With the federal election only five days away and the cash rate at an historical low last month, the dominant approach for the Shadow Board members is to wait and see what the election will bring.

The outlook for the global economy has not changed appreciably from last month. While the US Federal Reserve is looking for an exit from its quantitative easing program (QE3), there exists a growing concern about the possible implications of rising world interest rates and reversals in international capital flows, particularly for some of the developing nations in the Asia Pacific region.

Domestically, previous interest rate cuts are slowly feeding through the economy, buoying the real estate market and depreciating the Australian dollar. However, the longer it takes for low interest rates to stimulate the real economy, the greater the risk that easy money will lead to inflated asset prices and to financial trouble in the future.

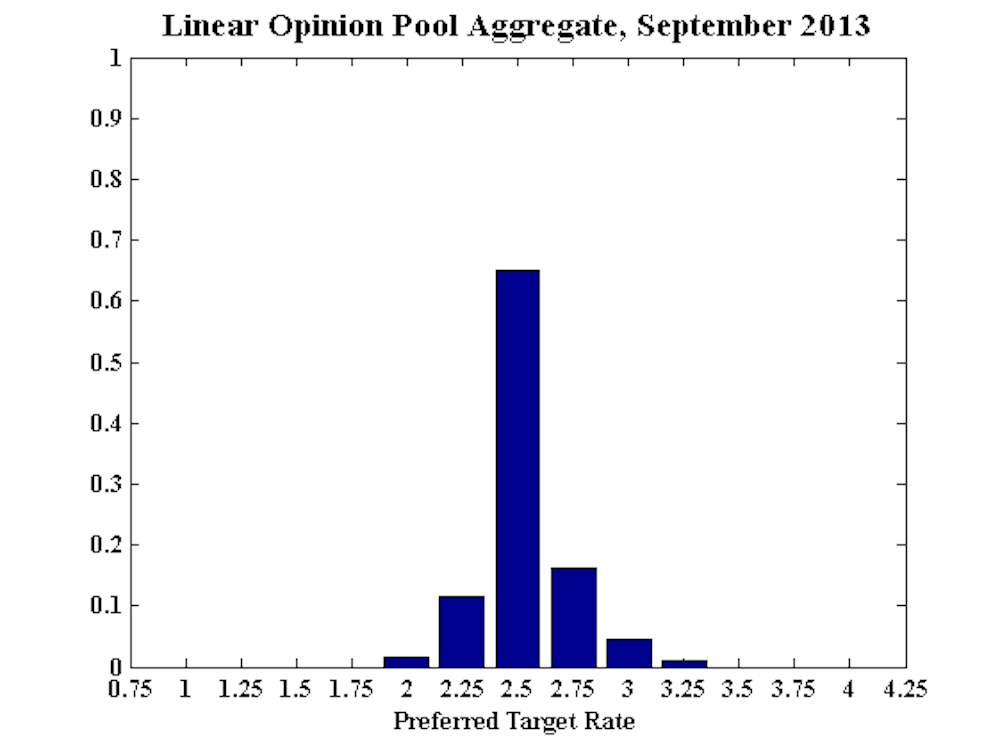

After the RBA’s decision to cut the cash rate to 2.5% last month, the Shadow Board’s preference for keeping the cash rate unchanged is strong: the nine members are 65% confident that holding steady is the appropriate policy. Members are only 13% confident that a further reduction of the cash rate by 25 basis points is warranted, while a 22% probability is attached to the need for a higher current rate.

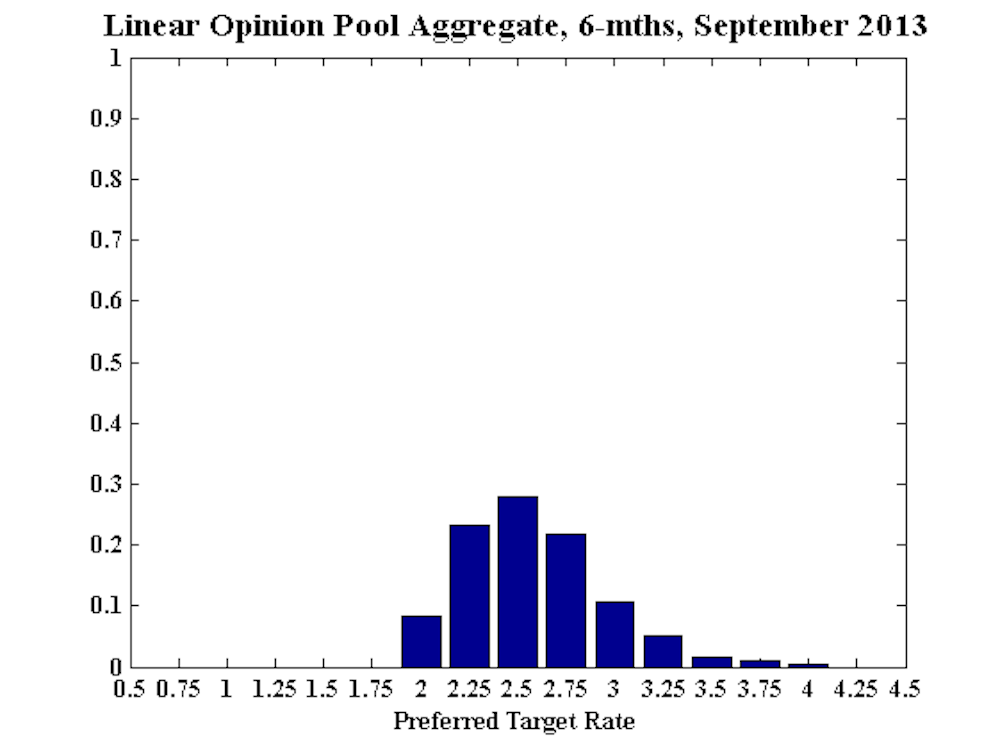

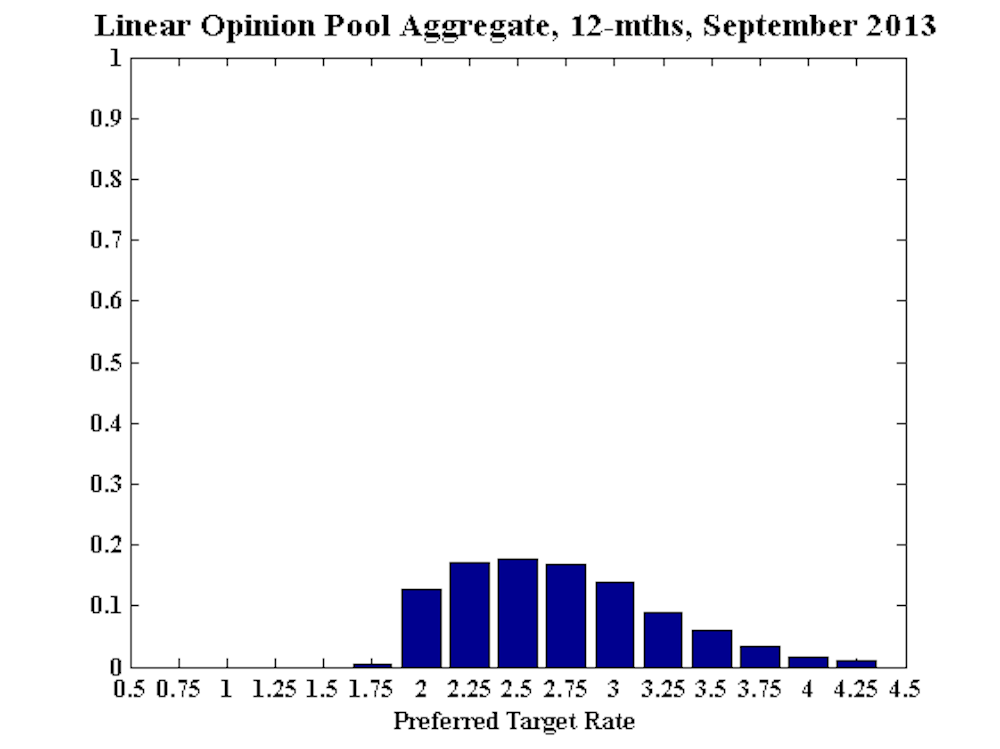

There is more uncertainty about the appropriate policy setting at longer horizons: the probability that rates will need to rise in the next six months is about 41%, while the probability that rates ought to be lower than the current rate has increased to 32%. A year out, the shadow board members attach a 52% probability to the need for an increase in the cash rate and a 31% probability to the need for a decrease in the cash rate.

The CAMA RBA Shadow Board is a project by the Centre for Applied Macroeconomic Analysis, based at the ANU, which asks industry and academic economists what interest rate the Reserve Bank of Australia should set.

The project is designed to test and improve transparency of central bank deliberations by revealing the opinions of individual members, emphasising the underlying macroeconomic uncertainties.

