Repealing Obamacare was central to both Donald Trump’s, and the Republican party’s, policy platforms. The President-elect has since softened his stance and there are several Republican proposals to replace Obamacare with a more viable alternative.

Obamacare involves establishing state insurance marketplaces (or exchanges) on which people buy insurance. These are like price comparison websites on which people can buy subsidised insurance. People can also get insurance through their employers or directly from insurers.

All people must have insurance (under threat of penalty) and insurers cannot refuse people with pre-existing conditions or charge them more. Most state marketplaces work independently, with different plans available to residents of different states. In offering insurance, companies must spend at least 80% of premiums on healthcare and quality improvement.

Key criticisms of Obamacare have included rising premiums and fewer available policies. Repealing Obamacare without a replacement could have “devastating consequences”, according to the Iowa Insurance Commissioner. People’s insurance would be disrupted and insurers would face losses as sick people rush to have procedures before their cover ends.

So what has led to Obamacare’s problems, what needs to be addressed and what might alternatives to Obamacare look like?

Rising premiums, less choice

Obamacare has become decreasingly popular in recent years. Insurance premiums will reportedly rise by 25% in 2017. Subsequently, almost half of exit poll respondents in the US election thought Obamacare “went too far”. Insurers too argue they are losing money on Obamacare. A 2016 McKinsey & Co report indicates insurers lost money in 41 states on Obamacare exchanges in 2014.

Insurance companies too are withdrawing from Obamacare marketplaces and instead choosing to focus on employer sponsored plans. So, some states also have fewer insurance options. UnitedHealthcare is withdrawing from most Obamacare marketplaces and remaining in only a handful of states in 2017. Aetna will stop offering insurance in 11 of the 15 states it serves.

The Congressional Budget Office indicates subsidies from the government to consumers will amount to US$43 billion in 2016. These subsidies increase as premiums increase, squeezing health care budgets further. This is clearly not sustainable given the existing budget deficit.

The Republican party has detailed replacement plans for Obamacare. A Better Way and the CARE Act both maintain key features, including that insurers cannot refuse people with preexisting conditions (the preexisting condition rule).

However, they both propose increasing premiums for people who have not maintained continuous coverage. The idea is to encourage people to sign up while healthy, the first issue that an Obamacare replacement needs to address.

1. Get healthy people into insurance

Efforts to get healthy people into insurance, and to reward them for keeping up their policies, are intended to enable companies to insure sick people without going bankrupt.

Obamacare’s current “individual mandate”, which states that everyone must buy insurance or face a penalty, is meant to facilitate this.

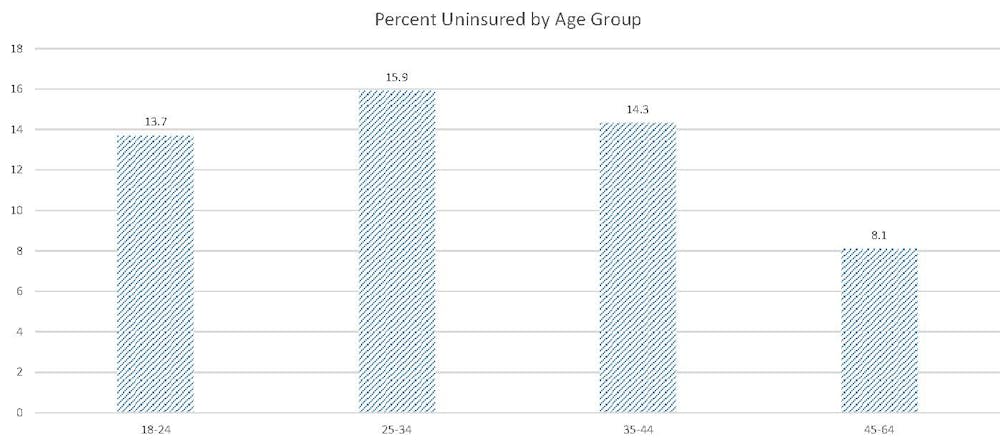

However, too many healthy people pay the penalty rather than buy insurance. While the overall percentage of people without insurance decreased between 2012 and the first quarter of 2016, this varied across different age ranges. As the graph shows, in percentage terms, more 25-34 year olds are uninsured than are 35-44, or 45-64 year olds. Thus, in percentage terms, older (generally sicker) people make up an increasing portion of enrolees, increasing risk and forcing companies to charge higher premiums to remain solvent.

