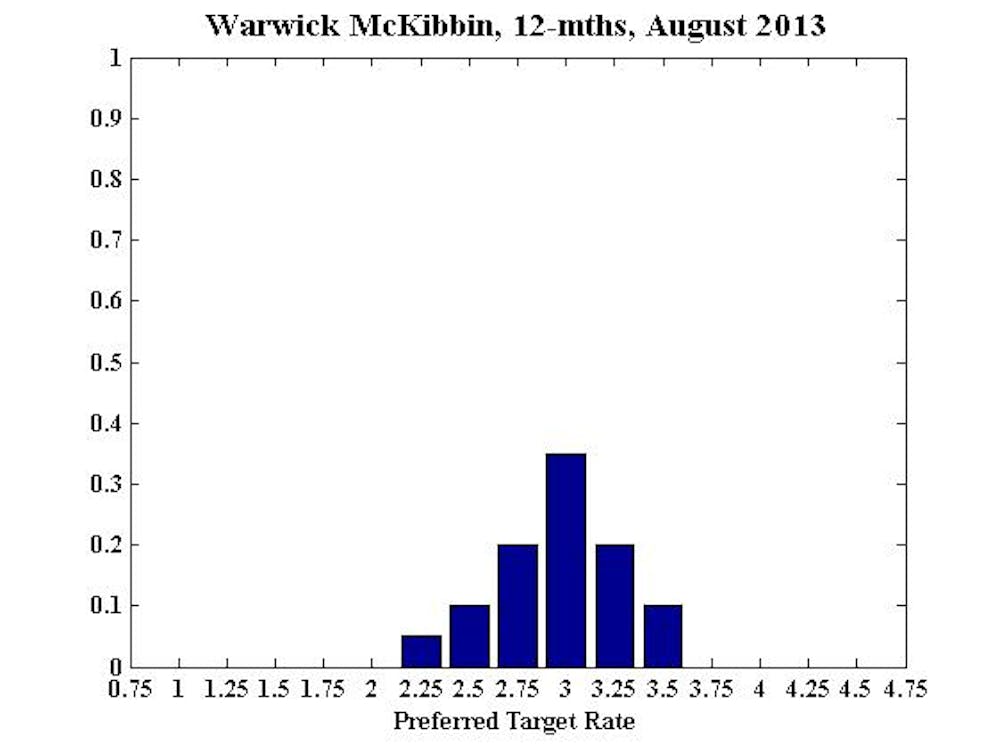

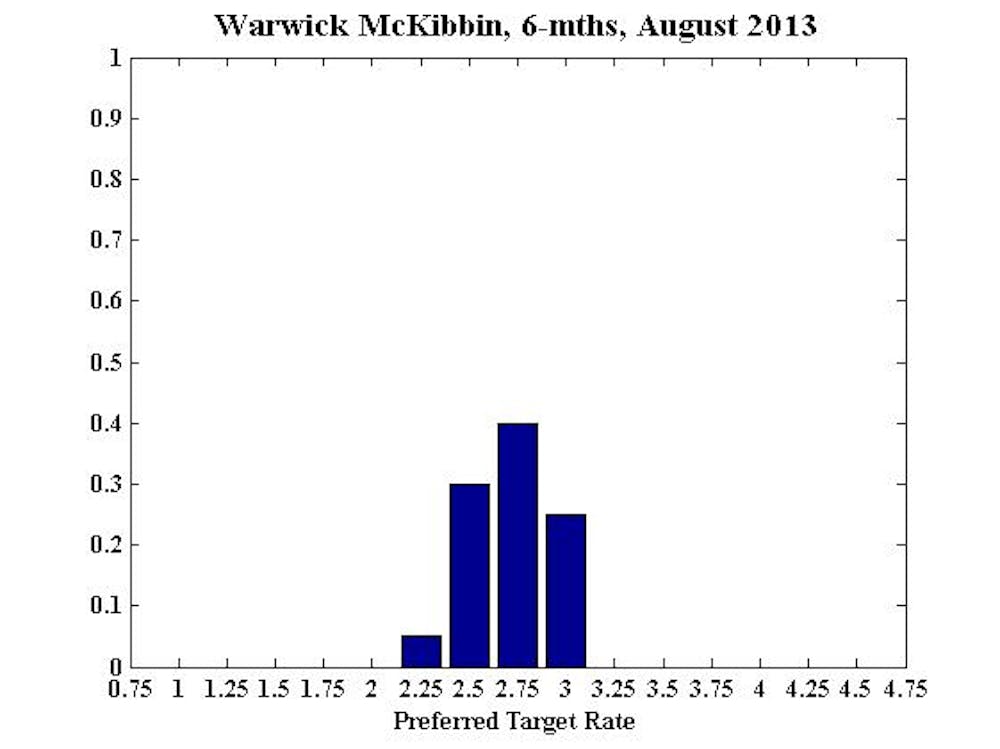

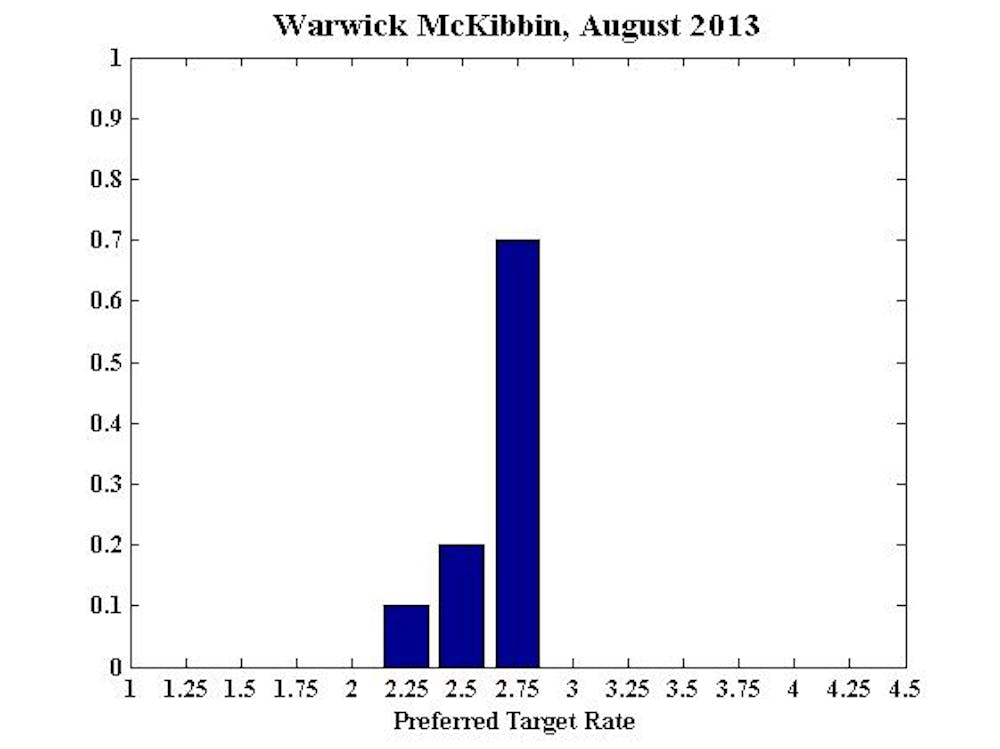

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University:

Although there are clear signs of a change in the drivers of growth in the economy as the resources boom enters a new phase, reducing interest rates any further will do more to misallocate capital than they will stimulate demand. The problem is that fiscal policy through tax changes and infrastructure spending and direct reforms to enhance productivity will do more to rebalance the economy over time than monetary policy can.

The question to be addressed is that without the correct policies elsewhere in the economy, should monetary policy fill the void? My view is that it should not, especially when interest rates have hit such low levels and there is a real danger from the misallocation of capital causing bigger problems over future years. For example, housing pricing have been rising since the trough in May 2012 when you would expected weakness in asset prices as expected income growth drops from the resources boom. Low interest rates are driving asset prices higher than fundamentals. Trying to raise demand from cutting interest rates does not induce investment, especially when weak confidence driven by political incoherence is a driving force in the current Australian economy.

