If you look at the efficiency of the GST – in other words, the amount of economic activity that is destroyed for every dollar you raise – the Government’s latest tax discussion paper says it is just as inefficient a tax as the income tax. It’s much less equitable though. The income tax is paid disproportionately by those further up the distribution and the GST hits those down the bottom. – Andrew Leigh, Shadow Assistant Treasurer, interview with Patricia Karvelas on RN Drive, July 20, 2015.

There are two parts to the Shadow Assistant Treasurer’s statement. In the first part, he simply cites a Treasury report that shows that the GST is as efficient – or inefficient – as the income tax. The second part states that the GST is less equitable as “the income tax is paid disproportionately by those further up the distribution and the GST hits those down the bottom.”

A spokesperson for Dr Leigh said:

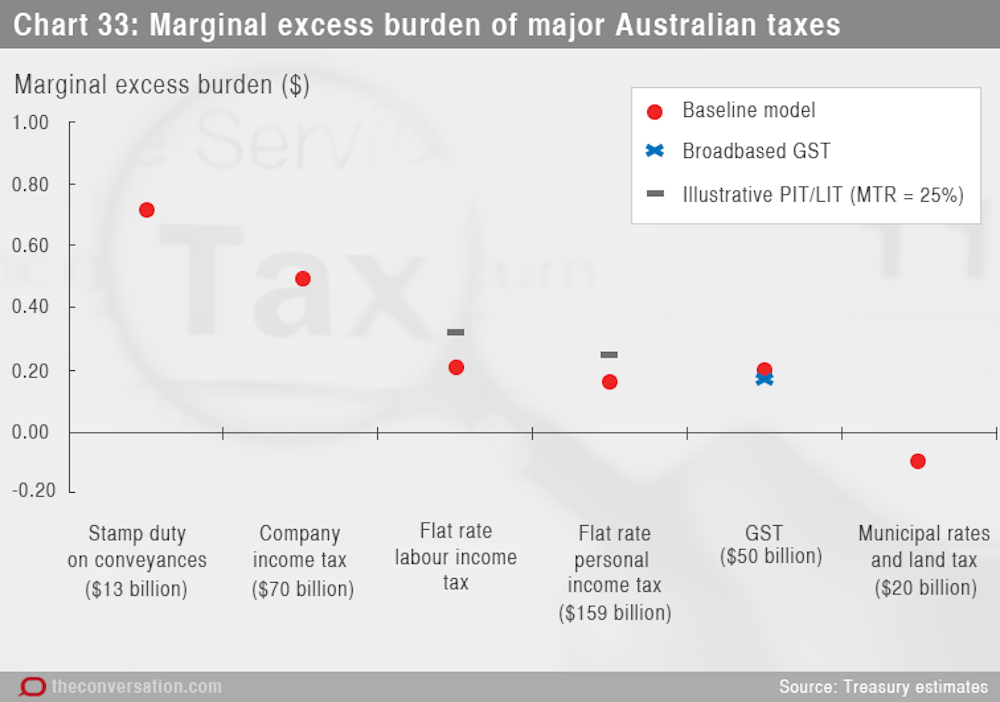

In terms of data supporting the statement, I’d refer you to p.25, chart 2.9 of the government’s Re:think tax discussion paper. This shows that the GST and flat rate labour income tax have an equivalent marginal excess burden, according to Treasury modelling.

What do economists mean by an efficient tax?

There are both direct and indirect costs associated with raising taxes. Direct costs include those that are incurred in the collection of the tax. While direct costs are not insignificant (the Australian Taxation Office employs over 20,000 people), economists consider the indirect costs of taxation to be more relevant. These relate to the distortions that a tax creates.

For example, a tax on apples raises the price of apples to consumers and importantly makes apples relatively more expensive than say oranges. This will lead to consumers buying fewer apples and perhaps more oranges. While the government raises revenue in this process, the tax distorts the behaviour of consumers with possible impacts on the production of oranges and apples.

The efficiency loss is the reduction in welfare, usually measured in dollars, from a consumer buying fewer apples than what she would like to because of the tax, and also any distortions in production.

Is the GST as efficient (or inefficient) as the income tax?

To apply this idea in the current context, an income tax will reduce the remuneration of a worker, relative for example to other non-remunerated activities such as leisure.

Thus, in theory, an income tax could impact on one’s decision of how much to work (or whether to work at all). The GST, however, raises all prices except for goods and services not subject to it.

