Universities will feel some funding pain in years to come, as the budget reveals government plans to save A$2.8 billion over the five years from 2016-17 by reforming the higher education system.

This includes a 2.5% efficiency dividend on the Commonwealth Grant Scheme in 2018 and 2019 and other significant changes to reduce expenditure under that program.

In the lead up to budget night, Treasurer Scott Morrison said that universities have “effectively got a profit there of around 6%”:

Now, if you add companies running around today saying that they’ve got 6% profits, when on average it’s less than 1%, you’d be thinking there’s a bit of room there – and you’d be right.

The Conversation contacted Scott Morrison’s office to request sources for his figures but did not receive a response before deadline.

Nevertheless, it is true that many universities are in surplus. Depending on how you crunch the numbers, the surplus across the sector could be close to 6%. But there are good reasons for universities to aim for a surplus, and it doesn’t necessarily indicate that there’s “a bit of room there” for cuts.

Profit vs surplus

First of all, let’s look at the terminology. Universities are not-for-profit organisations and the money they hold at the end of a financial year is a “surplus”. A surplus isn’t the same thing as a “profit” that might be returned to a business owner.

The focus of a not-for-profit organisation isn’t to make a profit. It is to pursue its stated objectives. In the case of universities, these objectives are usually in its state establishing legislation. Not-for-profits commonly have small surpluses or deficits every year.

So, are Australian universities making surpluses of around 6% per year? It depends on how you measure it.

Calculations based on Department of Education and Training data can show that in 2015 the surplus across the university sector was 5.8%. The median university surplus was 5.9%. These figures have been trending down for a number of years. In 2014, the figures were 6.8% and 6.3% respectively.

The Tertiary Education Quality and Standards Agency (TEQSA) - Australia’s independent national regulator of the higher education sector - has a different number.

Its 2015 report analyses university data for 2014 and reports a median net surplus for universities of 4.6%, compared to the 6.3% mentioned in the previous paragraph. TEQSA figures also show the current downward trend, with its median figure for the previous year being 6.1%.

Why the difference in the reported median surplus?

The sector-wide figure derived from Department of Education and Training data is simply net operating result for the year as a percentage of total revenue from continuing operations, with each of these factors being the sum for the entire sector. Let’s call it the “crude” surplus, partly because it ignores the different circumstances of individual universities.

In contrast, TESQA’s numbers are based on adjusted figures for revenue and expenses. Why does TEQSA adjust its figures? Well it’s all about the best metrics and accounting.

Part of TEQSA’s job is to assess the financial position and performance of Australian higher education providers. It uses a variety of financial indicators derived from university financial statements to make these assessments.

Not all Australian higher education providers are the same. One of the major differences is that some are not-for-profit and others are commercial organisations.

In Australia, not-for-profit and commercial organisations are required to use different financial accounting standards.

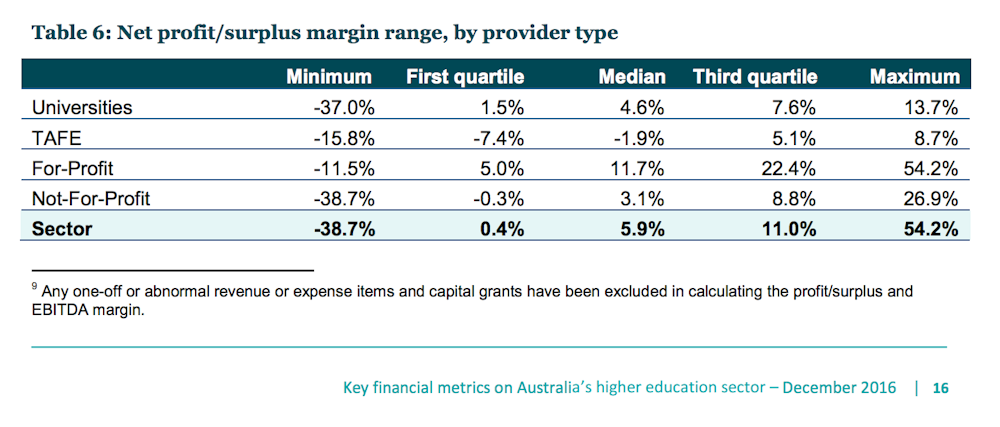

The TEQSA metric which is closest to surplus and profit removes any one-off or abnormal revenue or expense items and capital grants. This produces a metric that is more comparable across provider types and a more reliable indicator of the underlying financial position of each provider.