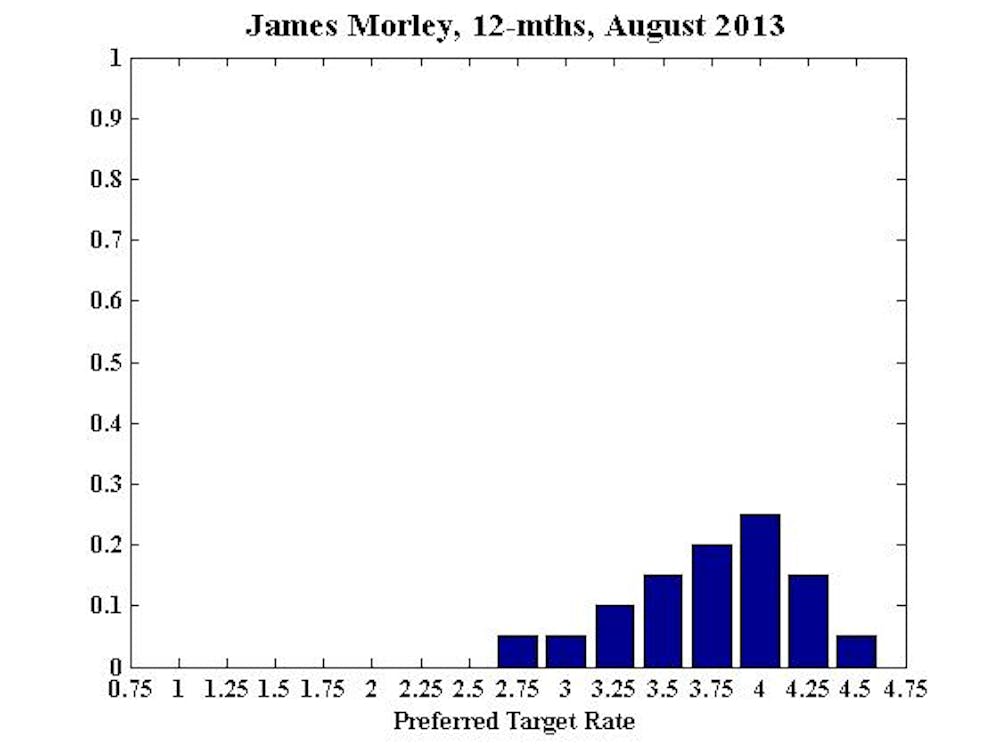

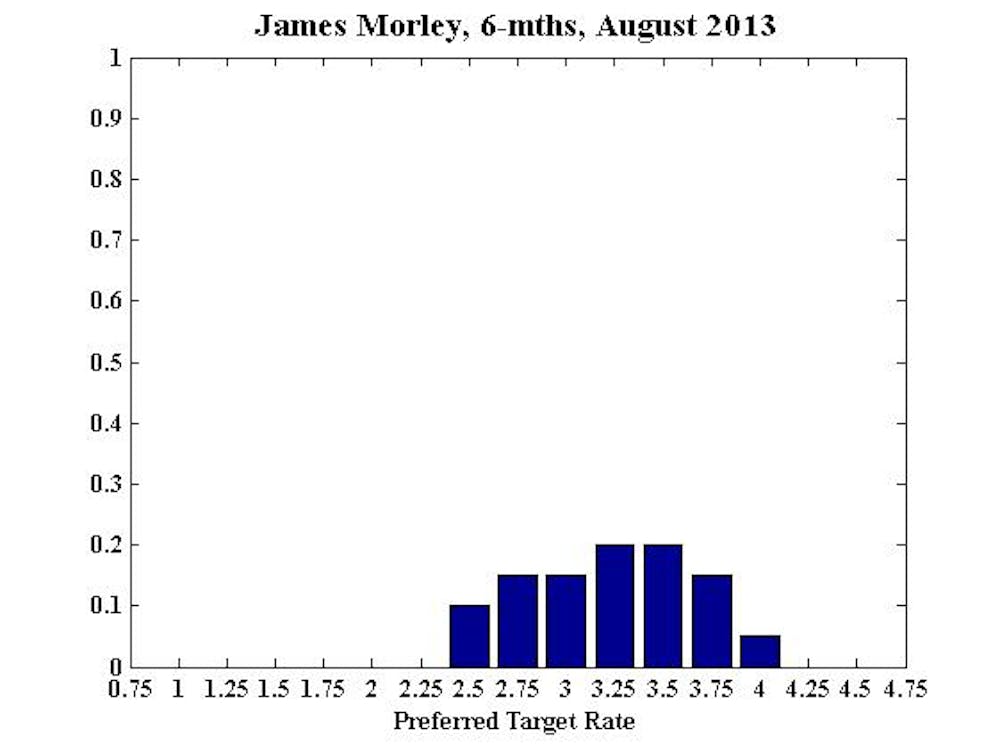

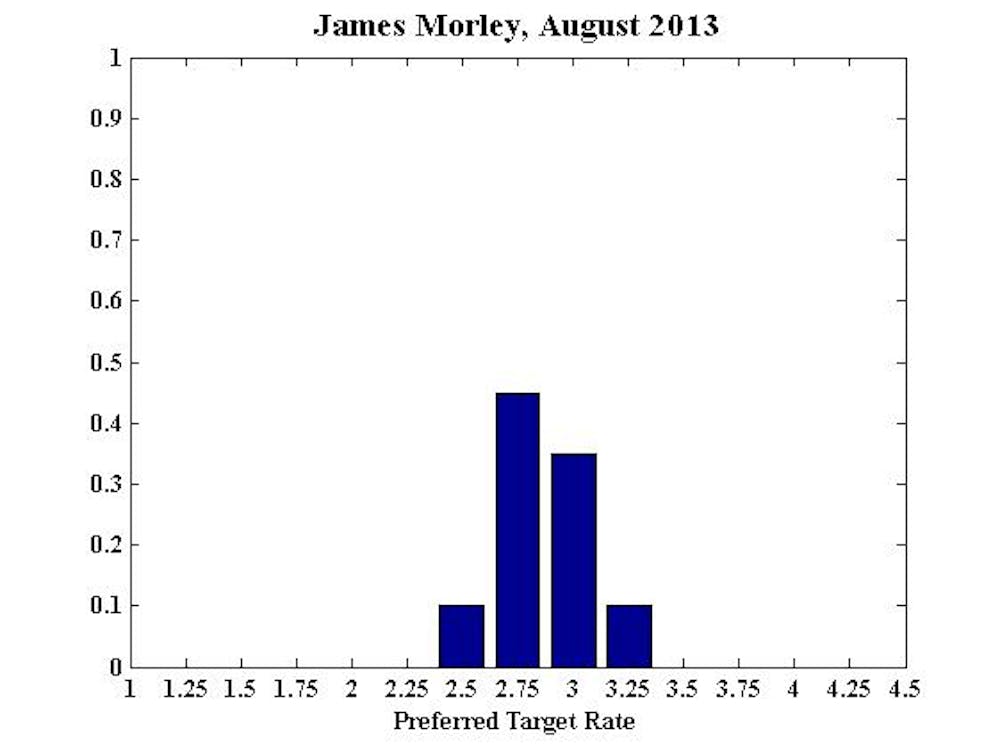

James Morley, Professor, University of New South Wales, CAMA:

Policy should remain accommodative for now, but with an eye on inflation expectations.

Headline inflation in Q2 was 2.4% on a year‐on‐year basis, which is safely within the RBA’s target range. Meanwhile, labour market conditions remain lacklustre, with the unemployment rate creeping up to 5.7% in June.

