If you wonder why there is so much antipathy towards the Renewable Energy Target from the electricity utilities, all you need to do is look at what is happening to demand for poles and wires electricity.

Across the eastern seaboard served by the National Electricity Market (NEM) demand is collapsing and heading towards territory not seen since the last millenium. Another few years on current trend and the industry will be in chaos. The last thing utilities want now is new capacity enforced by government regulation into an already grossly oversupplied market.

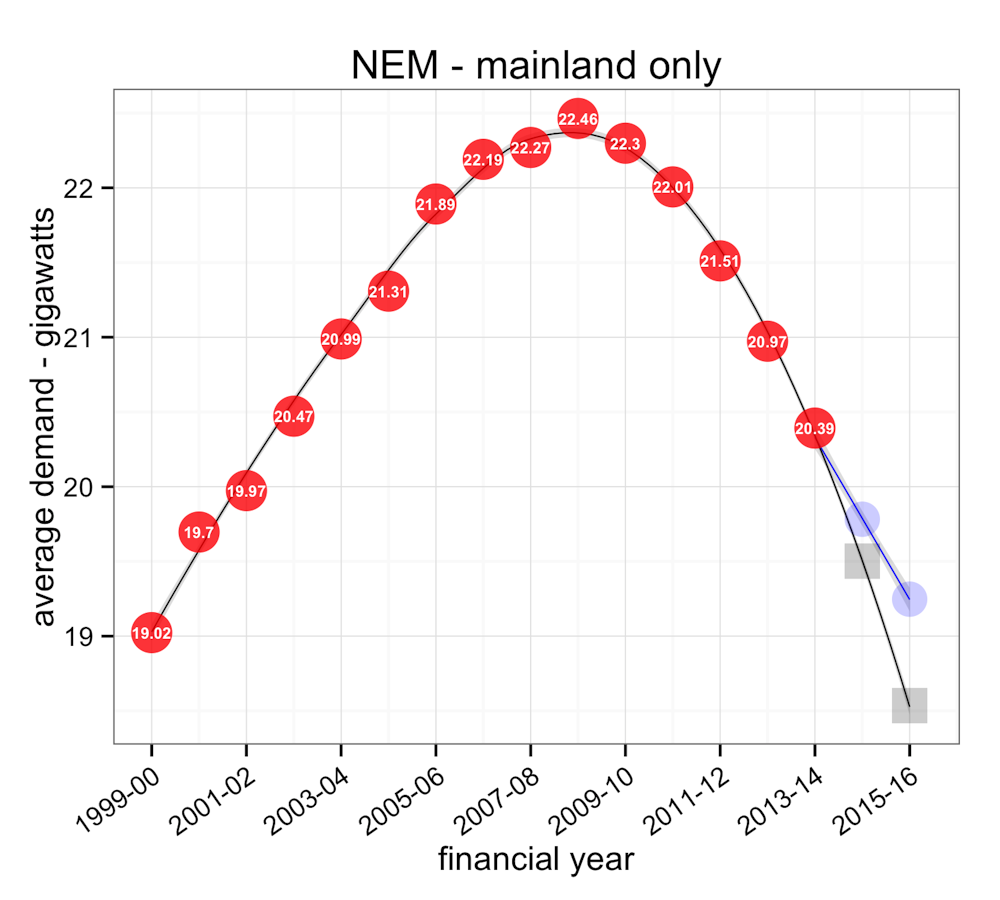

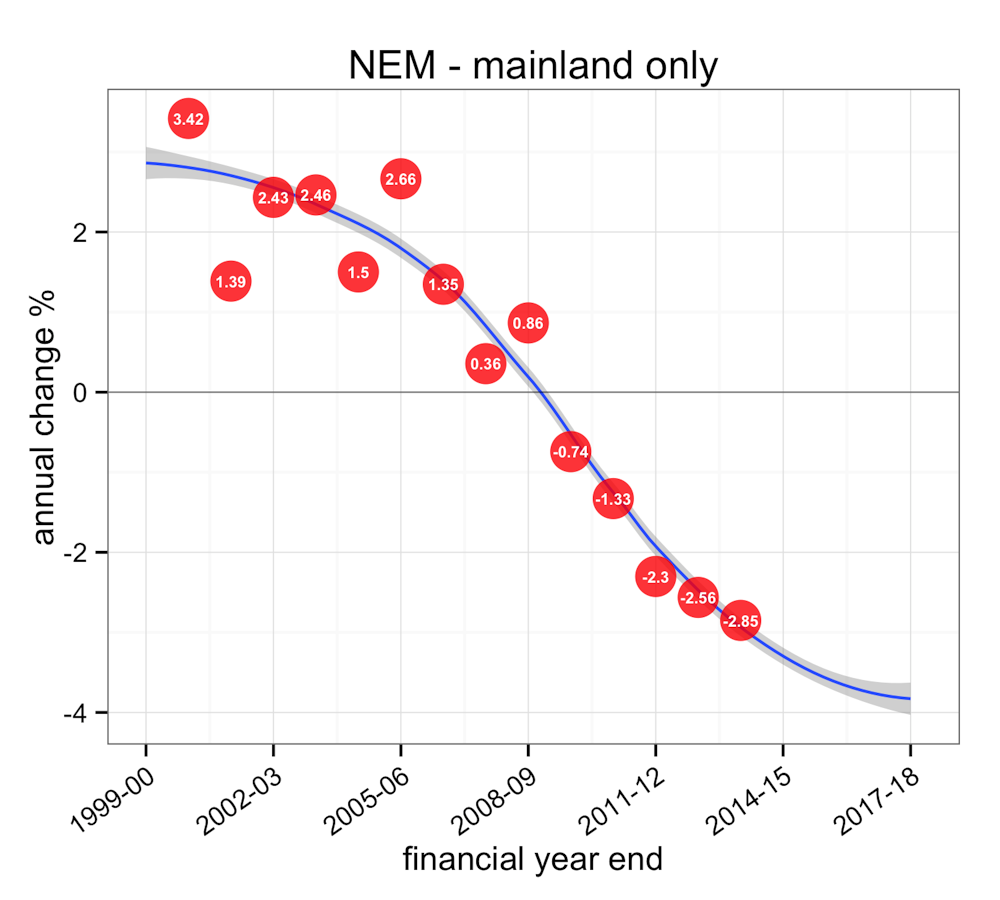

The 2013-14 financial year is the fifth consecutive year to see negative demand growth on the NEM. And the problem for the electricity utilities is that the demand is falling more sharply with each passing year. In 2013-14 demand fell almost 3%. The trend is really quite alarming.

Predicting energy demand is proving to be a mug’s game. Just ask the Australian Energy Market Operator (AEMO).

As recently as 6 years ago, growth in demand for poles and wires electricity could be counted on with certainty. Then demand grew at an average of a touch over 2% each year, varying between 1 and 3.5% depending on the economic cycle and seasonal weather variability.

It all made sense. With an implicit assumption that demand for electricity is inelastic, in an expanding economy, with a rising population, it has been a given for industry and government that demand must rise. And since poles and wires electricity seemed the only way of servicing that demand, growth was assured.

