What on earth is going on in the oil market? Does the recent 60% collapse in oil prices in six months really reflect shifts in underlying supply and demand for crude oil? I’m afraid not, as I have been predicting for more than three years. Here’s what has really been happening.

When an oil market is over-supplied, it causes something called a “contango”. This is where the spot price of oil (the price for immediate delivery) is less than the forward price – a reverse of the normal situation.

The oil market is currently significantly over-supplied, partly from a period of strong demand from emerging economies and partly because the high price made more expensive forms of petroleum production viable, such as US shale, Canadian tar sands and deep-water plays. There is also a very significant contango of more than $6 per barrel for a six-month period.

There was another massive contango in 2009. This was the middle of a period where the oil price spiked from $80 to $147/barrel in July 2008, collapsed to $35 within six months and then regained $80, all within two years.

You might have expected the contango during a time of falling prices, signalling that the market was over-supplied, but it remained once prices started rising again. This surge in prices suggested that physical demand was exceeding supply, which indicated market under-supply. So which was it?

This remains an unexplained paradox. Despite the economic crisis, global production and consumption of physical crude oil varied by no more than 3% during that period. To understand what has happened this time around, we need to explain this first.

The market reality

Until about 20 years ago, oil-futures trading existed purely to help oil producers and refiners cope with the ups and downs of the market by hedging against big shifts in the price. In the 1990s, investment funds entered the scene, which made more funds available for hedging. But there were drawbacks: everyone involved in the trade took a cut, and there always came a date when the oil had to be delivered.

Although futures trading is still big business, the costs and drawbacks of exchange trading make off-market trading attractive. A prepay agreement is such an off-exchange agreement directly between producers and consumers. Though a form of prepay was involved in the Enron collapse of 2001, it appears to have reached the oil market three years later. It is my understanding from a very highly placed market source that between 2004 and mid-2008, a major oil company routinely entered into prepay crude-oil transactions with a big investment bank (albeit there is no suggestion of wrongdoing, unlike in the Enron case).

It worked like this: the bank loaned money interest-free to the oil company in exchange for a loan of oil. A different part of the bank then entered into matching transactions with investment funds, where they invested in this loaned oil. This was not speculative investment but putting money into oil as a hard asset that would protect against inflation.

This arrangement appears to have been one of the forces which drove up oil prices towards their 2008 peak. Speculation would also have been instrumental in the short term, but it couldn’t have sustained high oil prices over a period of years.

Enter the Saudis

When the price of oil plummeted late in 2008 as the credit to pay for oil dried up, it would have been deeply uncomfortable for big oil producers such as the Saudis. Saudi Arabia depends on a high oil price to fund its hefty public spending commitments.

The oil-based relationship between the US and Saudi Arabia goes back a very long way. My theory is that a bargain was struck at some point during the oil price crash of 2008-09.

The Americans would have guaranteed a high oil price ($80/barrel, perhaps, below which the price never fell between autumn 2009 and autumn 2014). In exchange, the Saudis might have ensured that the price of US gasoline did not exceed a level (say $3.50/gallon) at which President Obama’s chances of re-election in 2012 might be compromised. As the only player big enough to move the market, the Saudis would have been the only country capable of this.

According to the former Saudi oil minister Sheikh Zaki Yamani, such interventions are nothing new. He claimed that the 400% oil price increases which took place in 1973, and which were blamed on OPEC, were actually secretly engineered by the US and UK to finance more expensive production in places like the North Sea and Alaska. You could say the same about the need in 2009 to dramatically increase US shale oil production.