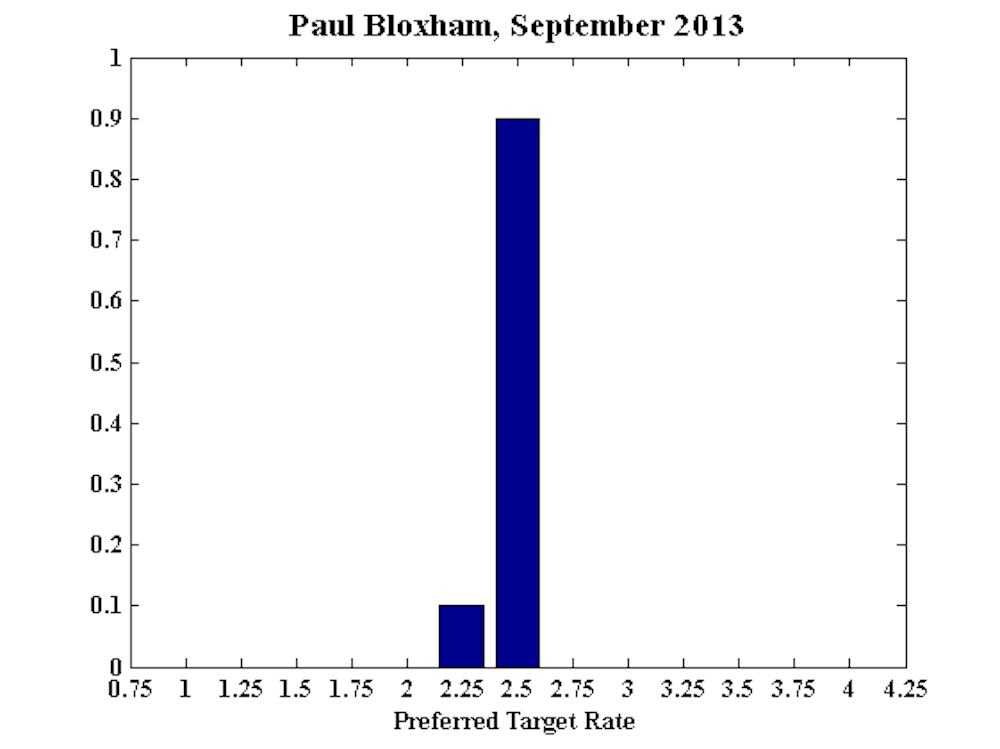

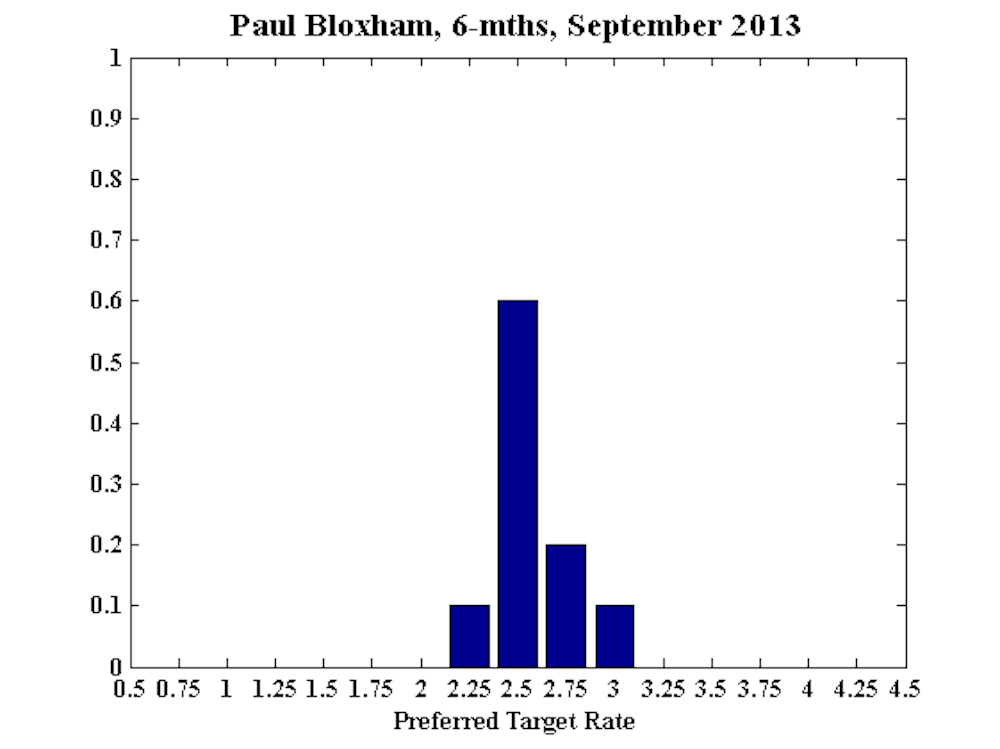

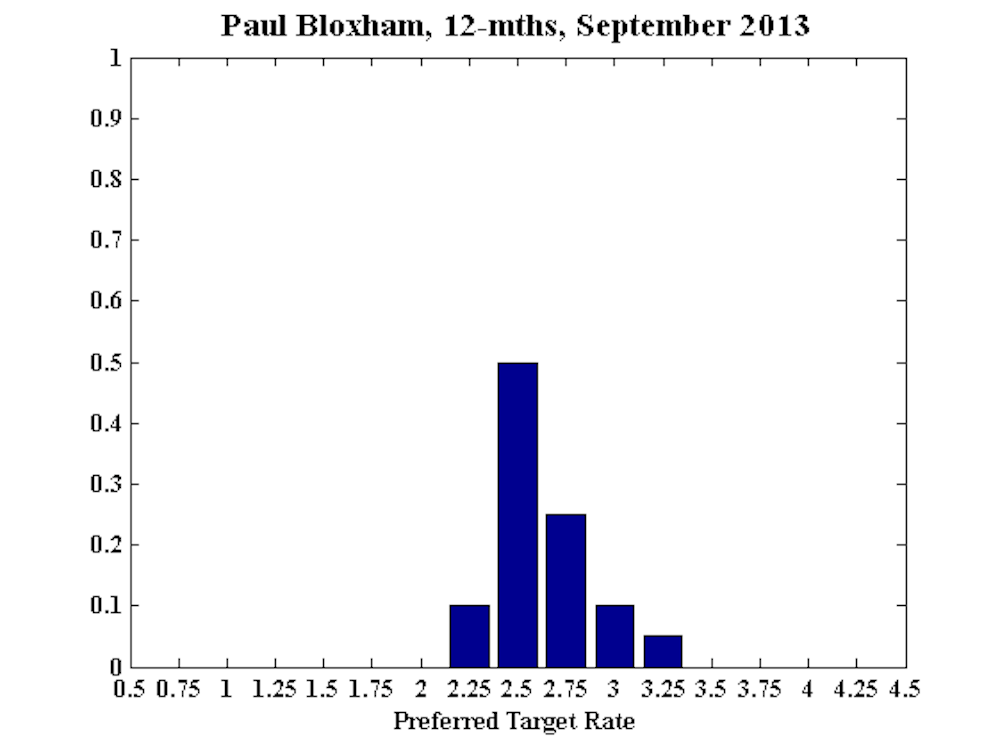

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

With the RBA having cut the cash rate just last month, I recommend that the rate is kept on hold this month. The cash rate is now at a very low level relative to history and is imparting significant stimulus into the economy.

The fall in the Australian dollar since April has also loosened broader financial conditions considerably. Low rates are already feeding through to the housing market, where turnover has picked up and prices are rising solidly. There has been less evidence of loose monetary policy supporting other areas of the economy as yet. Monetary policy settings are, however, not a barrier to growth, suggesting that weakness in other parts of the economy is likely to be due to factors outside of monetary policy.

In short, monetary policy can’t be expected to do all the heavy lifting in the economy. Cutting rates further from here may entail increased risks of asset price misalignments. While in the short run rising asset prices are likely to support growth, they may cause other problems in the medium term. For this reason I am cautious about recommending that rates fall any further from here in the coming months.