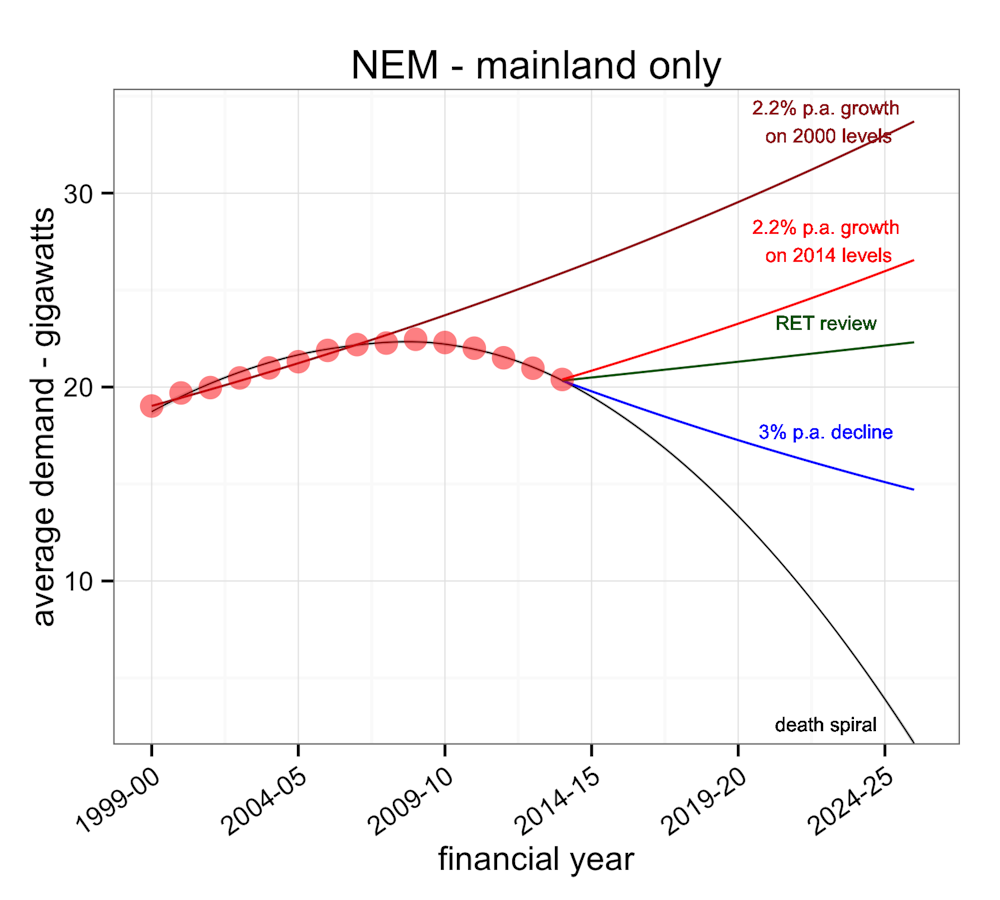

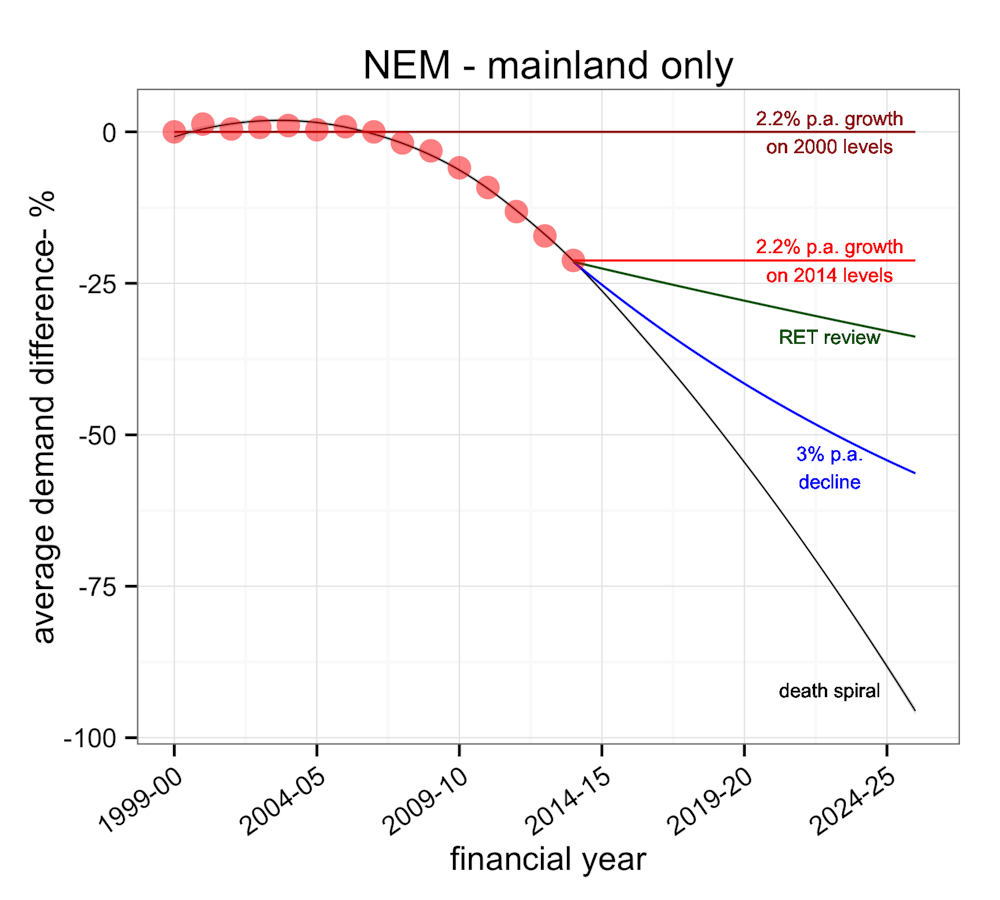

But since the GFC, the growth in demand has collapsed, initially flat lining before falling into negative territory where it has been for the last five years. In fact, compared to the forward projections of 2007, when 2.2 % annual growth seemed assured, demand is now down some 6 gigagwatts, or almost 25%.

Since the GFC many things have changed. The take-up of distributed technologies have greatly reduced demand for poles and wires electricity. And poles and wires electricity is no longer the only game in town due to the phenomenal cost reductions in solar photovoltaic. Contrary to perceived wisdom, electricity demand has proved to be anything but inelastic.

The reduction in demand has clearly blindsided both industry and government, which continue to operate as though demand growth must inevitably return. Even the market operator, AEMO, has found the downturn difficult to comprehend. Each year for several years in a row, AEMO has been forced to revise down its electricity demand forecast.

In fact, the idea that energy demand growth is essential for a growing economy is so ingrained in industry and government thinking, that we might question their collective sanity. The idea that Australia might be in for a sustained period of falling consumption for poles and wires electricity seems almost impossible for industry and government to comprehend. In the recent RET review, ACIL-Allen assume long-term growth of 0.5% per annum.

In face of the current trend, this seems to be delusional at best, utter madness at worst. A more sensible assumption might be to presume that demand for poles and wires electricity will continue to decline. A more pertinent question might be “when will we no longer need transmission?”. On current trend, we might be guessing that could be frighteningly soon.

With average demand dropping almost 600 megawatts in the last financial year, and large electricity consumers such as the aluminium sector already exiting the industry, it is hard to imagine anything but further reductions.

And that will put upward pressure on costs of distributing poles and wires electricity, which in turn will further encourage energy efficiency measures and distributed generation.

It makes for challenging times for our energy utilities, who continue to want to operate a business model that involves servicing our need for the benefits of energy (heating cooling, lighting, communication etc.) by supplying more and more energy across the grid.

With the costs of distributing poles and wires electricity consuming a larger and larger proportion of the retail bill, it is time to step back and reconsider what we want from our energy system, and how we get there. With concerns growing over how the bleak demand outlook will impact the viability of the electricity grid, we could do well to ask “why do we continue to promote two energy grids (gas and electricity) to provide essentially the same energy service.”

.