These domestic conditions provide scope for the RBA to cut the policy rate further, which they will most likely do at the next meeting in response to a weakening outlook for China.

However, it should be emphasised that past cuts in the policy rate are already having their impact on bringing the Australian dollar back towards its long‐run level and this will likely trigger headline inflation to run near the top of the RBA’s target range in the near term. So it is essential that RBA policy focuses on keeping inflation expectations anchored during this period of adjustment in the dollar back to its long‐run level. Also, partially compensating weakness in China, the outlook for the US economy is improving.

Given this background, I continue to believe that real interest rates are already sufficiently low and will need to return to neutral within the next 18 months or so. However, I put more weight than last month on the need for interest rates to remain at these low levels in the coming months due to the weakness in China and the need for a shift in economic activity from mining to other sectors.

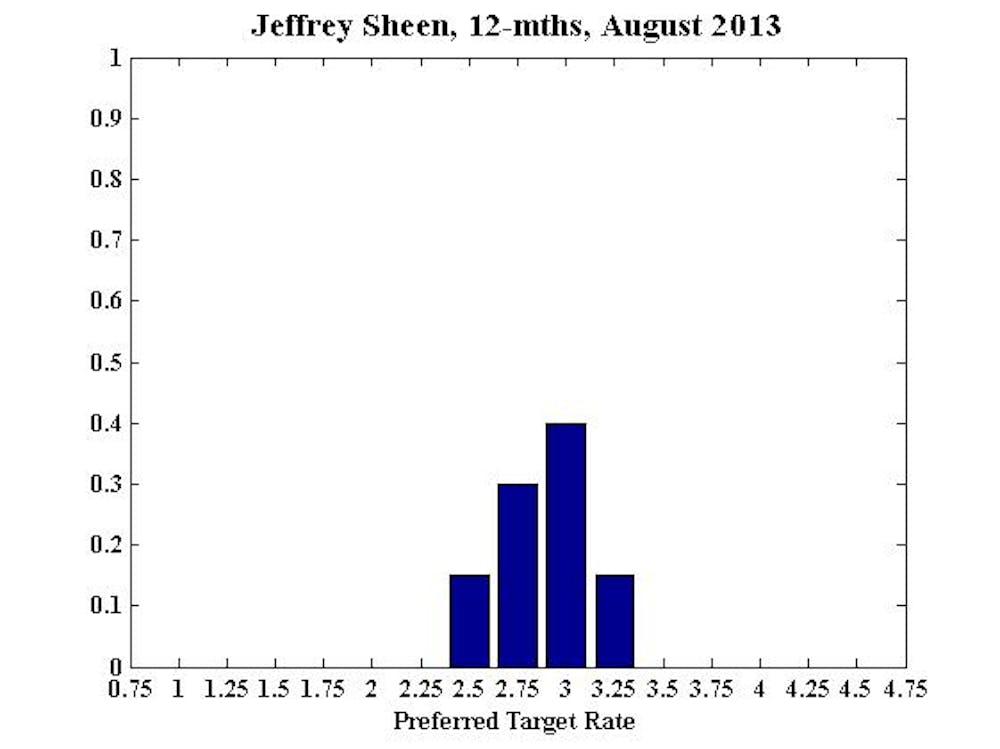

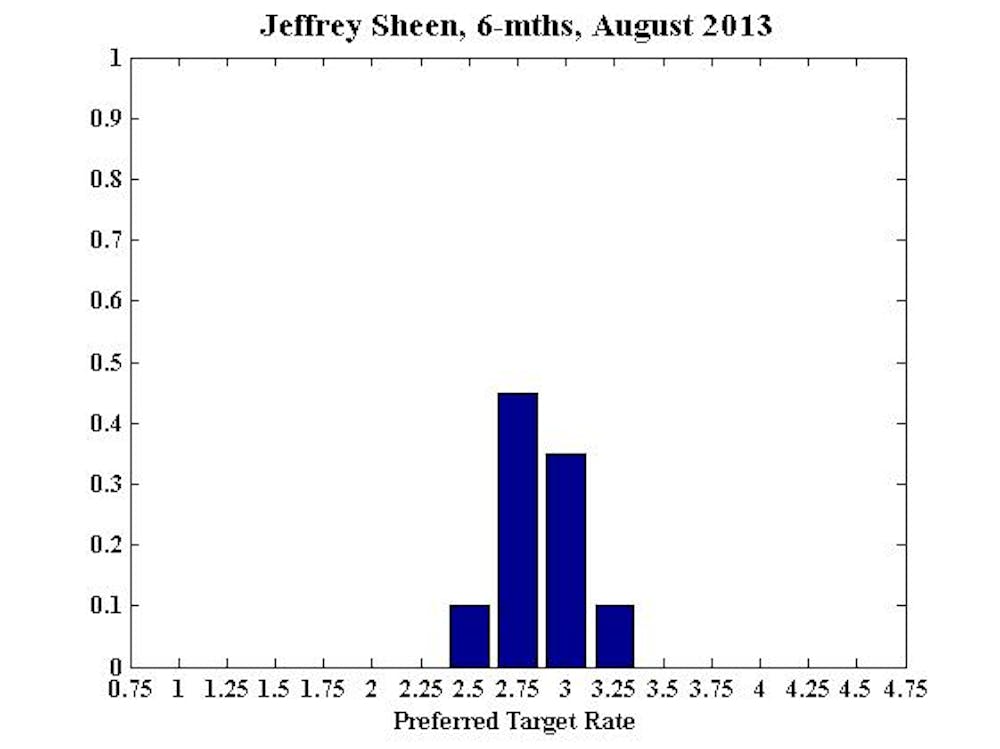

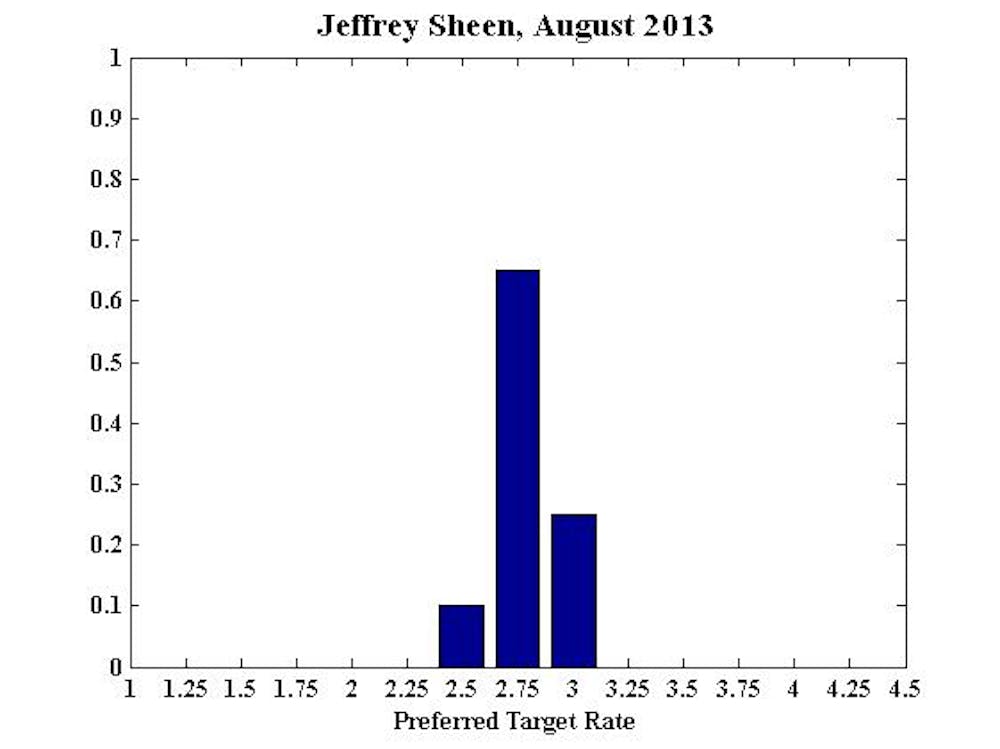

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

The June 2013 Australian labour force figures show a rise in the unemployment rate to 5.7%, but that was due to a rise in participation. CPI inflation remains benign. Business confidence in Australia is stronger in 2013 than 2012. The nominal trade‐ weighted exchange rate has depreciated 12.3% since March 2013, but the real trade‐weighted exchange rate has only depreciated by 2% so far - therefore more time is needed to see what will happen to the real exchange rate. Given these facts, my recommendations are unchanged from last month.