There lies the conceptual reason for the GST to have a similar impact than an income tax; individuals care not about the dollar amount they receive as wages but rather about the goods and services that they can purchase from their wages over their lifetimes, including savings and bequests.

Let me illustrate this with an example. Here I assume that there is no borrowing or saving, a flat income tax of 10% and a broad-based GST of 11.11%. Consider an individual on a $50,000 income. After paying taxes, she has $45,000 left to spend on goods and services. In this case, $50,000 expenditure on goods and services would include GST of $5,000. That is, both taxes would allow the consumption of $45,000 of goods and services and, as a result, should lead to similar behavioural impact and distortions.

This theoretical argument is borne out by Treasury modelling. Chart 33 from the report is reproduced below. It estimates the “marginal excess burden” (MEB) of different taxes.

The MEB is measure of efficiency loss that captures the decrease in the future ability to spend across the economy per dollar of revenue raised from a tax. These estimates are derived using a long-run economic (computable general equilibrium or CGE) model where households are captured by a representative economic unit.

The chart reports the marginal excess burden of a number of taxes including a stylised personal income tax (represented by a flat rate), a stylised tax on labour income only and the GST. An out-of-model calculation for a marginal tax rate of 25% is presented as an illustration of an average taxpayer in 2011-12. As it can be seen in the chart above, the MEB estimates for the GST and the stylised income tax are nearly identical.

Is the GST less equitable than the income tax?

To answer this question, I need to define a couple of simple terms.

A tax system is regressive if the tax paid, as a fraction of income, decreases with income. A common view of the GST, reflected in the Shadow Treasurer’s statement, is that poorer households pay proportionally more than do richer households. Conversely, a tax system is progressive if the tax paid, as a fraction of income, increases with income. By design, the income tax rate faced by individuals in Australia increases with their income.

The table below uses a survey of households undertaken by the Australian Bureau of Statistics (ABS) to shed light on this question. It shows the average amount of GST, taxes and net income per income quantile for the 2009-2010 financial year. Net income includes pensions, family tax payments, and other benefits, and excludes tax paid on income. As expected, the income tax is clearly progressive. The amount of GST as a fraction of gross income varies considerably less across most of the income distribution, although it is overall decreasing, with the exception of the lowest quintile who pays a much higher fraction of their gross income as GST. Taxes and GST paid as a percentage of average weekly household gross income per income quantile (2009-2010).

However, looking at the fraction of GST paid and income may be misleading as incomes are volatile and spending can be smoothed via borrowing and savings. To take this into account, I report below the amount of GST paid as a fraction of total expenditures, which is likely a better measure of the level of spending that households can sustain. Once again, the lowest quintile pays substantially more GST as a fraction of expenditures, but there is a small variation for the other groups.

Verdict

The Assistant Shadow Treasurer is correct that the efficiency of the GST as a tax is similar to that of income tax. He is also correct that the income tax is more progressive than the GST and that the GST hits disproportionally those in the bottom of the income distribution.

However, while technically the data above suggests that the GST is a regressive tax, the difference between the fraction of income or expenditures paid in the form of GST is small amongst the various quantiles of the income distribution, with the exception of the poorest.

Review

I concur with the comparative distribution effects of the GST and personal income tax.

In the case of relative efficiency effects, because the income tax in practice falls on capital income as well as labour income and because it has a progressive rate schedule, it has additional distortion costs to those assessed with a flat rate tax on labour income considered in the FactCheck.

First, income tax applies to capital income (for example, stock dividends) as well as to labour income. Capital income tax distorts aggregate saving versus current expenditure decisions. The hybrid Australian capital income taxation of different saving options distorts the composition of savings between one’s home, other property, bank deposits, superannuation and so forth.

Second, while the GST has a flat rate of 10%, the income tax rate schedule is a progressive one with marginal rates from zero to 49%. With efficiency costs increasing more than proportionately with the tax rate, a progressive tax rate generates larger distortions on average than a flat rate tax.

Accepting the comparative efficiency and distribution effects of the GST and income taxes, most sensible suggestions for taxation reform which involve a more comprehensive base and/or higher rate GST to reap efficiency gains from a tax mix change also propose that some of the GST revenue gain be recycled as higher social security rates and a lower but more progressive income tax rate schedule to maintain the effective purchasing power of the poor. – John Freebairn

CORRECTED: An earlier version of this article mislabelled the last two rows in the table titled “Taxes and GST Paid”. The last two rows were labelled “GST/Gross income (%)” and “Income tax/gross income (%)”, but have now been changed to “GST Net income (%)” and “Income tax/net income (%)”.