The Australian economy appears to be benefiting from the current expansionary stance in monetary policy, despite uncertainties in the global economy.

The CAMA Shadow Board is 71% confident that the cash rate should remain steady at 2.5%. The probability attached to a required rate cut equals 4% while the probability of a required rate hike has increased to 25%.

The Australian labour market is showing promising signs, with a surprisingly robust increase in employment in February 2014 (an increase of 47,000 for overall employment and 80,500 for full time employment). As the participation rate also rebounded from 64.49% to 64.85%, the unemployment rate remained unchanged at 6%.

Inflation remains within the 2-3% target range. The Australian dollar has appreciated considerably, this week making a four month high of over 92 US cents. Asset markets, in particular housing, remain buoyant. Overall, domestic consumption and production indicators point to a marginal improvement. Encouragingly, the AIG manufacturing index rose to 48.6 in February (compared to 46.7 in January 2014 and 45.6 a year ago) and the ACCI New Orders increased to 26 in the first quarter of 2014 from 13 in the fourth quarter of 2013.

At the moment, the greatest threat to the Australian economy comes from the international economy. US economic data is still mixed but improving. There is growing confidence in the likelihood that the Federal Reserve Board will tighten monetary policy by the end of this year.

Of considerable concern is the fallout from a deterioration of the political crisis engulfing the Ukraine and Russia. This might include trade and investment sanctions, higher energy prices and volatile capital flows. China’s economy looks like cooling further, pointing to a softening of commodity prices, coal in particular.

