We can now safely say that deficit elimination and public debt reduction were never central to George Osborne’s long-term economic plan. Take the casual way the chancellor pared down a planned budget surplus for 2019/20 [(from £23bn to £7bn)](http://www.bbc.co.uk/news/business-31942068](http://www.bbc.co.uk/news/business-31942068), having long ago ditched the once-essential balanced budget target for 2015/16 as proof. The real “long-term plan” was to let companies make more profit, even if it meant the public and household sectors going further into the red.

Back in 2010, delivering the City of London’s Mais Lecture, the Chancellor of the Exchequer told his business-focused audience that:

When our households, our banks and our government are so indebted, raising the real rate of return on investment is the only sustainable route to prosperity … By embarking upon a series of reforms that will raise the real return on investment, we can raise the rate of investment right now.

Budgets since June 2010 have relentlessly stuck to that task. To raise business investors’ return, the main rate of corporation tax has been dropped to 21% from 26% since 2011 and is soon to match the small-business rate of 20%. The wage subsidy introduced by the previous government’s employee tax credits has been supplemented by direct subsidies for younger workers, and other tax breaks for capital expenditure, now defined to include research and development.

These policies have undoubtedly helped to revive the return on private sector investment, according to the best available measure for what businesses get back for what they put in. Non-financial companies’ net rate of return on capital employed, excluding the volatile North Sea oil sector, climbed back to 12% by 2014, a level last attained in 1998.

Higher corporate profitability has, as promised, been followed by a rise in the UK’s rate of investment. This doesn’t show in the data for gross domestic fixed capital formation, which as a proportion of GDP has levelled off at 16% since 2009, after dropping from 18% in 2005-8. But that broad measure includes households’ property purchases, and the public sector programmes which the chancellor cut sharply in 2010.

More precisely defined private sector business investment has risen steadily, from 8.5% of GDP in 2010 to 9.9% across the first three quarters of 2014, according to the latest GDP data. So it’s mission accomplished, on the terms the chancellor set himself in early 2010.

A high price for higher returns

Achieving this goal has required a heavy sacrifice of the chancellor’s other start of term pledges, especially that of balancing the budget, now postponed four years to 2018/19.

Corporation tax receipts haven’t risen in the way that proponents of the rate-cuts hoped. And much of the substantial job creation since 2010 has been at rates of pay too low to generate tax revenue.

Building up demand for what businesses produce, when households don’t have much more to spend, as meant re-mixing another siren call from 2010. Osborne warned his Mais Lecture audience that “the overhang of private debt in our banking system and our households weighs heavy on future prosperity.”

Banks have since brought their debts down, with generous treasury and Bank of England help. But after a brief period of payback, UK household debt started rising again in 2011, with any ongoing improvement for homeowners’ finances now dependent on rising house prices. Household consumption will contribute 1.6 percentage points to this year’s forecast 2.5% GDP growth, compared to just 0.5 points from business investment, with the same pattern continuing to 2020, according to the Office for Budget Responsibility analysis accompanying Wednesday’s budget. To achieve this, households’ gross debt to income ratio is forecast by 2019 to have risen to 170%. The eagle-eyed will notice that this exceeds its pre-crisis peak in 2008.

Investment disconnect

Confirming that it is consumption, not business investment, that has underpinned the return to growth, Bank of England Monetary Policy Committee member Ian McCafferty noted a year ago that:

A broad-based recovery in activity – which must mean a recovery in household spending, which accounts for 60% of gross domestic product (GDP) – is a prerequisite for a recovery in business investment, not the other way round.

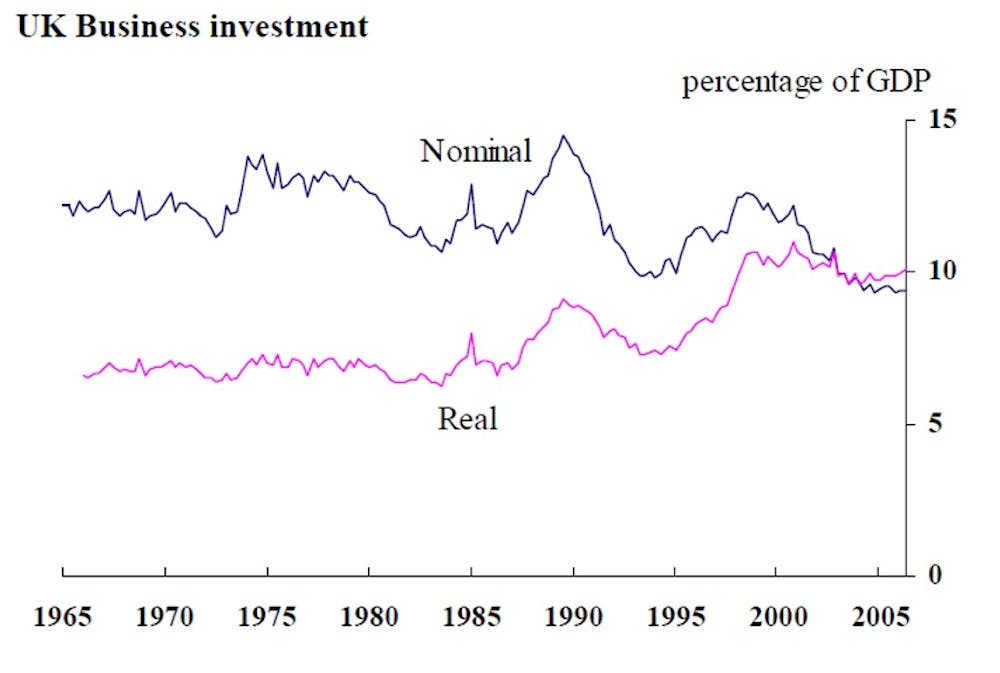

The lagged response of investment may be one reason for the failure to revive labour productivity since 2008, which underlies the slow wage growth. But there’s an unsolved puzzle from the pre-crisis period that Osborne might have done well to study before pinpointing investment and its rate of return as the key to prosperity. The tranquil decade before 2008 was great for corporate profitability – and featured a trend decline in the investment rate, as the chart below shows.

The pre-crash economy grew without needing faster accumulation. And before 2000, UK corporates regularly posted world-leading profitability (far above other EU countries’) without this translating into stronger investment or growth.

Osborne’s budgets have undoubtedly made many businesses happy. But not enough to make them splash the private cash sufficiently for his unprecedented monetary and fiscal stimulus to be safely withdrawn.