President-elect Trump seems to want to keep the preexisting conditions component. However, this could be unviable given the current lack of young, healthy, enrolees. The government would need to enforce the individual mandate either through increased penalties for people not taking up a policy or to persuade people to sign up.

Australia and Republican proposals could give some guidance. Australia’s Lifetime Health Cover program, as well as the previously mentioned alternatives, Better Way and CARE Act, allow insurance companies to charge higher premiums to people who have not maintained continuous coverage.

The Republican proposals also reduce the required level of care insurance companies must offer, thereby reducing premium costs and attracting more people to insurance. The CARE Act forces people who do not enrol into a default low cost insurance program, which provides coverage for only a limited range of conditions.

2. Address fragmented marketplaces

Insurance companies can sell insurance via employer based plans, on Obamacare marketplaces and/or directly to consumers. A total of 155 million people under 65 get their insurance from employment based plans; 12 million buy their insurance on the marketplaces; 9 million buy it outside the marketplaces (directly from insurers).

Compared with those on employer-sponsored plans, people who buy insurance on the exchange tend to qualify for government subsidies and tend to be sicker and poorer. The Blue Cross Blue Shield reports new enrolees after Obamacare tend to have higher rates of some diseases and use more medical services.

Insurance companies can mitigate having to insure excess numbers of sick people on Obamacare marketplaces by focusing on employer-linked plans. This reduces choice on the marketplace.

Some states have tried to address this problem through incentives and penalties. Alaska has a reinsurance type program to help insurers meet the costs of high cost patients. Nevada mandates insurers participate in its exchange. Australia too has a reinsurance arrangement to help insurance companies burdened with bad risks. The Better Way proposal would have a US$25 billion high risk pool. Such incentive measures could help to increase exchange participation without risking insurance companies’ solvency.

Trump potentially has a similar policy. His policy platform refers to establishing “high-risk pools to ensure access to coverage for individuals who have not maintained continuous coverage”. This might help to alleviate the stresses created by retaining the preexisting condition clause.

3. Allow interstate purchases

People can generally only buy insurance form their home state’s marketplace due to the McCarran-Ferguson Act (1945), which allows states to regulate health insurance plans within their borders.

Some markets have few insurance companies, and reportedly, will only have one marketplace offering in 2017. This gives little choice for their residents.

Trump’s solution is to allow “people to purchase insurance across state lines, in all 50 states”. This will not solve the issue of healthy people going without insurance and increasing the risk pool, but will increase choice. Increased competition also risks further eroding any profitability for insurance companies.

4. Relax the 80/20 rule

The 80/20 rule says insurance companies must spend at least 80% of all premium revenue on medical care and actions to improve the quality of care; they must spend at least 85% when selling insurance to large groups.

The 80/20 rule can be problematic because there’s a debate about whether the government is entitled to regulate companies’ profitability.

The rule also limits competition in individual marketplaces. This is because a firm can participate in a marketplace only if it can keep its overheads low enough to spend 80% of revenue on health care. This is possible only if both (1) it has relatively low costs, and (2) it has enough customers to generate economics of scale. Small insurers lack economies of scale, so could not participate.

Insurers unsure about whether a marketplace will be profitable will be deterred because there is no guarantee they could retain enough premium revenue to remain solvent.

The government might not want to enable rampant profiteering. However, relaxing the 80/20 rule could encourage more insurers to enter the insurance marketplaces.

Where to from here and will Trump’s position help?

Trump’s Obamacare position is evolving and his policy platform is vague. He states that he intends to “repeal and replace” Obamacare yet the form of that replacement is unclear.

Trump indicated he supported the rule that insurance companies must accept people with preexisting conditions and to allow adult children to remain on their parents’ insurance policies. Trump also wants to increase choice by allowing people to buy insurance across state lines, which does not itself solve the problem of unhealthy people flocking to Obamacare marketplaces.

Retaining Obamacare is untenable unless Trump retains, and enforces, the individual mandate. However, his policies regarding the individual mandate are unclear. The obvious solutions are to increase penalties for noncompliance and imposing a loading for failing to maintain continuous coverage. A reinsurance plan, similar to that in Australia, or in Alaska, might help mitigate the impact of high-risk customers.

Ultimately, the choice comes down to enforcing the individual mandate more stridently, potentially allowing higher premiums for those who fail to maintain continuous coverage, or watching Obamacare fail.