Differences between not-for-profit and corporate entities

The different accounting standards for commercial and not-for-profit organisations cause a significant number of differences in their financial statements.

A not-for-profit entity is required to recognise a grant - such as a research grant or a grant for capital expenditure - as revenue on the day it is received. The related expenditure is recognised when it is incurred and this may be in a subsequent year.

This contrasts with a company, which would usually recognise income only when it has contractually earned it - that is, when the goods for which it is receiving payment have been produced.

So the fact that a university has a surplus doesn’t mean it has a profit to be either reinvested or returned to shareholders. At the end of a financial year, the university may have outstanding obligations to spend the surplus revenue on purposes for which it has previously received grants.

Differences in how capital grants are treated also result in differences in how expenses are incurred.

A not-for-profit entity would generally recognise a capital grant in the year it is received and the resulting asset would be depreciated over its life.

In contrast, a commercial entity would generally recognise a capital grant as revenue in a manner that matches the depreciation expense, removing this potential element of fluctuation in revenue and expense items.

The accounting body CPA Australia says that when considering the surplus (or deficit) of a not-for-profit, it’s important to be mindful that even if a significant surplus or deficit is achieved in a particular financial year, this doesn’t necessarily indicate good or bad financial performance in that year.

What other sources are available?

In 2016 an independent assurance, tax and advisory firm, Grant Thornton Australia published a report on the financial health of Australian universities.

It drew on financial information from the Australian Department of Education and Training for the period 2009−2014 and applied methodologies associated with the Test of Financial Responsibility used by the US Department of Education. The report found that:

