The move by the RBA to a record-low 2.25% cash rate at its first meeting for 2015 has unsurprisingly reignited speculation of a “turbo-charged” bubble in Sydney’s house prices.

In actuality, the rate cut will not ignite a housing bubble and is the right policy given broader macroeconomic conditions.

While prospective property buyers in Sydney may feel the central bank has snubbed them, monetary policy is about a lot more than Sydney’s house prices. While pockets of Sydney have experienced high price appreciation in the past 12 months, this growth has not been experienced evenly across the city and certainly not across the country. Latest data from CoreLogic RP Data, for example, show that while property prices in Sydney are up 13% over the past year, prices in Perth (2.56%), Darwin (1.40%) and Canberra (-0.34%) have barely kept pace with inflation in the 12 months to 31 Jan 2015.

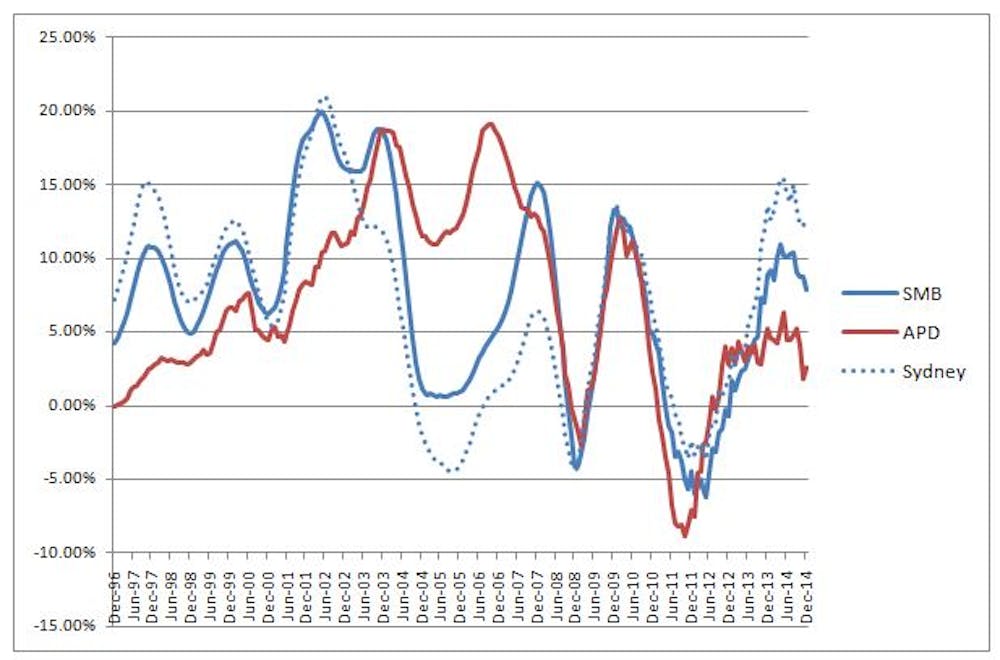

This high variation in property prices across the country is a recurring theme in Australia. The figure below shows the average annual housing market returns to the east coast cities (SMB: Sydney, Melbourne and Brisbane) against non-east coast cities (APD: Adelaide, Perth and Darwin). For comparison, housing market returns in Sydney alone are also charted.

Several facts become apparent in this analysis. Firstly, while price growth in Sydney has been high and increasing in the past year, it is not a bubble and is showing signs of cooling off. It also shows how the two-speed economy extends to housing markets.

Monetary Policy Is About More Than Sydney’s House Prices

The RBA cash rate is a blunt policy tool. The same rate applies to the housing market in Sydney as much as Perth, and to homeowners as much as small business owners, farmers and stock market investors. Adjusting the cash rate in order to target something as specific as house prices in Sydney is certainly not the appropriate response.

Rather the RBA has used the cash rate to target inflation. In the broader economy, there has been a significant easing in inflationary pressures. Commodity prices are falling, unemployment is creeping up and, most importantly from the RBA’s perspective, the consumer price index grew at its slowest rate since mid-2012 last year, slipping below the 2-3% target range.

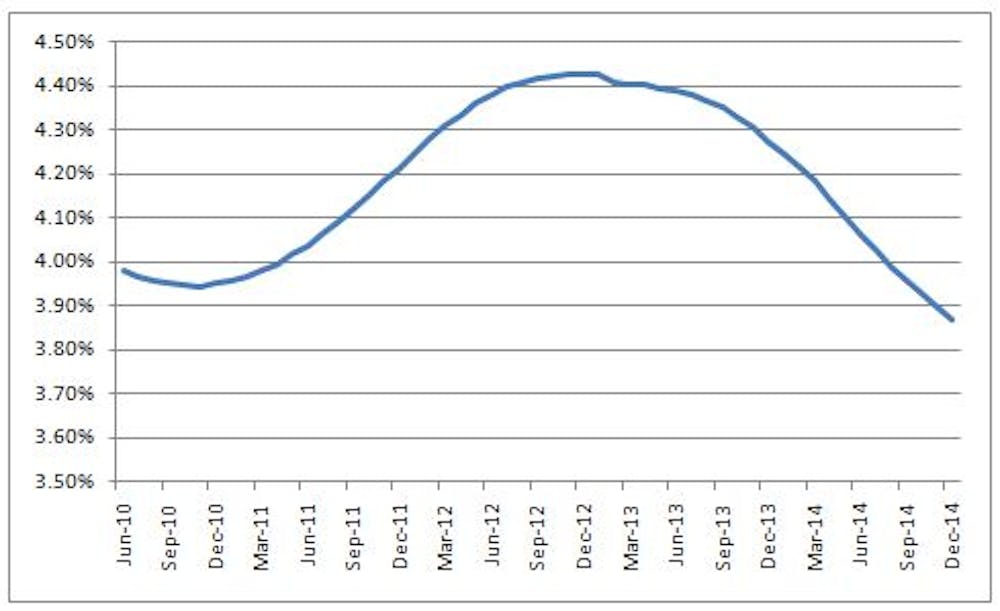

Another common argument you will hear from the bubble-spruikers is that property investors are going to fuel price increases with lower borrowing rates. Over the past year credit growth to housing investors has grown relative to homeowners (although subsequent data revisions indicate this difference was initially exaggerated). However, this trend is unlikely to continue with rents steady and yields falling markedly in the past year. Where the average rental yield in Sydney in 2013 was over 4.25% it has fallen to under 3.9% in 2014.

It is the role of regulators and government, not the RBA, to consider issues such as housing affordability and equitable access. We are seeing other regulators, such as the Australian Prudential Regulation Authority (APRA), actively monitoring lending practices as a targeted response to risks in the housing market. Earlier this week, the Prime Minister also signalled that issues around foreign investment would be considered by the government and Foreign Investment Review Board in coming weeks.

Keep these facts in mind as the tea leaves of the RBA’s February Statement on Monetary Policy are read and you hear about the impending property bubble.