Ben Bernanke prepares to vacate his seat as Chairman of the US Federal Reserve on Friday, making way for for Janet Yellen, just as the developed economies finally seem to be coming right.

Yellen’s impact on the global economy will come from decisions about monetary policy – specifically the Fed’s quantitative easing program – which will be felt around the world. Markets are already jittery.

The Fed holds more than US$3.2 trillion in mortgage-backed securities and US treasuries, mostly purchased under its quantitative easing program introduced to stimulate the economy by massaging medium and long-term interest rates lower.

Already, the reaction of financial markets to this initial cut to the quantitative easing program has been to push yields on long-term treasuries higher. Share markets initially increased in a surprise following this announcement.

But financial markets turned last Friday, falling in anticipation of Bernanke’s final Federal Open Market Committee this week, where a decision to taper further could be taken.

This will be the first regularly scheduled meeting of the year, in which the membership of the committee and potential positions are decided. Economists expect a further decrease of US$10 billion in asset purchases.

Strong growth forcasts

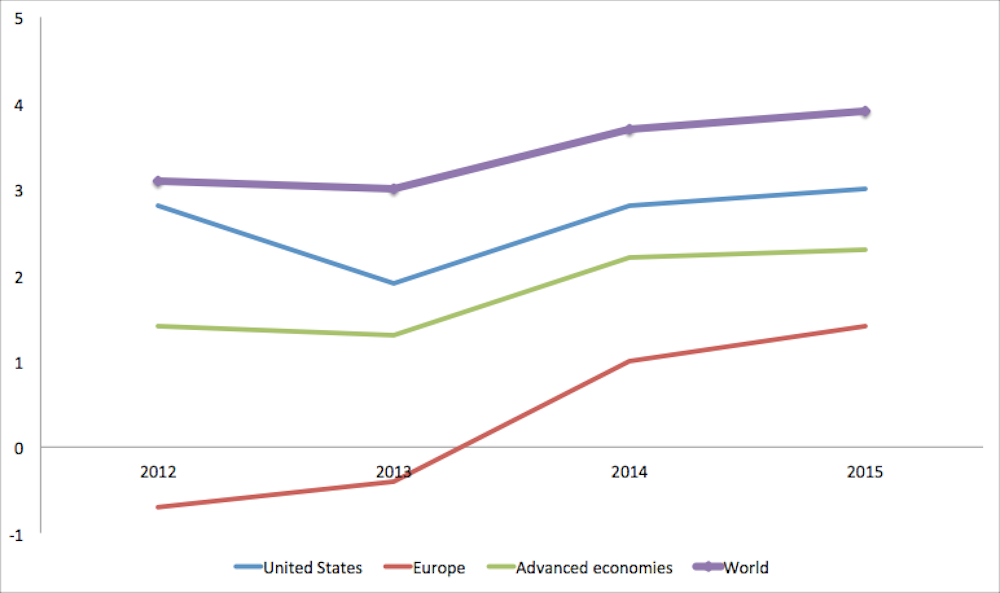

The International Monetary Fund and the World Bank have forecast global growth at a healthy 3.2% to 3.7% for 2014. It is the first time in two years that the IMF has raised its global growth forecast.

In particular, those countries that experienced the most severe economic impact during and after the global financial crisis – the US, the UK and nations in southern Europe – now have better outlooks.

But that positive scenario isn’t without risks. The IMF also cautioned central banks in the improving economies against lifting interest rates – or decreasing money supply – too soon as their economies return to stronger growth, for fear modest inflation could turn into deflation.

The stark increase in money supply, in response to the global financial crisis, in key economies hasn’t resulted in the asset value increases that economic theory might predict.

So, lifting interest rates and decreasing money supply could result in falling asset values – which would be a problem for borrowers and could result in another peak of credit defaults, triggering an economic downturn.

Country-specific issues, like a moderation of growth in China, could exacerbate these problems. The IMF concludes that countries shouldn’t increase interest rates and slow down quantitative easing programs for now.

Time to taper?

That puts Yellen in the spotlight in coming months. Bernanke has already taken the first step in slowing down the Federal Reserve’s asset purchase program, reducing its monthly security purchases by US$10 billion to a still large US$75 billion.

Yellen is expected to re-balance the Fed’s position given new economic information and continue to increase the transparency of its monetary decisions. Certainly, the current policies of the Federal Reserve Bank have the potential to destabilise the US economy and result in either deflation or inflation. Will Yellen act and take the tough decisions?

Yellen could continue to decrease asset purchases, which will lead to higher US treasury yields, with follow-on effects in other countries. The mere expectation of a reduction this week has already led to declines of currency values and net investment outflows in emerging markets. Tapering may exacerbate other challenges these countries face, like political and economic uncertainty in Argentina, Ukraine, Turkey and Thailand.

However, Yellen has expressed concerns about US unemployment, which remains relatively high. The IMF warnings support this concern, which means it is possible that Yellen may continue the quantitative easing program for longer than was expected. In this scenario, the US monetary policy may change little and continue to support global growth.

Where will Australia head?

What may matter most for Australia is economic growth in Asia, in particular the growth of its key trading partner China. China has recently announced an economy growth of 7.7% in 2013, relatively low compared to the past. Economists expect the growth in China and some of its neighbours to decelerate further.

China has now reached a higher level of wealth and the question is whether it will be able to maintain the sort of economic growth seen in recent years. This may require an increase in domestic consumption, and the development of innovative products.

Unlike other developed countries, Australia has avoided the recent financial crisis, public debt levels are low, other trade partners are geographically diversified, and the Reserve Bank of Australia has a variety of options to conduct monetary policy and support the economy. Whether this proves to be sufficient to deal with the potential challenges from the Asia region that may arise, remains to be seen.