Indigenous people will retire with 27% less income than non-Indigenous Australians, according to new research by Griffith Centre for Personal Finance and Superannuation. *

People who identify as being of Aboriginal and Torres Strait Islander (ATSI) origin make up 2.5% of Australia’s population. Australia’s indigenous people have a younger age distribution compared to non-indigenous Australians, with a median age of 21 years compared to 38 years for the non-indigenous population.

Superannuation is a highly researched area - however, very little attention has been given to understanding the retirement outcomes associated with indigenous Australians.

Researchers at the Griffith Centre for Personal Finance and Superannuation (GCPFS) have examined the retirement gap between the “typical” worker and other disadvantaged socio-economic segments (such as indigenous Australians) given the effects of time, asset returns and contribution rates.

The median indigenous income (for an employed person) is approximately 23% lower than the non-indigenous income per week.

A possible explanation for the income gap between Indigenous and non-Indigenous Australians is the level of education of the two populations. The evidence shows that Indigenous Australians have a substantially lower level of education than their non-Indigenous counterparts.

Around 59% of ATSI people aged 20-24 in 2012-2013 have completed year 12 or equivalent. For the non-Indigenous population aged 20-24 in 2010-2012 the proportion was 86-88%.

Reports show strong correlations between lower educational attainments, low incomes, unemployment and income support across both groups. Studies by Leigh 2008 show that non-completers earn lower wages, by as much as 8-11% for each year of non-attainment among other disadvantages.

This evidence can be seen in the distribution of occupations. At the low end of the pay scale, about 18% of employed indigenous Australians work as labourers and 17% as community and personal service workers compared to 9% and 10% for non-indigenous employees, respectively.

On the other hand, professionals and managers make up close to 20% of the indigenous workforce while the non-indigenous workforce comprises around 34% in these occupations. Improving literacy and numeracy levels and increasing year 12 completion rates could significantly improve education and employment outcomes for ATSI Australians. This is important as the level of income directly impacts on superannuation contributions and retirement savings.

Our study simulates the retirement outcomes of two individuals, an indigenous and non-indigenous Australian, both aged 25 years and in some form of full-time employment, under similar contribution and returns assumptions. The two full-time workers are assumed to contribute 9.5% of their pre-tax annual income into their superannuation fund.

This fund is invested in different strategies and we report the results based on a balanced 70/30 superannuation fund (that is, a fund has 70% invested in assets such as domestic and international shares, infrastructure and property and 30% in cash).

Our findings show that the non-indigenous full-time worker accumulates approximately 30% more superannuation wealth, on average, than the indigenous worker across all percentiles. This translates to about $165,000 (in today’s dollars) in extra superannuation savings, on average. Is this level of savings able to generate income to support a comfortable retirement?

We estimate how much guaranteed income one is able to derive from their superannuation at retirement and compare it to the Association of Superannuation Funds of Australia (ASFA) estimates for a comfortable retirement.

While the presence of the age pension complements the superannuation balance and may propel one to reach the comfortable retirement estimates, we investigate how close retirees are to being self-sufficient - that is, attaining comfortable income levels in the absence of pensions.

Increase contributions or work longer?

For these two populations, we find that for one to be self-sufficient in retirement, the non-indigenous worker will require an 11 per cent annual contribution rate into superannuation to reach the ASFA comfortable retirement income estimate. For the indigenous worker, a superannuation contribution of 14.3% will enable him to attain this retirement estimate.

While the ASFA estimate may not be a silver bullet in determining what makes a comfortable retirement, we believe it is a good anchor to inform and compare income levels in retirement.

If superannuation contributions remain at the current rate of 9.5 percent, both populations will need to delay retirement in order to accumulate wealth to sustain a comfortable income level in retirement. The non-indigenous Australian is able to retire with an adequate income at age 68 years.

The indigenous Australian who wants to retire comfortably on a 9.5% annual contribution must work until age 71.5 years, 6 and half years more than the current retirement age.

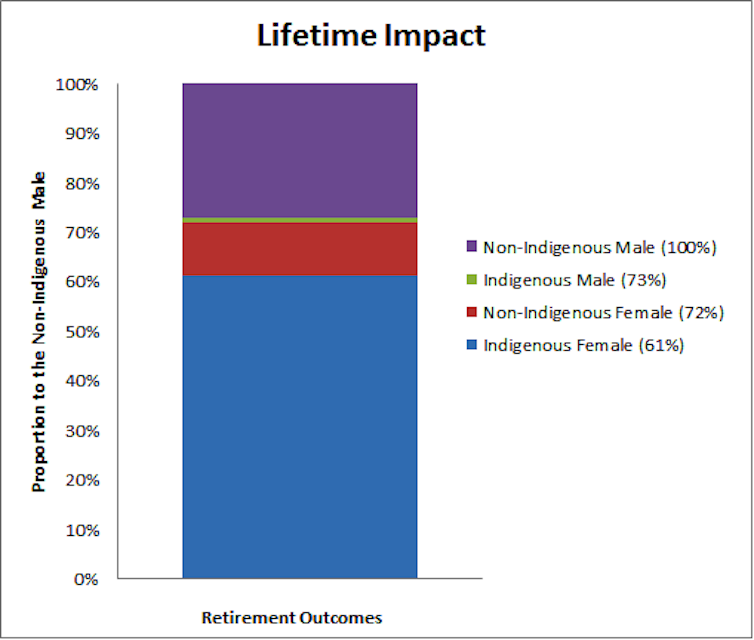

Lifetime impact of the difference in incomes

In summary, differences in current incomes have a significant impact on retirement outcomes. For about a $300 gap in weekly income (pre-tax), the male indigenous worker has a mean retirement outcome which is 27% lower than the male non-indigenous Australian over 40 years. This translates into a difference of approximately $250,000 in today’s dollars.

The average retirement balance of the non-indigenous female sits at 1% lower than the indigenous male. We use optimistic assumptions for non-indigenous women including no career break or other disturbances to their working pattern. The inclusion of these real-life parameters will further reduce these retirement outcomes. The mean superannuation balance of female indigenous workers is 64 percent lower than non-indigenous males.

This difference equates to approximately $350,000 in today’s dollars. There is significant variation in retirement outcomes from the “typical” Australian and while we consider ways to improve the gender balance, the story for indigenous Australians is equally important.

- This piece has been altered since publication to correct the headline and first line, which stated indigenous Australians retired with 23% less income. The correct figure is 27%. The error was introduced at the editing stage.