One of the most important issues for small businesses is their ability to manage cash flow. This is regularly illustrated in the Telstra Sensis Business Index of small to medium sized enterprises (SMEs). This survey of 1,800 firms usually finds a lack of sales; cash flow management and profitability are amongst the top concerns of owner-managers. Given the importance of this topic it seems worthwhile to examine the academic literature to see what the findings from recent research studies might suggest for the owner-managers of small firms.

Despite its importance the number of academic papers published on the subject of cash flow management within small business, has been relatively limited over the past five years. However, several papers were found that offer some potentially useful findings. In this article I will overview three of these research studies and will follow up with further articles on this topic in the future.

Management of cash flow and working capital

The first paper is by Jay Ebben and Alec Johnson from the University of St. Thomas in the United States. It was published in the Journal of Small Business and Entrepreneurship in 2011. They examined a sample of 1,712 small U.S. manufacturing and retail firms drawn from the financial and business research database of the Ewing Marion Kauffman Foundation. Their aim was to understand the relationship between the cash conversion cycle (e.g. time taken to collect payment from customers) and levels of liquidity, invested capital and performance.

Their hypotheses were that firms with shorter cash conversion cycles would require less invested capital, enjoy superior financial performance and be more liquid that firms that had longer cash conversion cycles. Taking a three-year time period they tracked the financial performance of these firms, and ran a series of regression models while controlling for industry and firm size.

They found that firms with shorter cash conversion cycles maintain lower levels of invested capital. By comparison firms with longer cash conversion cycles were forced to take on more debt seek equity partners or invest more of their own capital to maintain liquidity. Firms with shorter cash conversion cycles also enjoyed enhanced financial performance. These firms had superior asset turnover and return on investment figures than those with longer cash conversion cycles. Liquidity levels were also found to be higher amongst firms with shorter cash conversion cycles.

However, the study also suggests that small firms are reactive in their management of the cash conversion cycle and are also significantly impacted by changes to it. In their advice to small business managers, Ebben and Johnson note that it is easy for a busy owner-manager to ignore cash flow cycles. When sales are strong it is also likely that owner-managers will become less concerned over the collection of receivables. It is only when sales start to slow down that cash becomes tight and the cash conversion cycle becomes of interest.

As might be expected, the paper highlights the importance of the cash conversion cycle as a tool for small business owners to employ. Understanding cash flow management and monitoring creditors, debtors and working capital requirements within the business are critical. How short or long the cash conversion cycle is can impact on the firm’s inventory levels, discount policies and need to maintain over draught facilities.

Working capital management and profitability

The second paper is by Sonia Banos-Caballero, Pedro Garcia-Teruel and Pedro Martinez-Solano from the University of Murcia in Spain. It was published in Small Business Economics in 2012.

Their study used the cash conversion cycle as a measure of the firm’s working capital management. The cash conversion cycle includes the firm’s management of accounts receivable, inventories and trade credit. Shorter cash conversion cycles indicate a more aggressive approach to working capital management.

This study drew a sample of 1,008 small Spanish firms sourced from the SABI (Iberian Balance Sheet Analysis System) database. It also tracked firm performances over a 5-year time period. A range of industry sectors were examined in the sample encompassing agriculture, mining, construction, manufacturing, wholesale, retail, services and transport. Key variables tested were profitability, the cash conversion cycle, firm size, rate of growth and leverage (e.g. ratio of debt to total assets).

Their analysis found a concave relationship between working capital levels and firm profitability. This suggests that SMEs may have an optimal level of working capital that maximises their profitability. Once a firm moves away from this optimal level profitability is likely to decrease. These findings are contradictory to those from earlier research studies, which suggest that profitability increases with lower levels of investment in working capital.

A limitation of this research was that the size of the firms used in the analysis was larger than most SMEs due to the nature of the database used. However, the paper does highlight the need for small business owners to focus on finding an optimal level of working capital and seeking to maintain it.