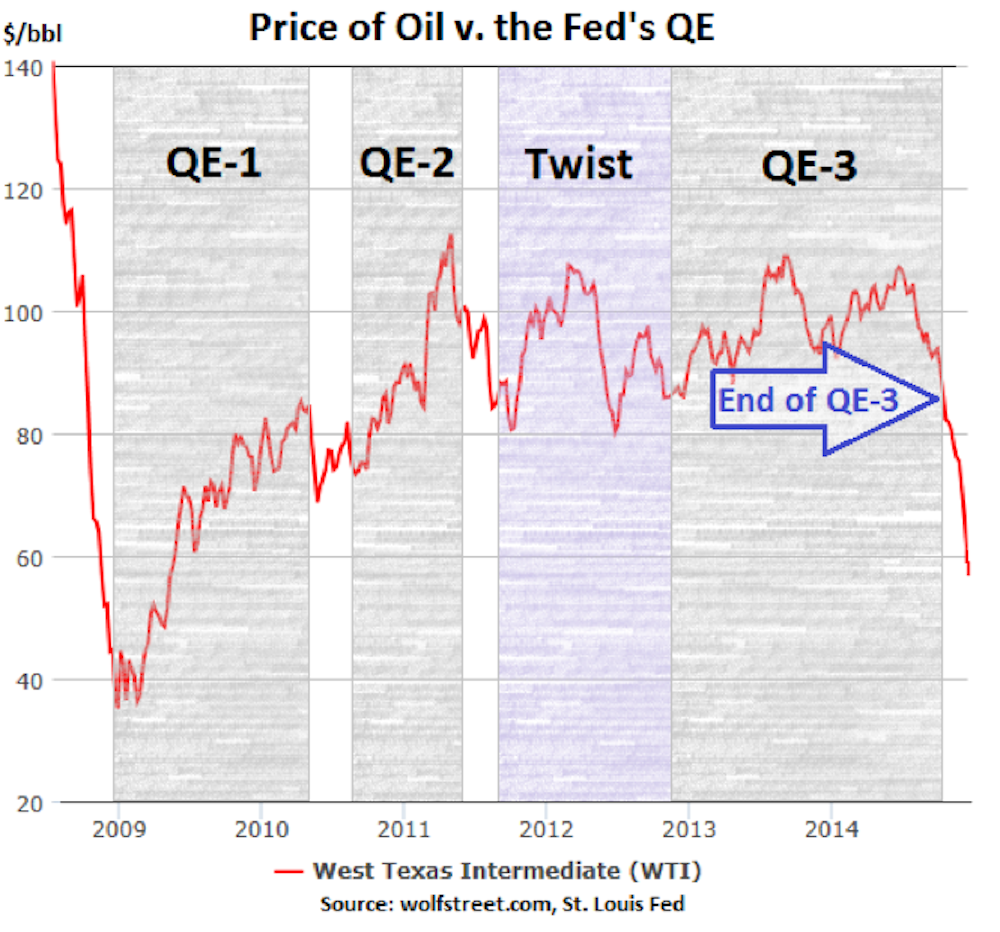

The US decision to begin quantitative easing (QE) certainly put the Americans in a good position to help. Not only did it create a huge wall of new dollars looking to invest in assets, it created big inflation fears. This would have made an asset like oil especially attractive – all the more so if it was done through off-market prepay (at the same time, if anyone had tried to do it on-market, the market would have speculated against them and driven the price down). No one would have thought the QE money would have lasted forever, but it would have been reasonable to assume that it could have helped prop up the price until demand from the likes of China could fill it.

This would both explain the 2009 reflation of the oil price and the big contango – to the market it appeared that there was a big over-supply of oil, but that could be explained by strong prepay demand off-market. This would also explain why the financial crude oil market became almost completely detached from the relationship to physical supply and demand, as well as explaining other anomalies such as the break in the longstanding relationship between oil and natural gas.

The outcome

The high-price years have led both to systemic over-supply from new high-cost US shale oil and demand destruction. This over-supply made the market fragile, but the end of US QE precipitated the collapse. The chart below demonstrates better than a thousand words what happened.

When Saudi oil minister Ali Al-Naimi was recently asked about the prospect of a major deficit in his country’s public finances, his answer was illuminating. Pressed on how Saudi Arabia would cope with this deficit, he said: “We have no debt. We can go to the banks. They are full. We can go and borrow money, and keep our reserves. Or we can use some of our reserves.”

I believe Al-Naimi’s confidence is based firmly upon the fact that Saudi oil reserves have – invisibly to the market – been monetised through the use of prepay credit for the last five years.

This will give the Saudis a softer landing from lower oil prices than might otherwise have been the case. But this still represents the definitive end of an oil-market paradigm of domination by market middlemen which began to develop in the early 1970s after OPEC first began to exercise market muscles which have now almost entirely wasted away.

Recent comments from dissident Saudi prince Alwaleed bin Talal that we will never see $100 oil again are undoubtedly correct. There will be a huge amount of unconventional oil that would become viable at that price, so that if the oil price returned to that level, there would rapidly be a big glut on the market that would suppress it again.

In recent months we have truly seen the end of an era. If my theory is right, there has been a massive market manipulation behind the scenes. If it is wrong, the world’s leading oil producers, traders and financiers have yet to come up with an explanation that remotely fits the facts.