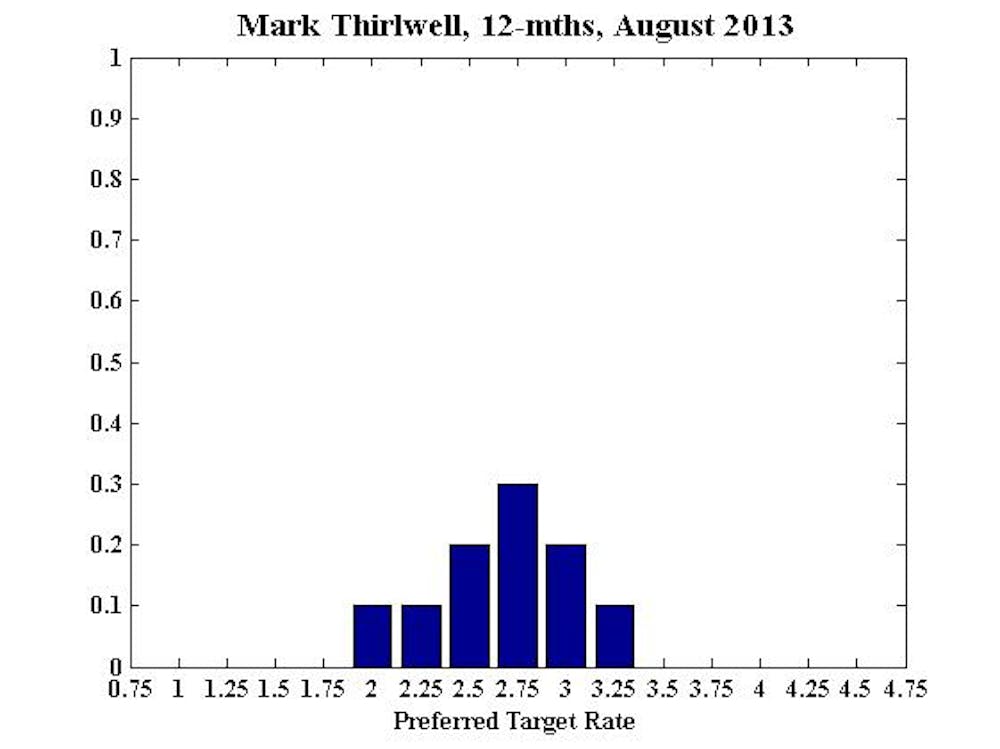

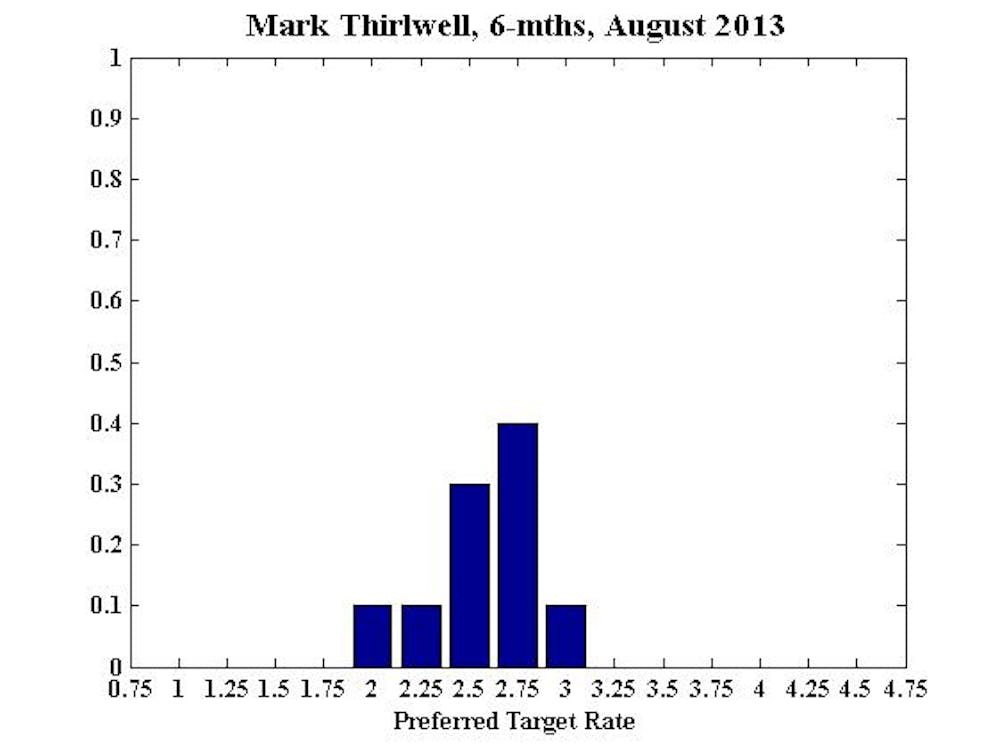