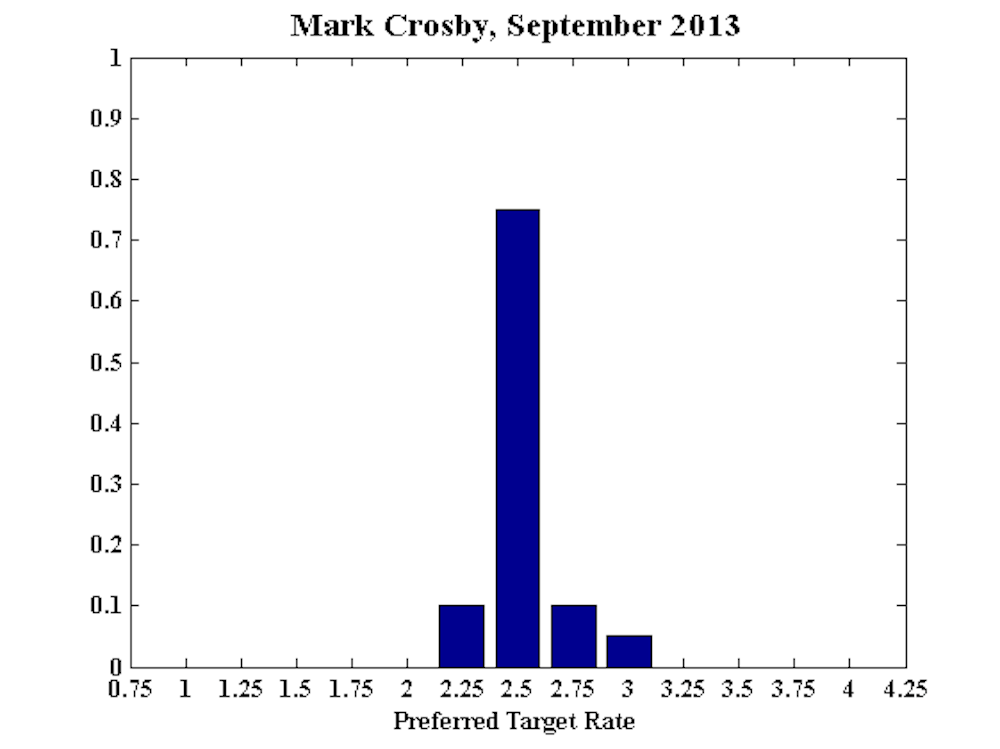

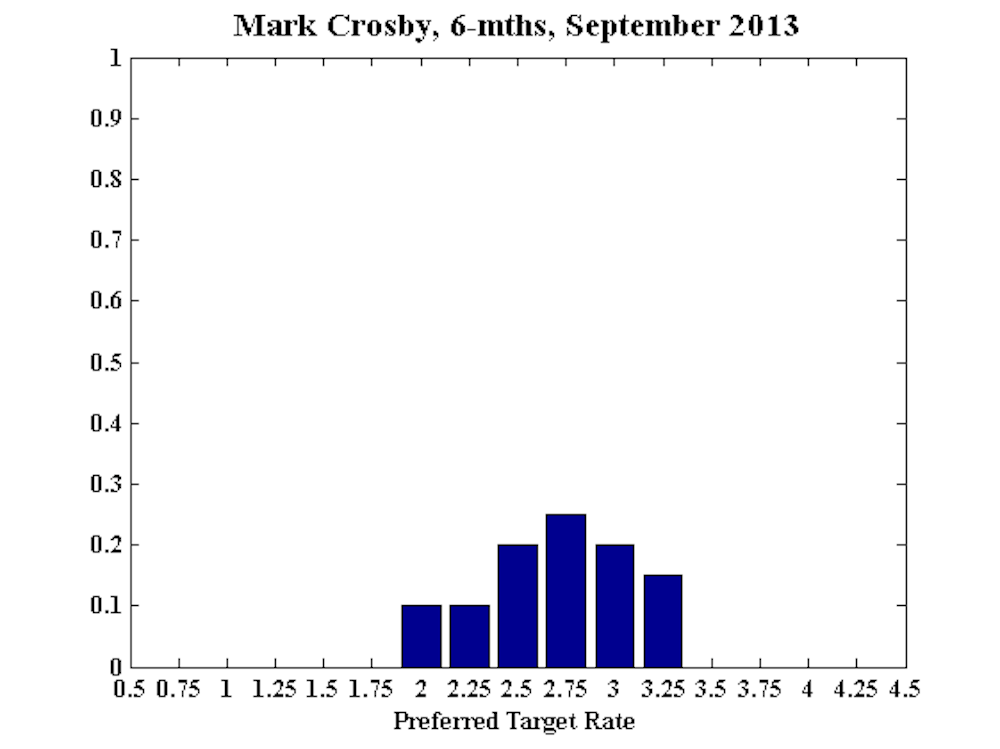

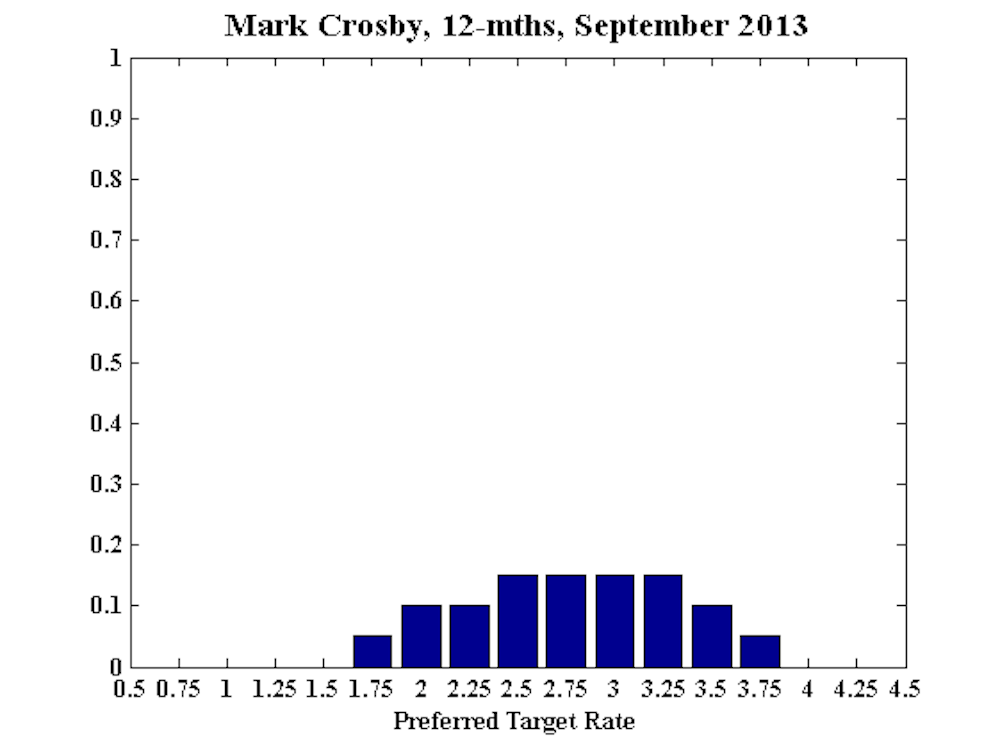

Mark Crosby, Associate Professor, Melbourne Business School:

With recent rate cuts still feeding through to the real economy there is little reason to see rates lower despite ongoing international uncertainty.

