Stock markets all over the world followed China’s lead, plunging into the red and wiping hundreds of billions of dollars off of share values. But, while it’s tempting to lay the blame entirely at China’s door, a look at the global economy and markets shows Western markets have been overvalued and were due a correction.

Equities are risky assets and do not go up forever in straight lines, so corrections can be fast and furious at times. This acts as a useful reminder to investors that stocks are risky assets.

Stock markets in recent years have benefited from market-friendly monetary policies. There have been three rounds of quantitative easing from the Federal Reserve, the Bank of Japan and more recently the European Central Bank. There have for some time been concerns about the outrageous valuation of shares of certain US companies, including Facebook, Twitter, Tesla, GoPro, Netflix and Amazon. Both short-term and long-term interest rates globally have been artificially low for record periods. This unusual era of money printing and low interest rates has boosted asset prices – not just stocks, but also property prices in major towns and cities around the globe.

More interestingly, until this correction, the current bull market has been extremely unusual in that it has been one of the longest ever periods recorded (48 months) without a 10% correction in the S&P 500 index. The green candles in the chart below show the index being up for the month red candles represent it down for the month. The previous longest periods were October 1990-October 1997 (84 months) and March 2003-October 2007 (54 months). The large red candle at the end represents the most recent drop.

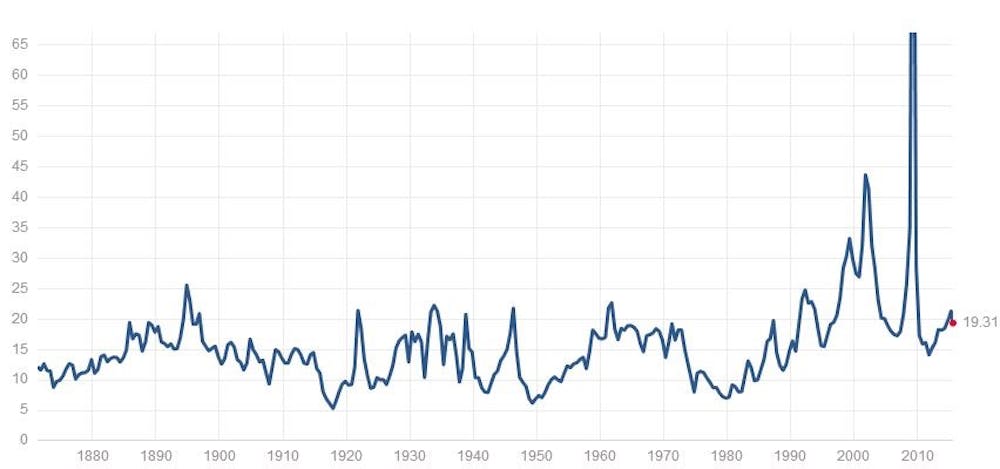

Another sign that US stocks had become overvalued was the fact that the price-to-earnings ratio, which measures a company’s current share price relative to its earnings per share, was approaching 19 to 20 times earnings – historically it averages 16.

If we were to use Robert Shiller’s ten-year cyclically adjusted ratio, the market is even more overvalued at 24 times ten-year average earnings, typically the long term average is 15. By giving a long-term average of earnings, the Shiller ratio better reflects a firm’s long-term earning power.

Prospective ten-year annual returns were likely to be in the region of just 1-3%, which is too low to compensate investors for holding risky assets. The recent fall in US and other stock markets will help improve future prospective US stock returns to a low, but more healthy, 3-5% range.

What about China?

The current sell-off is probably related to events in China – there, the stock market clearly entered bubble territory some months ago. Chinese stocks were rising despite the economy clearly slowing and it was selling at price-to-earning ratios that made no economic sense even if you believed in a 7% growth story.

The Chinese economy is in much greater difficulty than the Chinese government has been prepared to admit to date. That is why recent devaluations of the renminbi have been a catalyst for the recent global stock market correction. It is an admission by the Chinese that their economy is in serious trouble, and represents an attempt to boost the economy through an increase in exports at the expense of some of their competitors.

The Chinese economy is the second-biggest economy in the world after the US, so trouble there also spells trouble for the global economy. The attempts by the Chinese government to prop up their stockmarket were doomed to fail and in recent days this has become very clear.

Closer to home

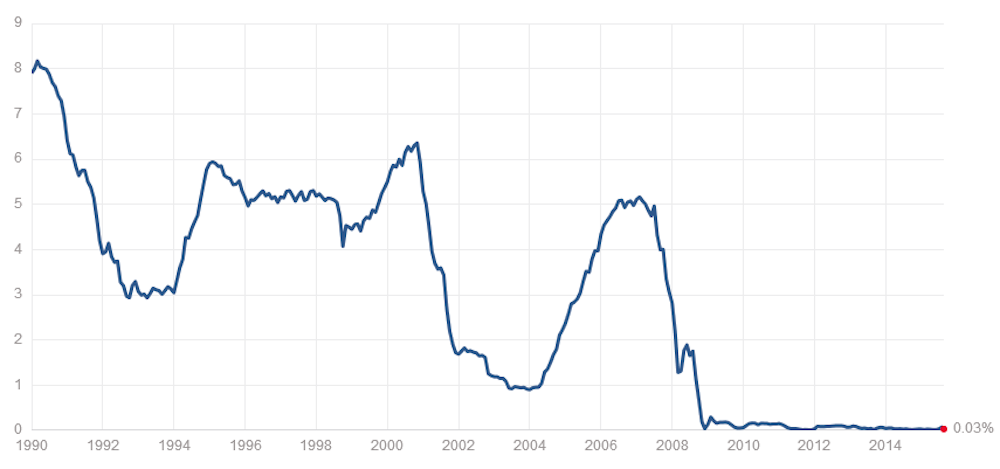

Another reason for the global stock market sell-off is that the US Federal Reserve has been getting closer to raising interest rates from their artificially low target range of 0 to 0.25%. Some market participants are clearly trying to get out of the market before any rise, which is now unlikely to happen in September.

The low interest rates have led to US companies issuing record amounts of debt, not so much to finance future growth but to buy back their own shares to artificially raise their earnings per share. This can work in the short-run, but not in the long run. Raising the leverage (debt-to-equity ratio) of US stocks increases their riskiness and therefore their potential for volatility. This is precisely what we are now witnessing.

The obvious question is what the recent turbulence implies for investors and companies. Should they stay put, or be worried that we are facing a similar crisis to the 2007-08 crash? The good news is that US stocks are nowhere near as overvalued as in the 2001 and 2007 although they should be wary of some of the most obscenely overvalued stocks mentioned earlier.

The Chinese stock market remains overvalued (still some 60 times their earning value) and the economy is in deep trouble. Even US stocks are still highly valued using the Shiller measure. This means global stocks will remain under pressure.

The turbulence we have witnessed is likely to continue, but rallies both ways tend to happen very quickly. Interest rates remain extremely low and will act as a future drag on the market as and when they rise. Companies should also be concerned about a wider slowdown in the global economy hitting their earnings, as China is now the world’s second largest importer of commodities, goods and services.