In California, people fear the “big one” – an earthquake of such magnitude that it could wipe the state off the map. They look nervously at the intense seismic tremors from previous earthquakes and fear it is only a matter of time. The financial markets have an equivalent to these tremors: flash crashes are temporary market spikes that are a feature of modern automated trading. So far, they have passed quickly and normal business has resumed. Yet that may not be the pattern in future. The worry is that one day soon, a flash crash could bring the global economy to its knees.

Rewind to January 2, when Apple issued a profit warning, largely thanks to softer demand for Apple devices in China. The Australian dollar, used by traders as a proxy for the Chinese economy, suddenly tumbled 3.5%. Something similar happened with the Japanese yen in the opposite direction. By the end of the Asian trading session, these shifts had rebounded. Yet market watchers were in no doubt: another “flash crash” had just struck.

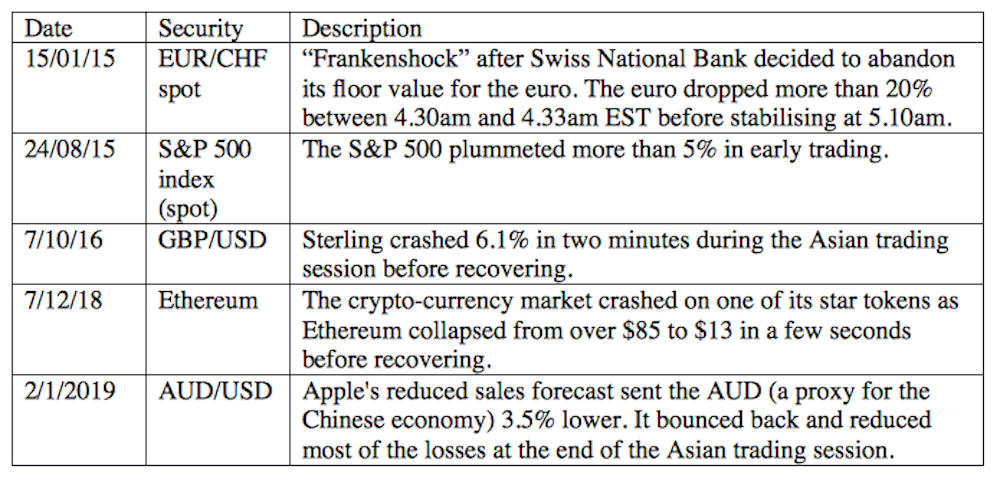

Flashes big and small

The first flash crash that made headlines infamously took place around 2.30pm to 3.00pm Eastern Standard Time on May 6, 2010. The Dow Jones Industrial Average suddenly tanked 10%, causing spectacular upheaval in the US futures and spot markets. A subsequent official report blamed automated trading, often known as algorithmic trading, for starving the market of willing buyers.

What saved the day was the triggering of a circuit breaker on the Chicago Mercantile Exchange, the world’s largest futures market. This stopped the market for just five seconds, but it was enough time for automated traders to discern that prices were artificially low. They duly sent manual purchases which cumulatively helped the markets to recover by driving up prices again.

Flash crashes have since become a more regular occurrence. There have been thousands of mini flash crashes, moving a market by a relatively small amount, but also more major incidents. The highlights are listed in the following table, including the crash of January 2, 2019. This doesn’t include the flash crash of December 5, 2018, which saw a sudden plunge in S&P 500 E-mini futures, the most traded futures contract in the world. In just three minutes after the day’s opening, these futures plunged 2.5%, only to rebound thanks to another circuit breaker.

So what is going on? Since around the turn of the century, financial firms have increasingly relied on algorithmic trading. It enables them to take advantage of the superhuman abilities of computers to process huge volumes of data at high speeds. Different operators use different strategies and time horizons, ranging from long-term investments by pension funds and insurance companies to short-term buying and selling by banks and brokers.

Problem predators

Most algorithmic trading is perfectly legitimate – indeed, it makes markets more efficient by increasing trading activity. It becomes problematic where it becomes predatory – manipulating other traders by giving a false impression of market demand.

Most predatory strategies involve posting then cancelling orders to buy or sell a security at a better price. Let’s say that a trading algorithm wants to sell 400 Microsoft shares at US$10 per share. The market order book, which records buyer demand, shows outstanding bids for only 50 shares at that price. This could be because, say, most trading is currently taking place at US$9.98.

To try and remedy this, our trading algorithm places a dummy bid for 450 Microsoft shares at US$10 each. Other would-be buyers are lured to place orders at the same price. This increases the number of share orders from, say, 500 to 900.

All this is happening in microseconds, so that none of this share demand has yet found a seller. Our algorithm knows exactly when its 450 order will be satisfied, and cancels just before. Instead, it instantaneously sells 400 shares at US$10 each to the buyers it attracted to the market. This is called spoofing. It was considered legitimate in the days of manual trading, but automated trading speeds have made it too effective. The same goes for other predatory strategies such as algorithm sniffing, quote stuffing, latency arbitrage and marking the close. Yet with more than half of US shares trading automated, for example, the worry is that there is still much predatory behaviour going on.

The reason these can cause or exacerbate flash crashes is that they can encourage herd behaviour – a rash of panic selling, say. This can prompt a particularly sharp price swing at a time when traders are staying out of the market because prices are too volatile – potentially spreading to other markets due to global interconnectedness, as traders begin to think that other prices must be wrong as well.

So far, flash crashes have coincided with a relatively calm bull market. But many now believe the tide has turned. The FTSE100, for example, registered its biggest fall in a decade in 2018. In a more depressed market, where there’s inevitably more volatility and traders are more downbeat, the worry is that flash crashes are more likely to get out of hand – possibly causing contagion around the world.

How we should respond

Circuit breakers have become much more widespread since 2010, but they don’t stop flash crashes. They merely pause trading – and if traders are feeling downbeat anyway, they may simply carry on panic selling (or buying) when the market reopens. Circuit breakers are also less helpful with securities traded in more than one market, such as currencies.

One alternative answer is more controlled exchanges which are friendlier to manual traders, such as the Investor Exchange (IEX) in the US. The IEX, established in 2012, offers simultaneous market access to all participants by imposing a 350 microseconds delay on trades. After only a few years of trading, the IEX accounts for about 2% of US securities trading. Faced with this new competitor, the New York Stock Exchange recently introduced a similar delay, but only for shares of small and mid-sized companies.

Elsewhere, the Tokyo Stock Exchange has implemented a system of trading checks to discourage manipulative order cancellations. The Italian exchange introduced a 0.02% levy on order cancellations beyond a particular threshold. France and Finland have launched similar systems.

Such interventions definitely reduce the risk of flash crashes. But even put together, only a relatively small proportion of the securities trade has been affected. The system as a whole remains gravely at risk.

With monetary policy tightening around the world; a trade war between the US and China; and stocks still generally expensive, it’s not surprising sentiment has been weakening. Having had two significant flash crashes in less than a month, the Bank of England’s recent warnings to “brace for future crashes” seem timely. Unless market regulators do more to mitigate these risks, there could be big trouble ahead.