Industry differences in cash flow management and liquidity

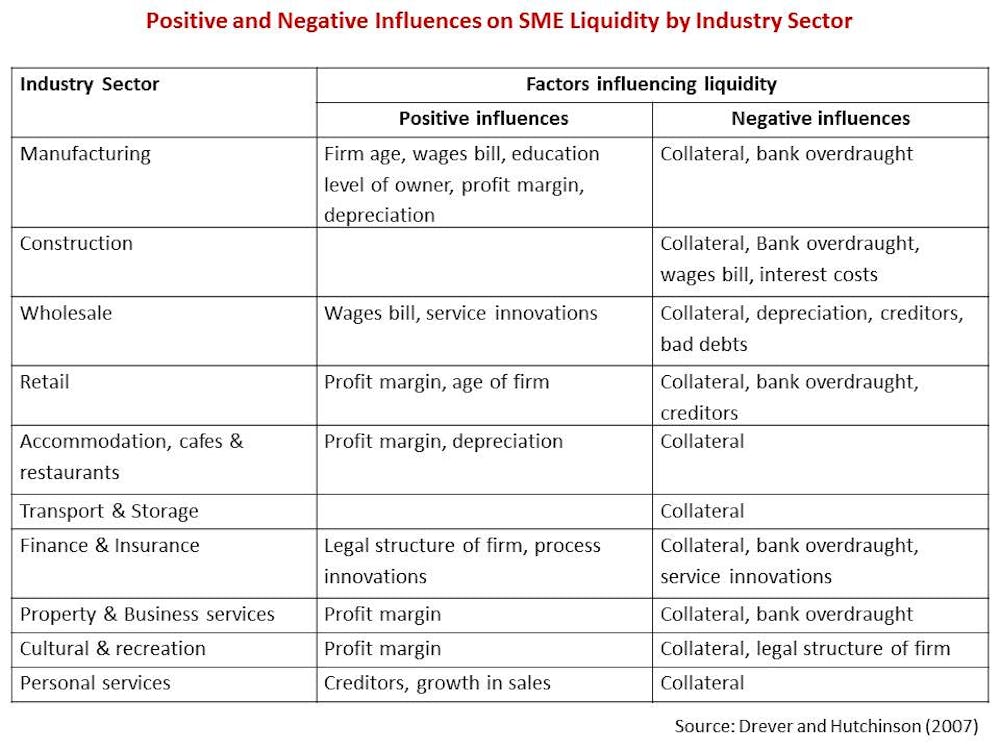

The third paper is by Margaret Drever from Southern Cross University and Patrick Hutchinson from the University of New England, who examined the factors influencing liquidity in Australian SMEs. Their paper, published in 2007 in Small Enterprise Research: The Journal of SEAANZ, drew upon a sample of 3,429 firms from the Australian Bureau of Statistics (ABS) Business Longitudinal Survey (BLS) database. Their methodology used regression analysis with net working capital as the dependent variable, and independent variables relating to the business, the owner-manager and financial measures.

The overall finding from this study suggests that the liquidity levels of small firms are determined by their age, availability of collateral, and presence of a bank overdraught. However, while the influence of firm age was positive, the influences of collateral and bank overdraughts were negative. When examined at an industry level significant differences emerged. The use of collateral (e.g. fixed assets as a proportion of total assets) was found to have a consistently negative impact across all industry sectors. However, there were many significant differences found between firms from different sectors as shown in the following table.

These findings suggest that use by small firms of fixed asset collateral to raise short and long term debt financing has a negative influence on liquidity in SMEs. Although the study does not find strong support for owner-manager or firm related factors influencing liquidity, it does suggest that different factors can impact the liquidity of small firms depending upon their industry sector.

For example, it is worth noting that the liquidity of SME manufacturers may be positively influenced by the age of the firm, the size of its wages bill, the level of education of its owner as well as it profit margins and level of asset depreciation. By comparison service innovations and the size of the wages bill appear to have a positive influence within wholesale businesses. For small firms in the personal services sector liquidity is enhanced by growth in sales and control over creditors.

Lessons to be noted

These three papers all addressed the issues of cash flow management and liquidity amongst small firms. All drew upon large samples and tracked the firms’ performances over time periods of several years. Their collective findings point to the importance to small firms of effective cash flow and working capital management. If we were to summarise their key findings into lessons for small business owners the following points should be noted:

First, you should monitor your cash conversion cycle by tracking debtors and creditors and setting measures of how long it should take to receive payment from customers and make payments to suppliers.

Second, you should also recognise that cash flow management is an integral part of your firm’s financial system and will impact on its working capital requirements and overall financial performance.

Third, there is a potential relationship between the firm’s profitability and its working capital requirement and each firm may have an optimal level of working capital.

Fourth, each industry may have different factors influencing liquidity levels.

Finally, manage your firm’s cash flow and working capital requirements towards a future in which you no longer need debt financing.

Note: Tim Mazzarol is President of the Small Enterprise Association of Australia and New Zealand (SEAANZ).

SEAANZ is a not-for-profit organisation founded in 1987. It is dedicated to the aim of bringing together small business professionals in practice, education and training, and to promote small business development, communication and dissemination of research, ideas and information.