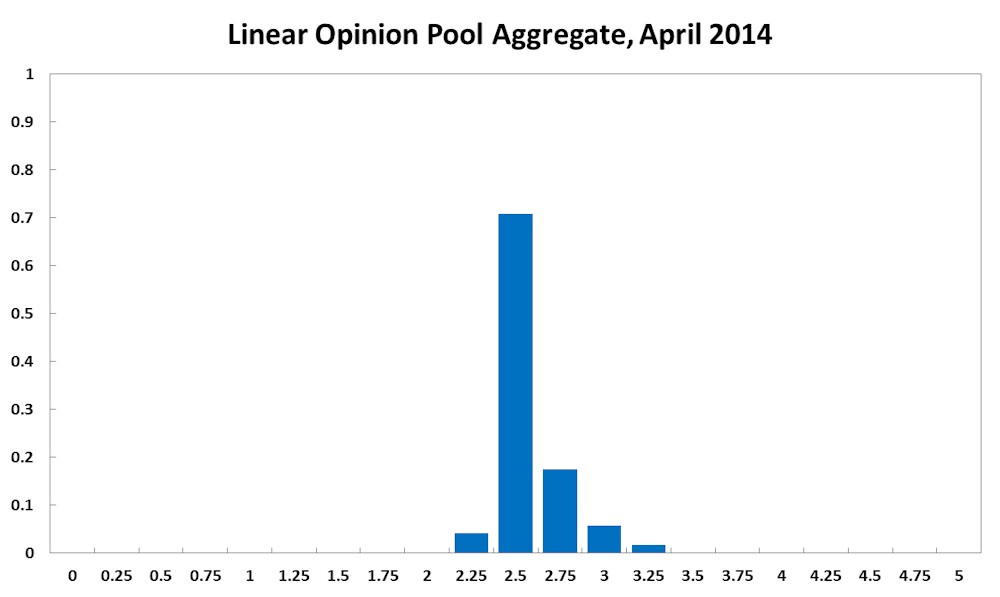

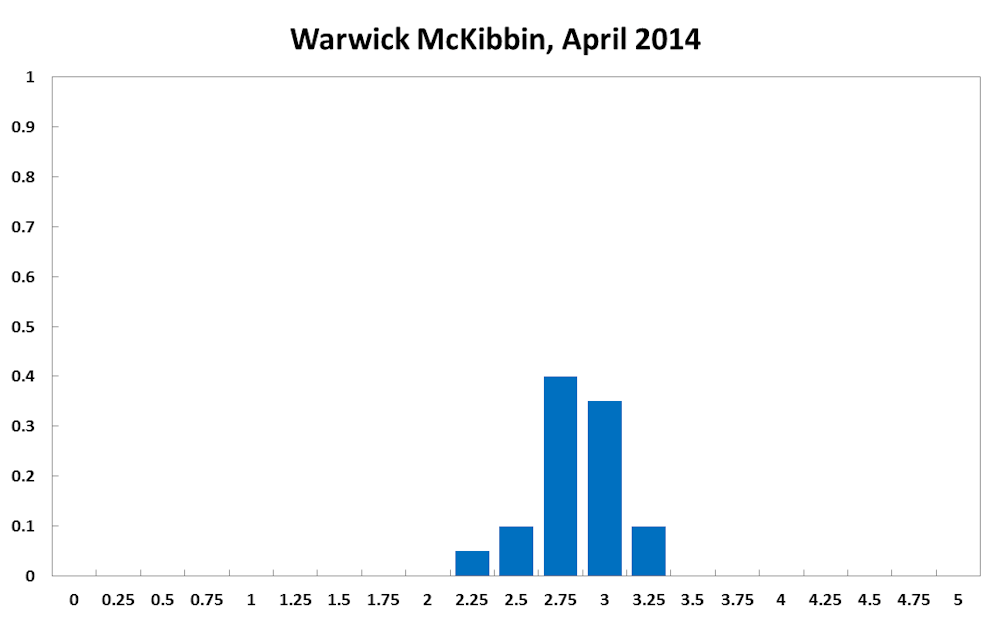

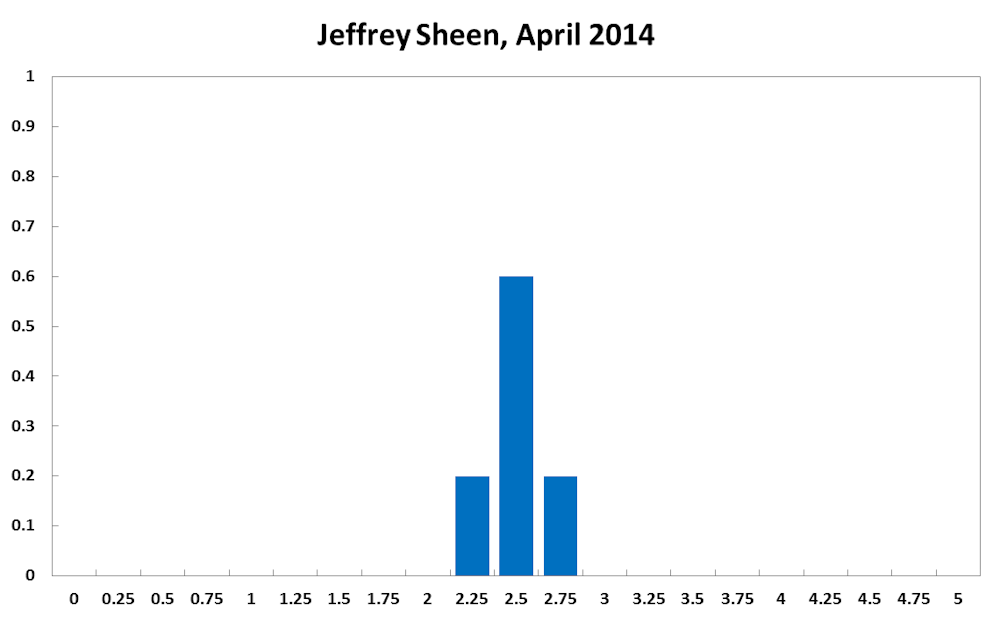

The consensus to keep the cash rate at its current level of 2.5% remains strong. The Shadow Board’s confidence in keeping the cash rate steady equals 71% (73% in March 2014). The probability attached to a required rate cut equals 4% (8% in March) while the probability of a required rate hike has increased to 25% (19% in March).

