The recent announcement by Prime Minister Kevin Rudd to offer lower company tax rates for northern Australia has received a range of positive and negative criticism. However, it is not a new idea. As long ago as 2001 Dr Ian Manning, from the National Institute of Economic & Industry Research (NIEIR), published a report sponsored by the Institute of Chartered Accountants and Local Government and Shires Associations of NSW.

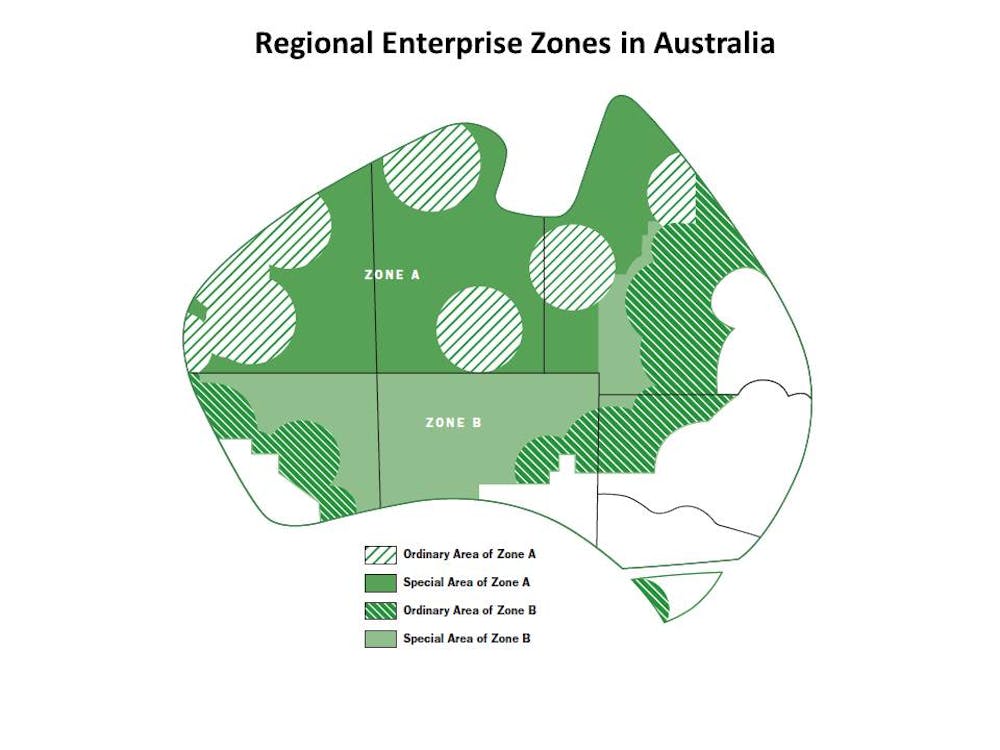

This took a much broader and well-considered approach to the issue of offering differential taxation regimes across Australia. The report identified four enterprise zones that might be part of a nationwide strategy focused on enhancing regional economic development. These zones are illustrated in the following diagram where the “Special Areas” are shown that would potentially attract differential tax treatments based on need.

As can be seen from the diagram above, the assessment of where special economic zones are to be found did not look simplistically at the north versus the south. Instead it recognised that economic and social disadvantage are found across the nation in many areas. A conclusion from this study was that:

“Eligibility for enterprise zone assistance should be based on objective criteria of disadvantage and on the production of a development strategy which ensures that assistance is put to the best use.”

The research undertaken by Dr Manning suggested that the focus of any enterprise zone program should be driven by “objective criteria” that included consideration of:

1) Unemployment rates within the region;

2) The number of social welfare recipients within the region;

3) The value of rural land per farm property and farm production statistics;

4) The amount of export capacity within the region with a particular focus on small to medium sized enterprises.

The study examined comparable regional economic development strategies in other countries and noted that the lack of “regional governments” required that any future strategies be focused around a division of responsibility between state and local governments.

Arguments that the Australian Constitution restricts the ability of governments to offer differential tax incentives across regional areas were dismissed as being “ill founded”.

Instead it was claimed that “Advice from Special Counsel finds that there is no constitutional impediment to Commonwealth participation in the setting up of such Zones or providing for tax incentives in these designated areas”.

Overall the message from this twelve year old report was that there had been a successful intervention by government in the development of regional Australia in the 1900s and 1920s. Yet the 1970s saw a transition towards cost cutting and the retreat of government from intervention in the process of economic development.

So in summary the idea of government intervention via such things as tax incentives to help stimulate economic growth in regional areas has some merit. However, the targeting of such incentives should be part of a wider regional economic development process that targets areas on the basis of objective criteria.

To argue that northern Australia is a special case when there is high unemployment and other social and economic need elsewhere in the nation is to miss the sophistication of well-considered analysis that has been around for over a decade.