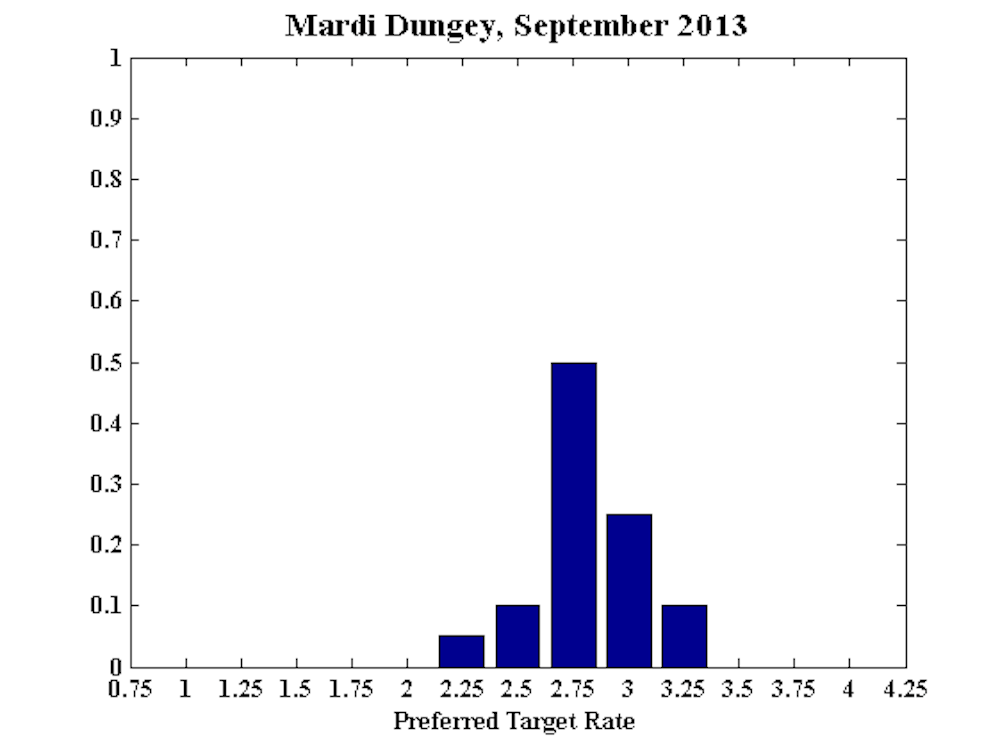

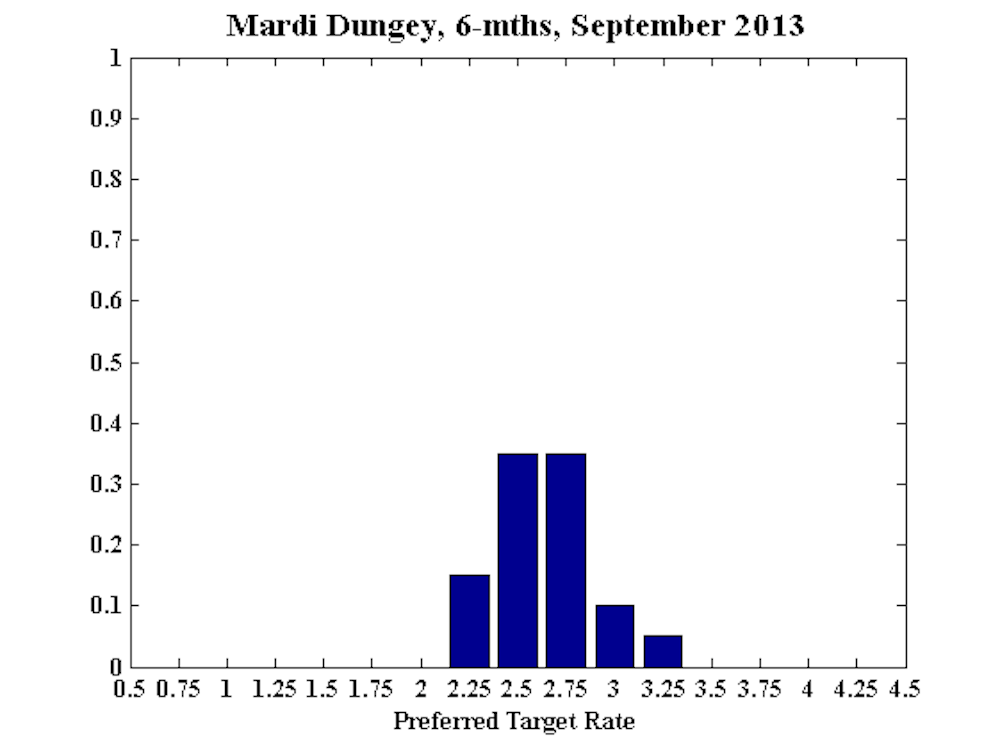

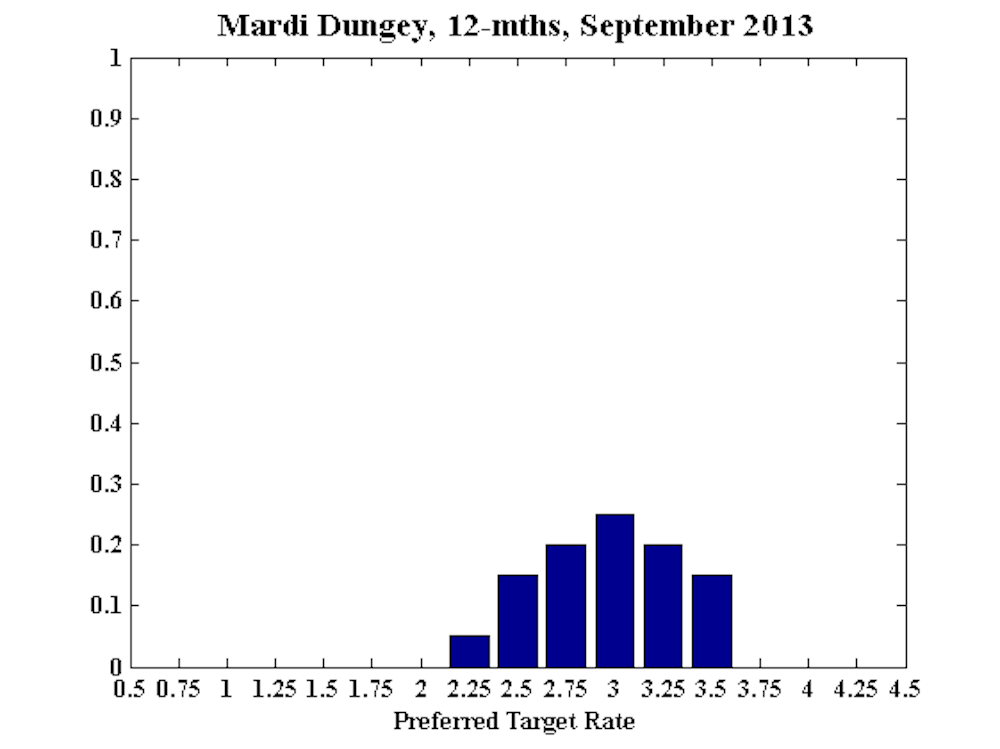

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA:

No comment.

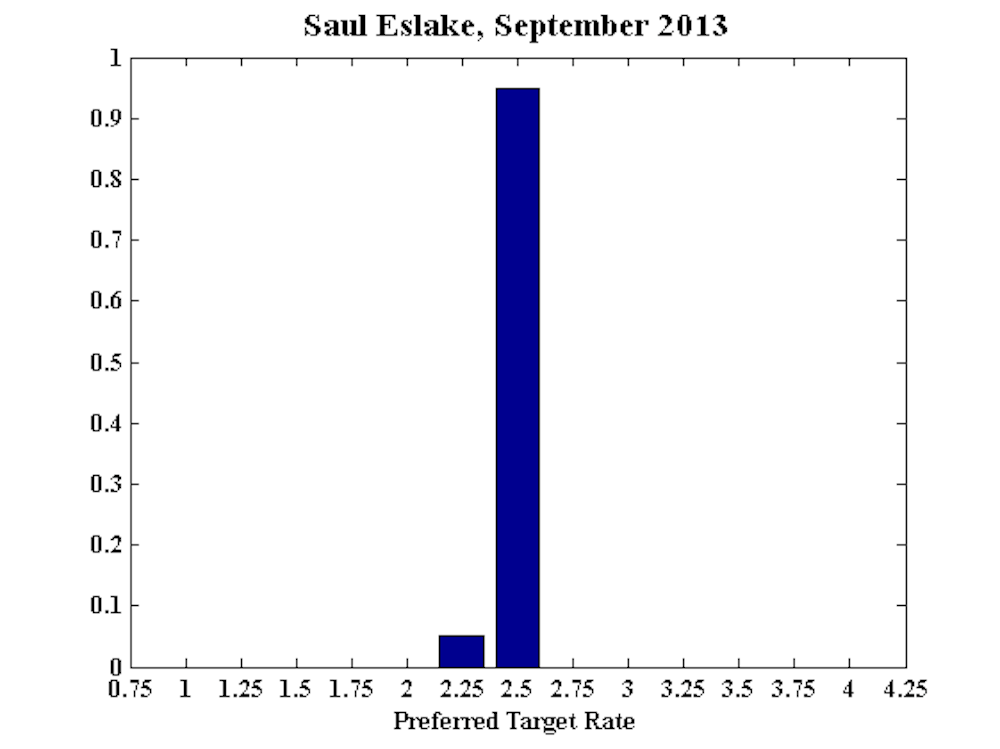

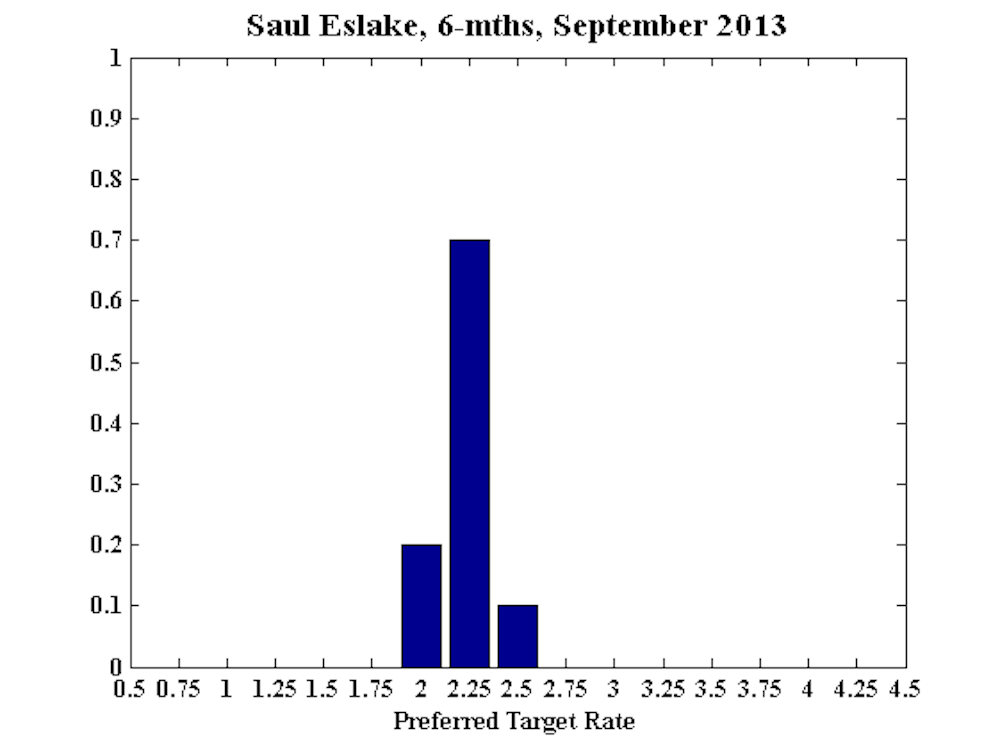

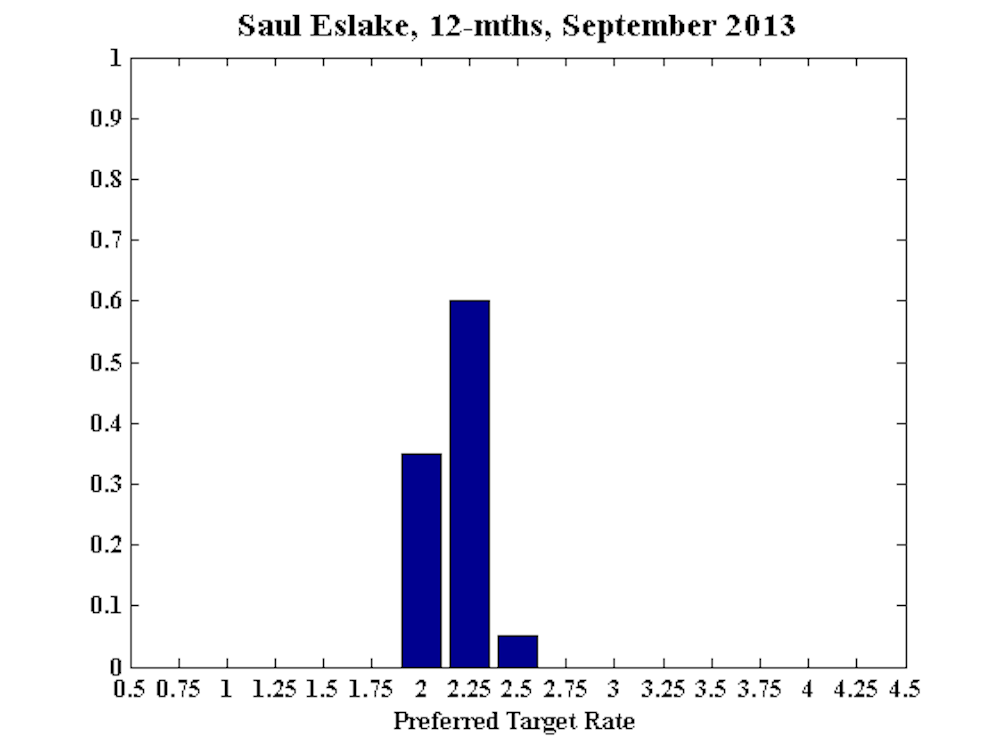

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia:

I can’t see much justification for the RBA to cut rates at a second consecutive meeting, and just four days out from the election. It’s possible that there could be a “bounce” in business confidence if the election results in a change of government (and the new government has a comfortable majority in the Lower House), although whether that “bounce” is sustained will depend importantly on the performance of that government in its early days. Otherwise I expect the economy will continue to grow at a below‐trend pace, with unemployment continuing to edge higher, making a further rate cut over a six month horizon desirable.