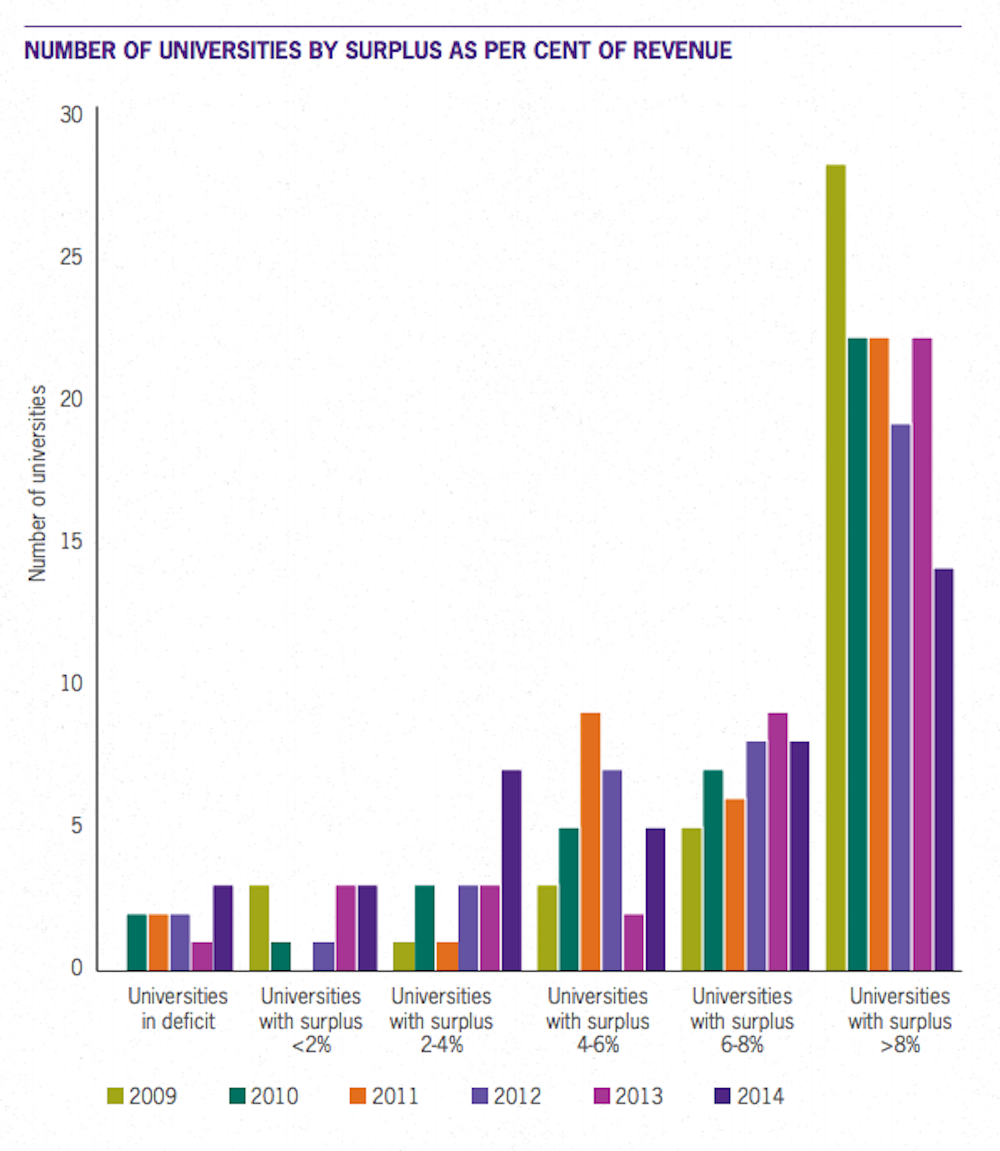

The majority of Australian universities (55%) are currently achieving a surplus of more than 6%; however, the trend in declining surplus as a per cent of income … suggests that the number of universities achieving such surpluses greater than 6% will continue to decrease.

On the overall Test of Financial Responsibility, it found that all institutions met the standards, but five institutions would be subject to additional monitoring in the US. The finding highlights that universities can be in quite different financial circumstances.

What do universities do with their surpluses?

Australian universities have a high degree of autonomy in how they manage their affairs. Their executives and councils make decisions about how the university is run and how resources are internally allocated. They determine the major investment priorities. As with any class of organisation, some are more efficient and competent than others.

TEQSA says the generation of a surplus in a not-for-profit university is “important in ensuring that the provider can fund its operations into the future”.

Its figures for adjusted net surplus show a high degree of variability across universities, which may affect their ability to do this. One quarter of universities had an adjusted net surplus of less than 1.5%, with the lowest being -38%. Around half of universities were in the range 1.5% and 7.6%.

As the CGS grew with demand-driven funding of student places from 2010 to 2013, the government gradually closed off many other grant programs, in particular those providing capital grants. In 2014, it created the Higher Education Infrastructure Working Group to provide it with advice on how to support institutions to create high quality infrastructure.

The group’s final report found that the ability to generate sound operating surpluses was critical to universities’ capacity to make infrastructure investments. It was generally positive about the ability of many to do so.

It did note the difficulties associated with an uncertain funding environment, the many legacy problems in the sector and government imposed constraints on dealing with dealing with them. It also found that:

some suburban and regional universities have no realistic prospect of amassing significant surpluses or developing balance sheets that allow them, acting alone, to effectively access capital markets.

‘A bit of room there’?

Scott Morrison’s view that “there’s a bit of room there” to absorb cuts is not an opinion shared by universities.

The government has to make judgements about whether the impact of reduced resources on the quality of higher education at this time is less important than reducing the commonwealth budget deficit or meeting other expenditure priorities.

The sector wide “crude” surplus discussed above is not a particularly good indicator on which to make a judgement about the ability of particular universities to continue to support high quality teaching, learning and research with reduced resources.

The data show most of Australia’s universities are in reasonably strong financial shape, but their finances have considerably tightened from 2013 to 2015 due to previous savings measures. Further reducing their resources will require additional financial adjustments and managing resources will get harder.

Some universities are already struggling, particularly some dual sector universities which also have been affected by changes in VET funding. At some point, they may well have a good case on which to seek extra financial assistance.