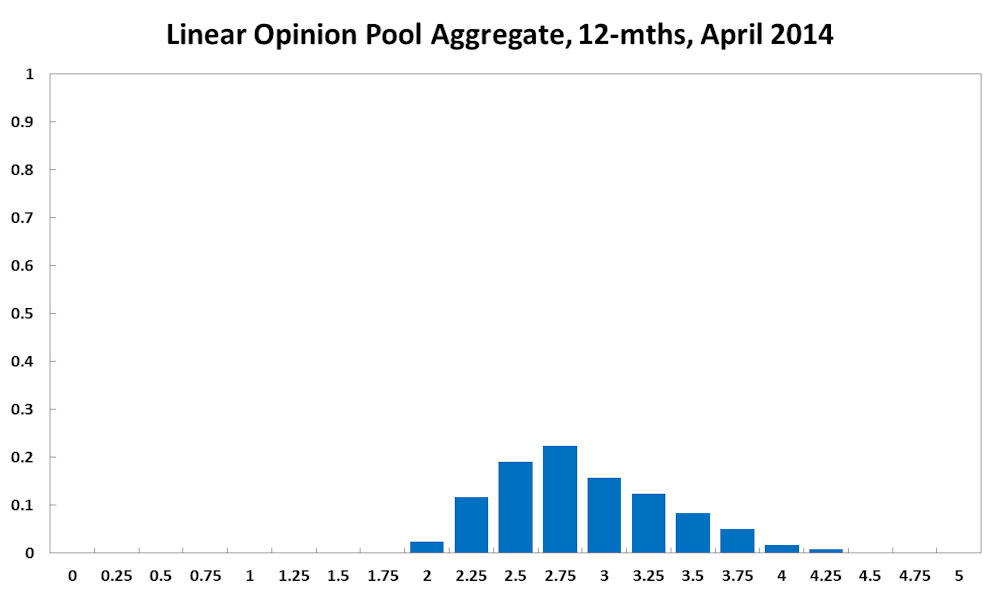

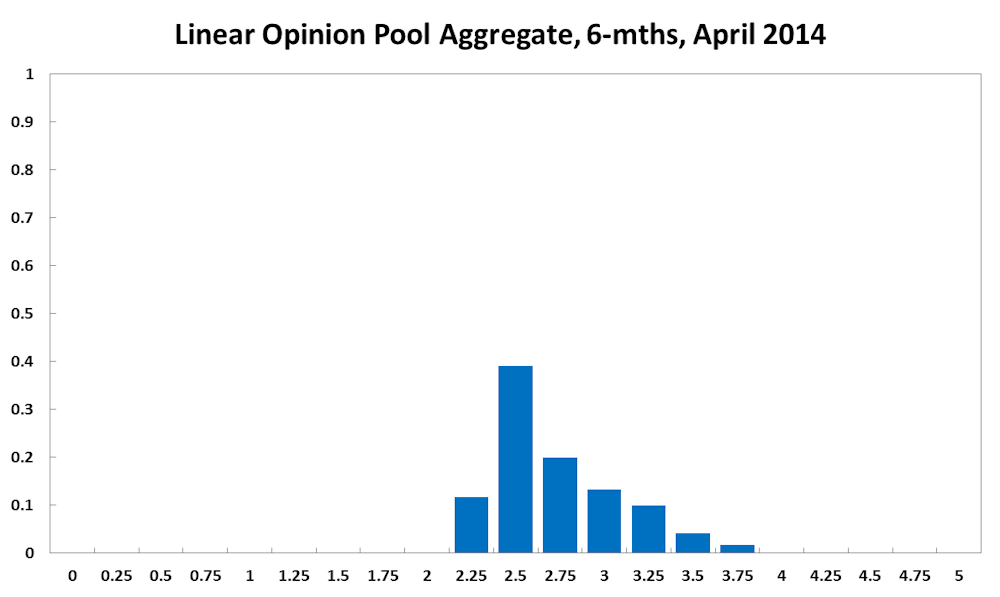