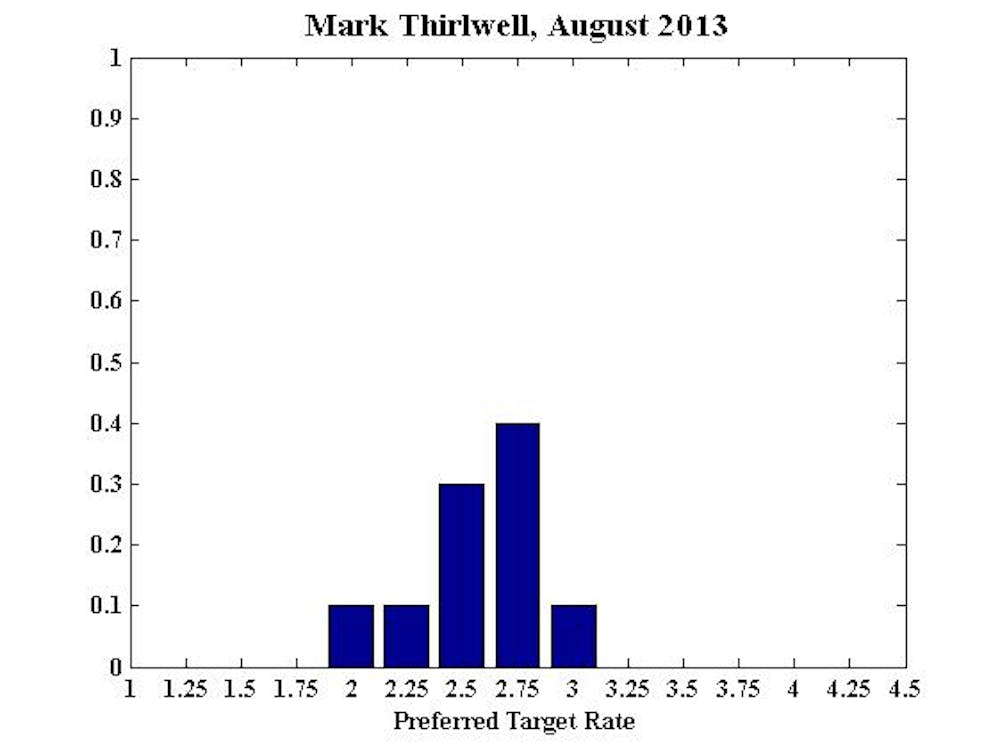

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy:

No comment.