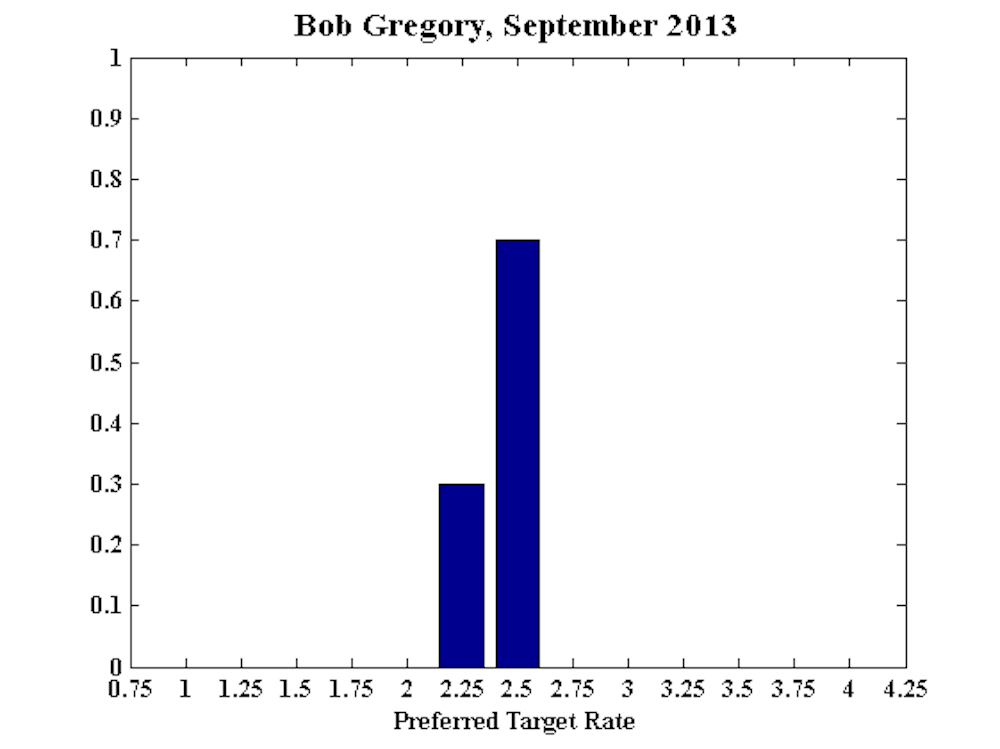

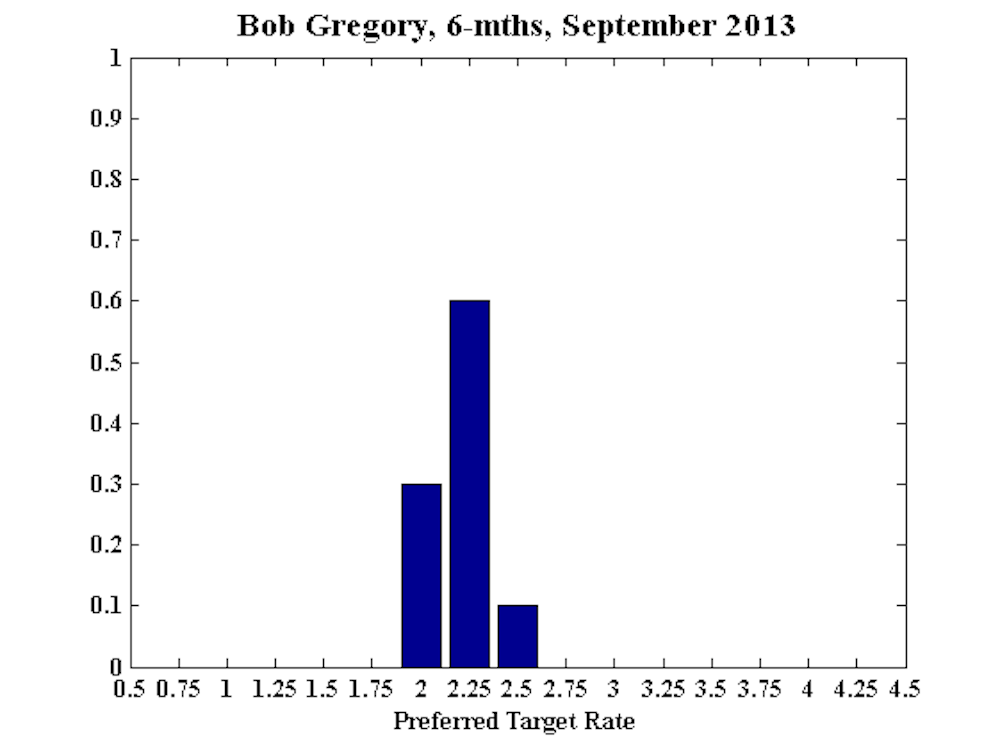

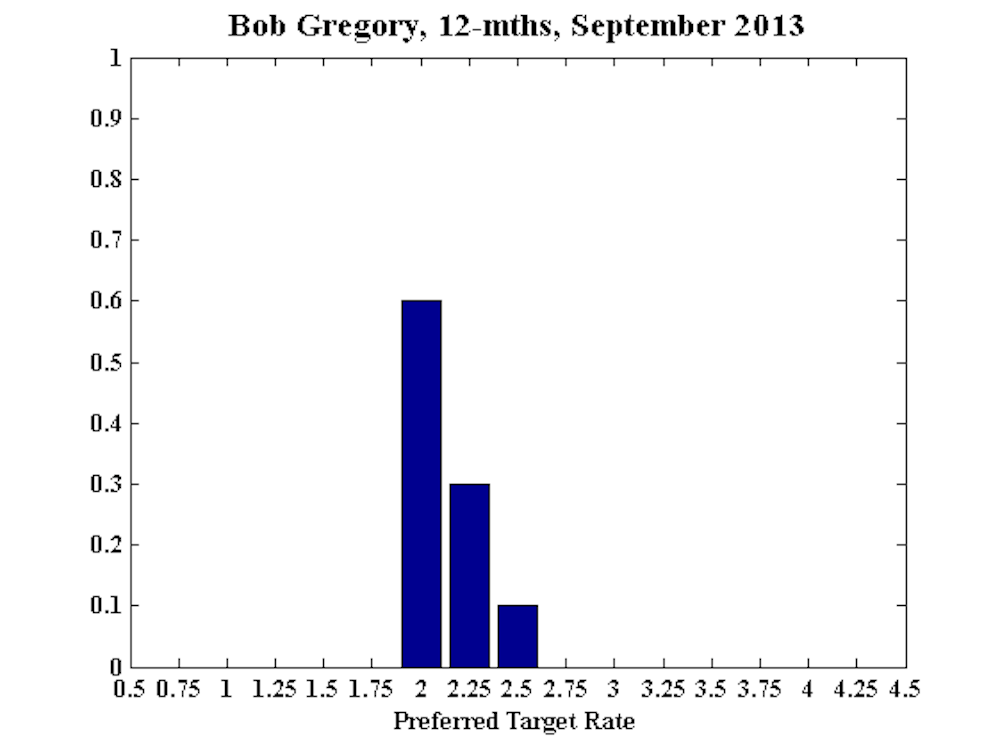

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology:

No comment.

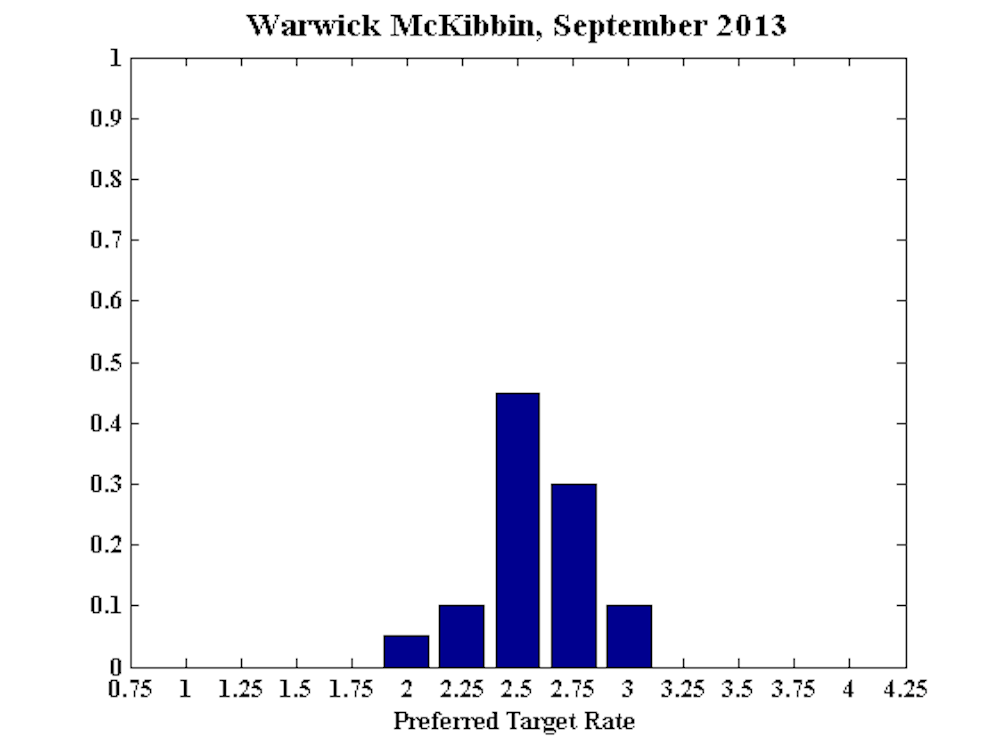

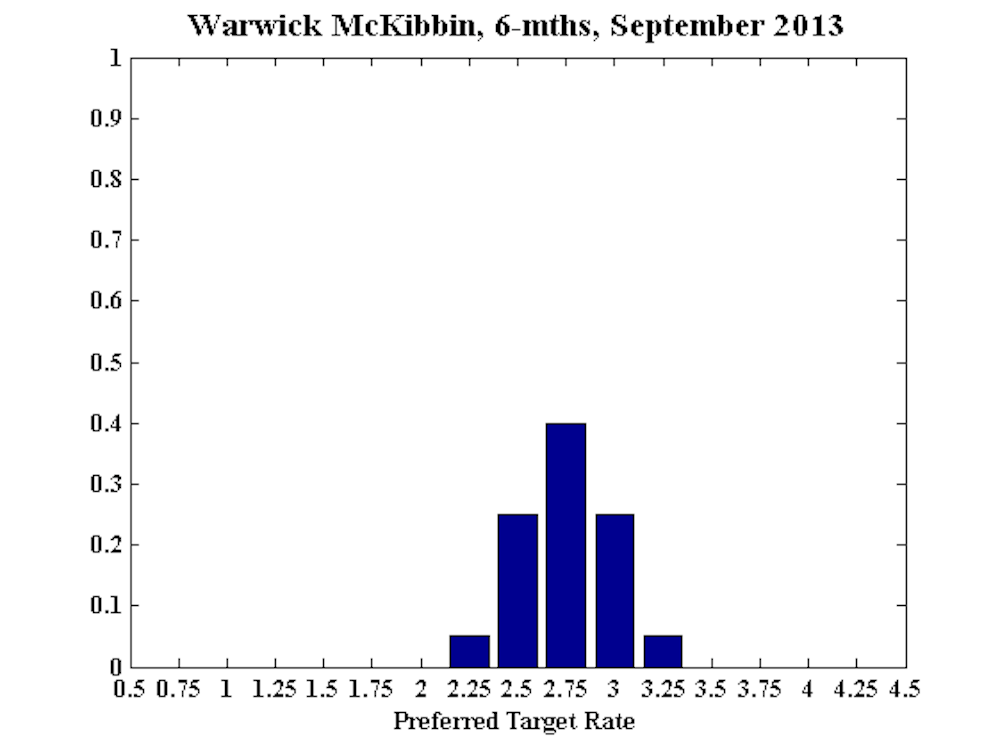

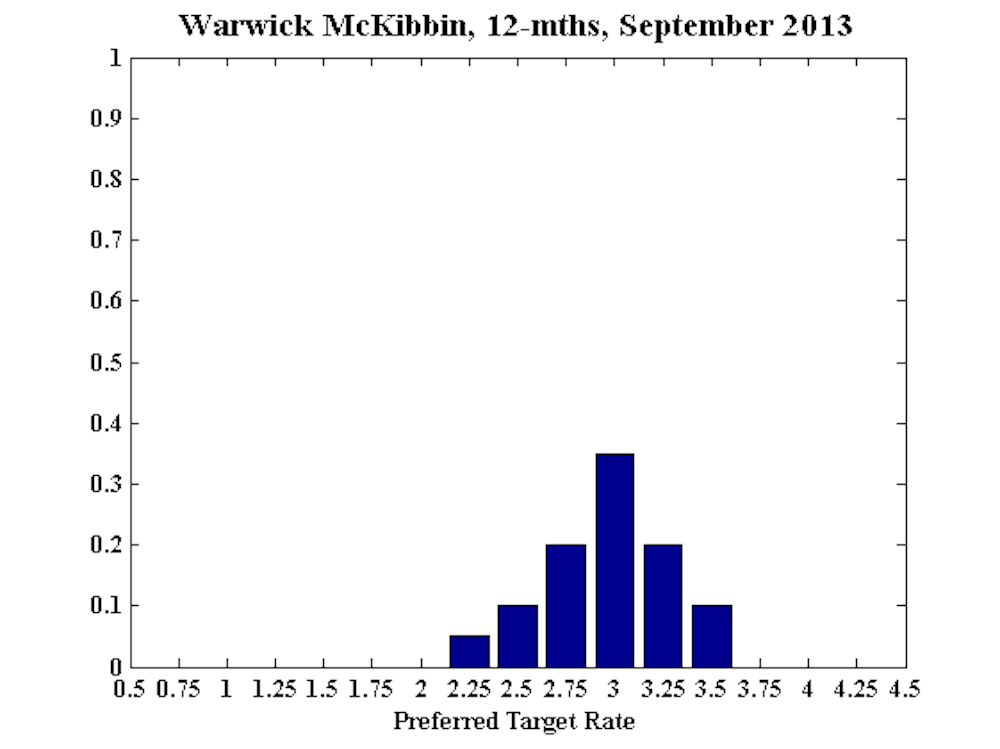

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University:

Here is continuing evidence that loose monetary policy in Australia is driving the demand for assets rather than supply (especially housing) suggesting that that asset prices are inflating relative to fundamentals. Political uncertainty that is hurting confidence is likely to be resolved soon although the first 100 days of the new government will be decisive in setting a clear growth agenda for the next few years. Structural reforms are critical to take the pressure of monetary policy so it can respond to external macroeconomic forces rather than structural problems in Australia.

Globally emerging markets are being stressed through a reallocation of global capital flows as the Fed edges closer to the end of quantitative easing. As capital flows into the strengthening US economy, the falling bond prices globally will continue and global long term interest rates will rise. This will be a dangerous period for some economies who have not wisely used the cheap global capital to undertake growth stimulating reforms or to solve debt problems that make them vulnerable to shocks. There is a high likelihood of some countries entering a crisis during the adjustment in the next year and policy in Australia may need to respond to this external shock.

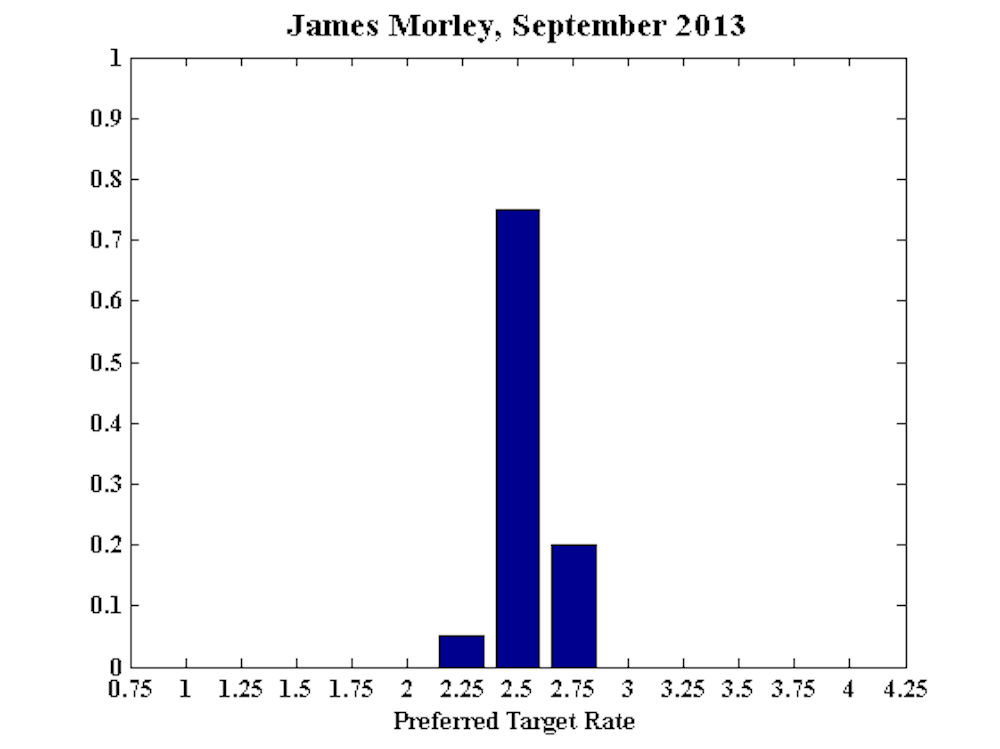

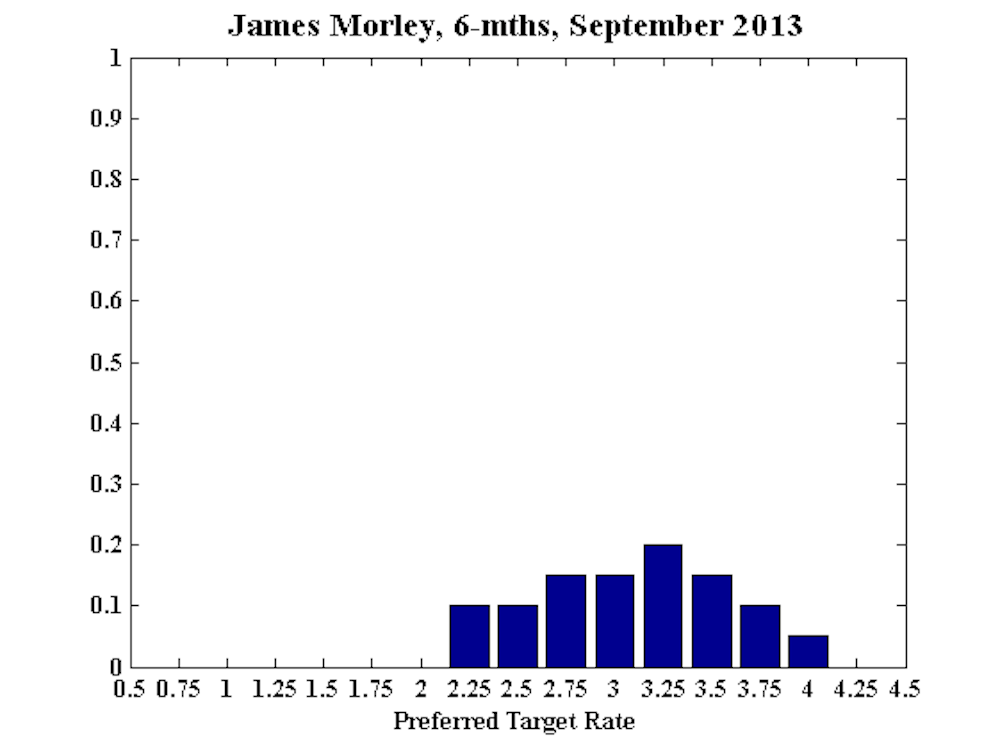

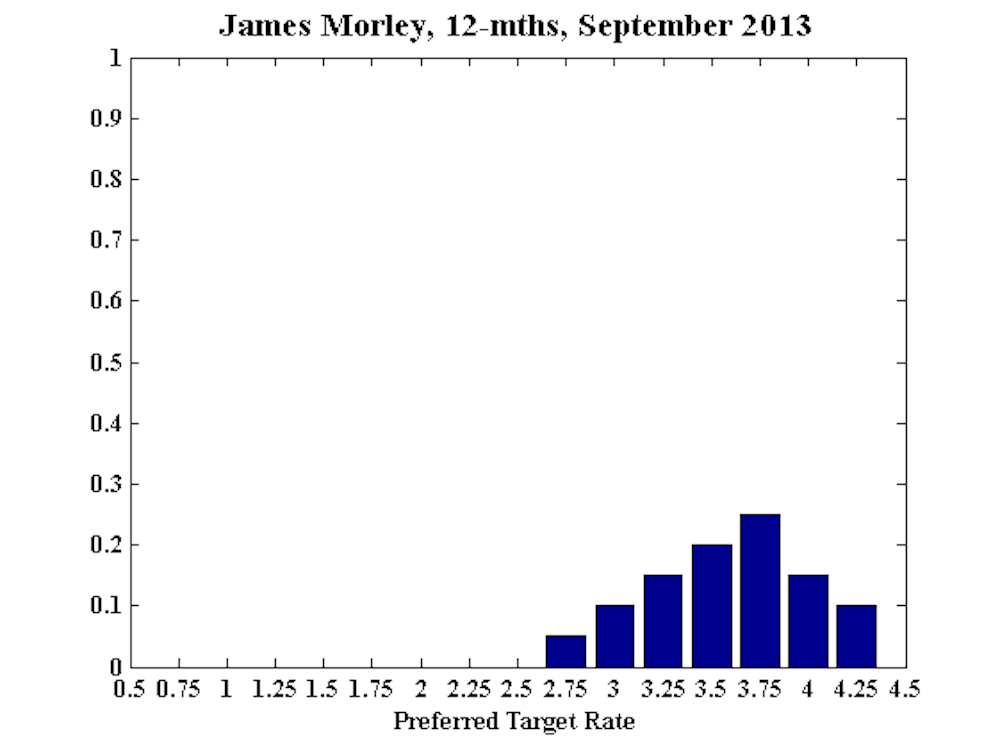

James Morley, Professor, University of New South Wales, CAMA:

I don’t expect the RBA to adjust the policy rate right before a national election, nor should they under most circumstances. Only if there were a big development prior to the meeting that suggests quickly rising inflation or rapidly deteriorating economic activity, should they adjust the policy rate. I do not think this will happen. So, the RBA should hold steady this month and re‐evaluate their policy stance in October.

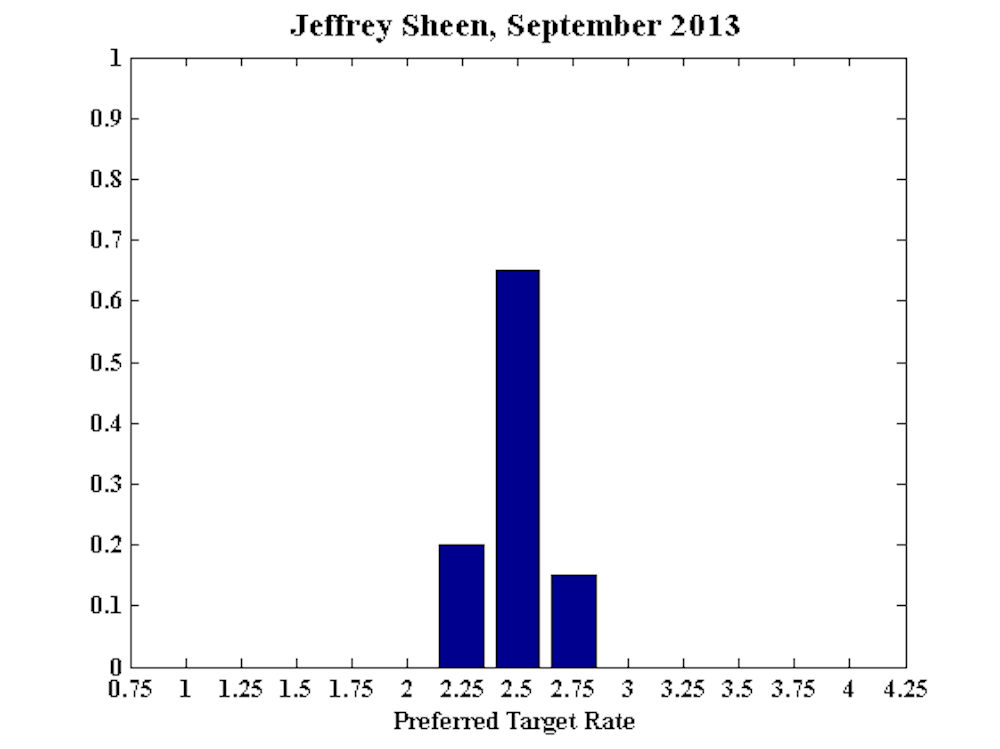

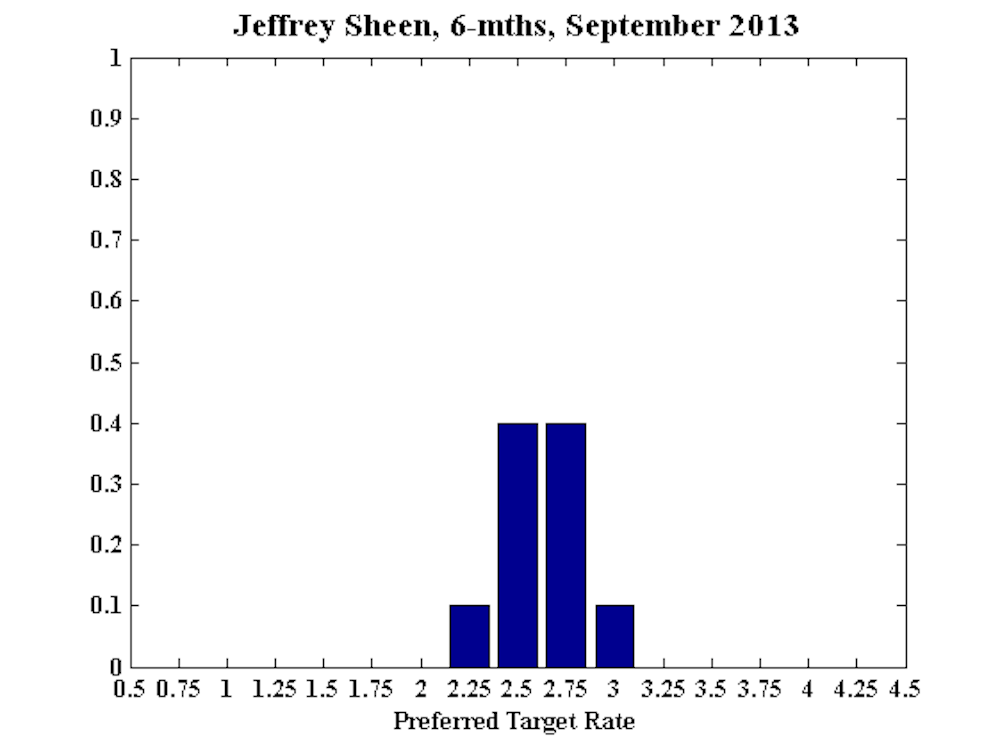

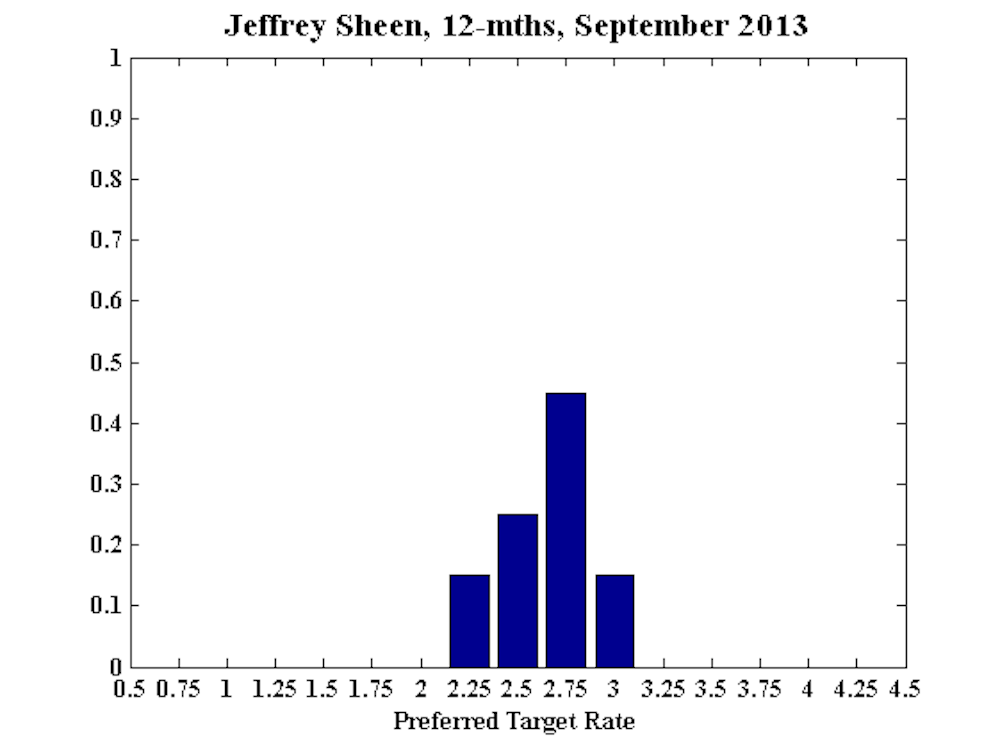

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

Business investment, particularly in buildings and structures, was remarkably strong in the third quarter of 2013. Mining continues to make a significant contribution, suggesting that the mining investment boom is far from over. The continuing decline in manufacturing investment (which is only about 6% of total investment now, down from 10% in 2010) should not be addressed by monetary policy.

The expected real depreciation of the Australian dollar is likely to encourage future export demand and also further foreign investment. Future monetary policy decisions will depend on the outcome of the election, but, whichever party wins, the fiscal implications remain somewhat uncertain. Therefore I recommend no change in the cash rate in September.

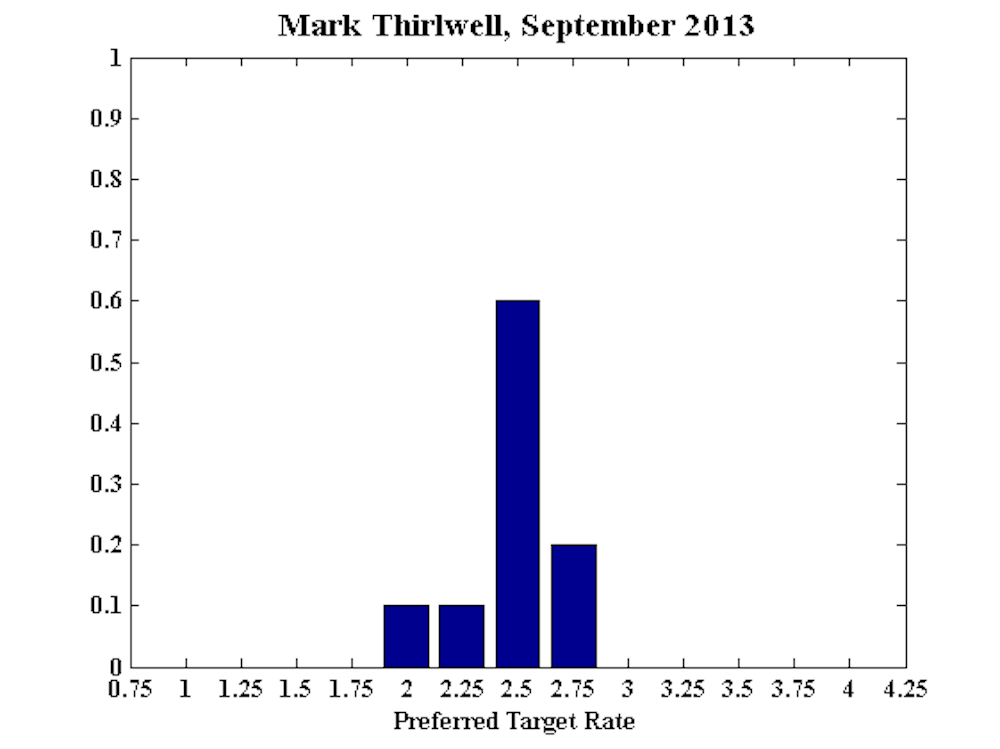

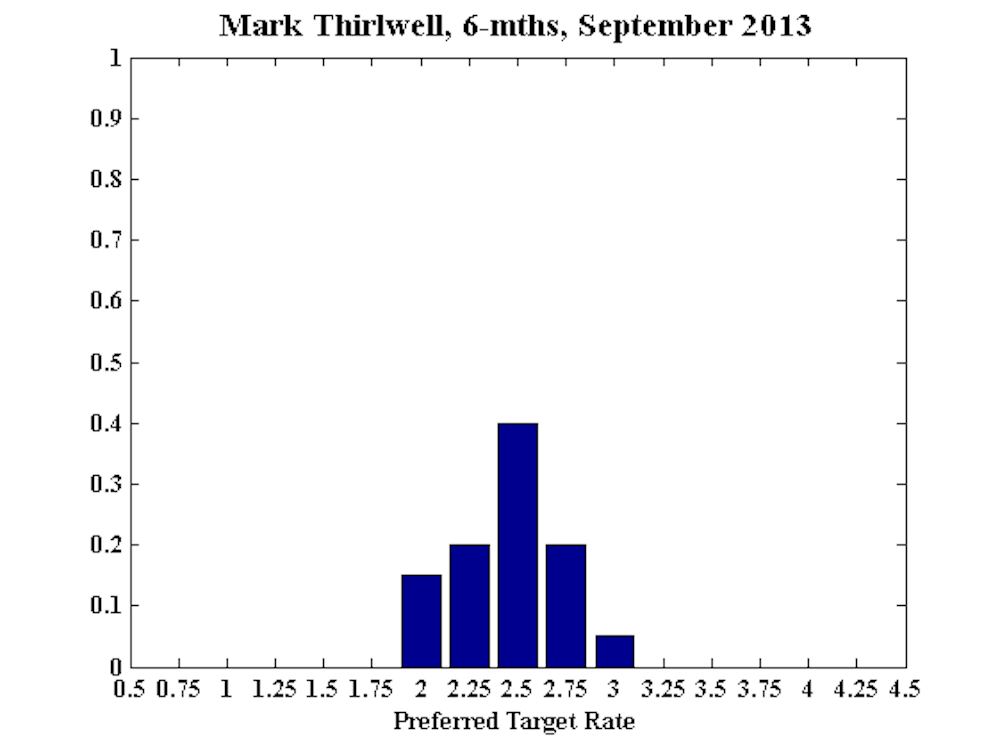

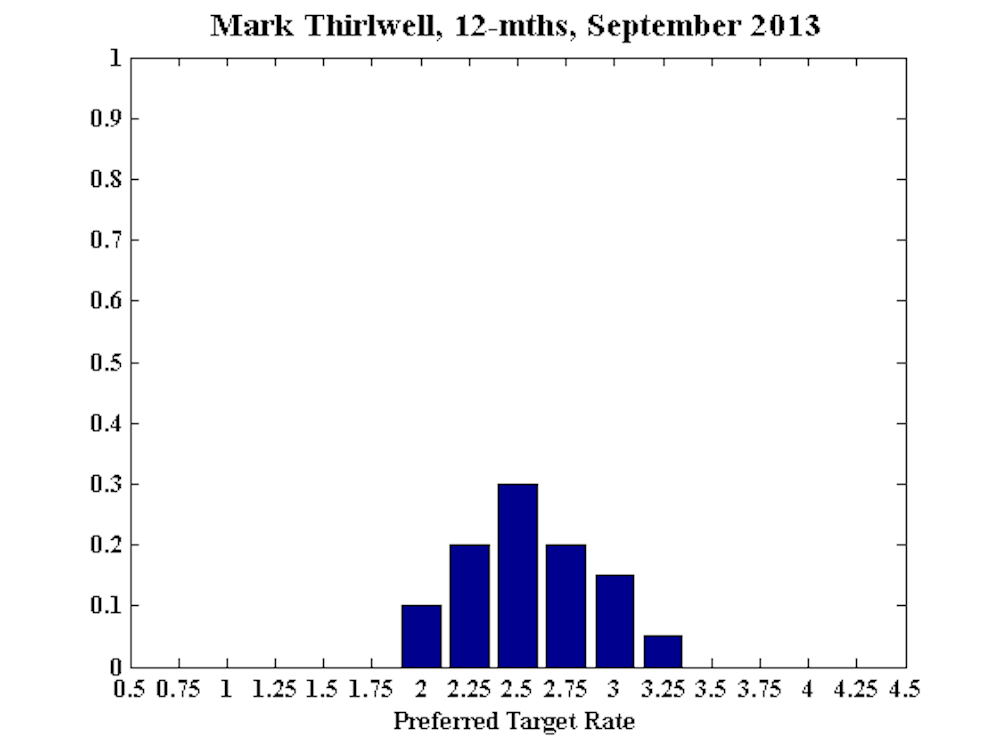

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy:

No comment.