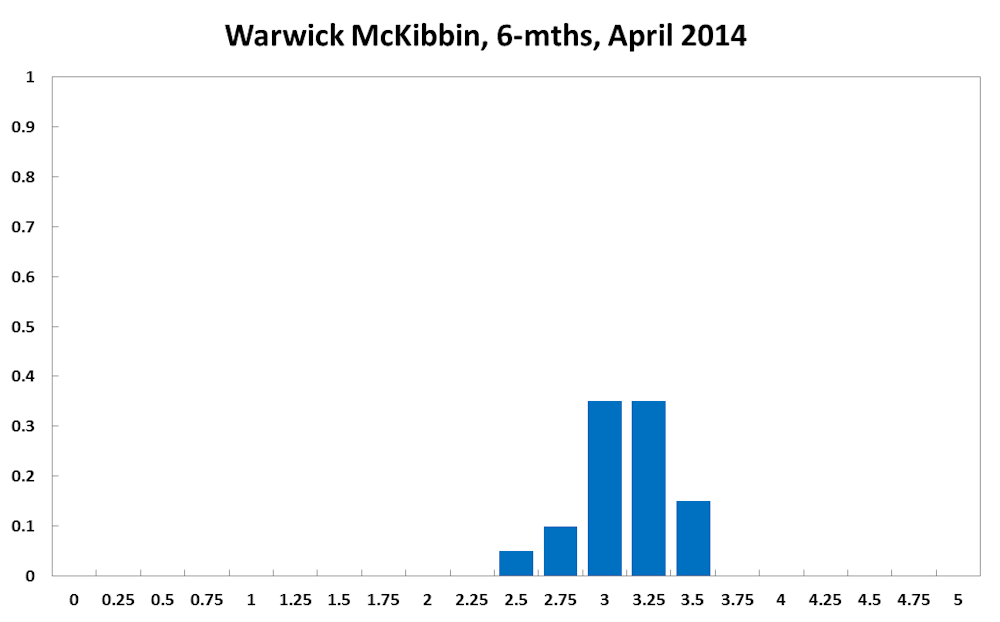

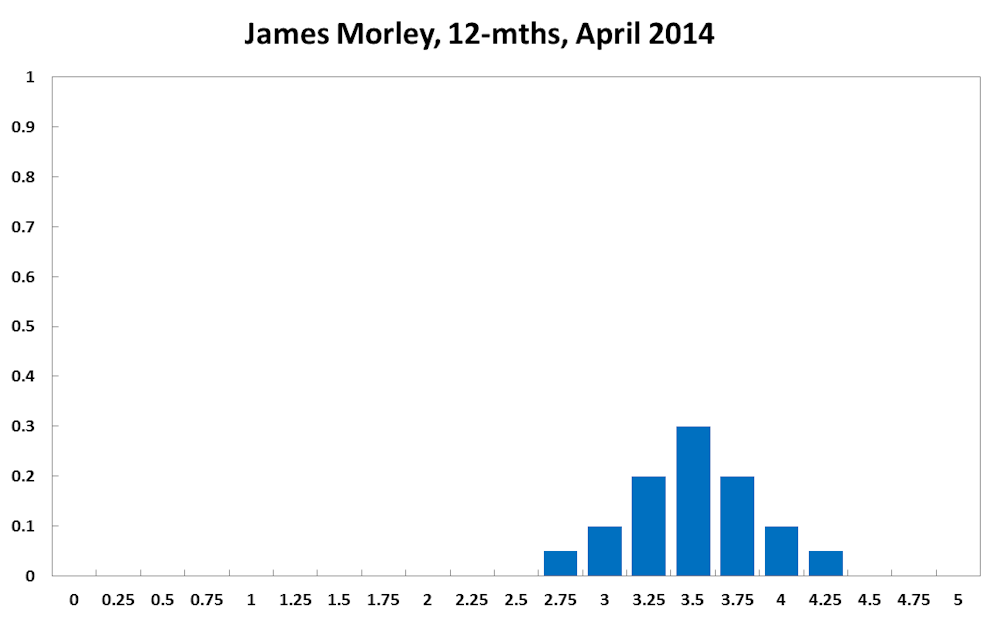

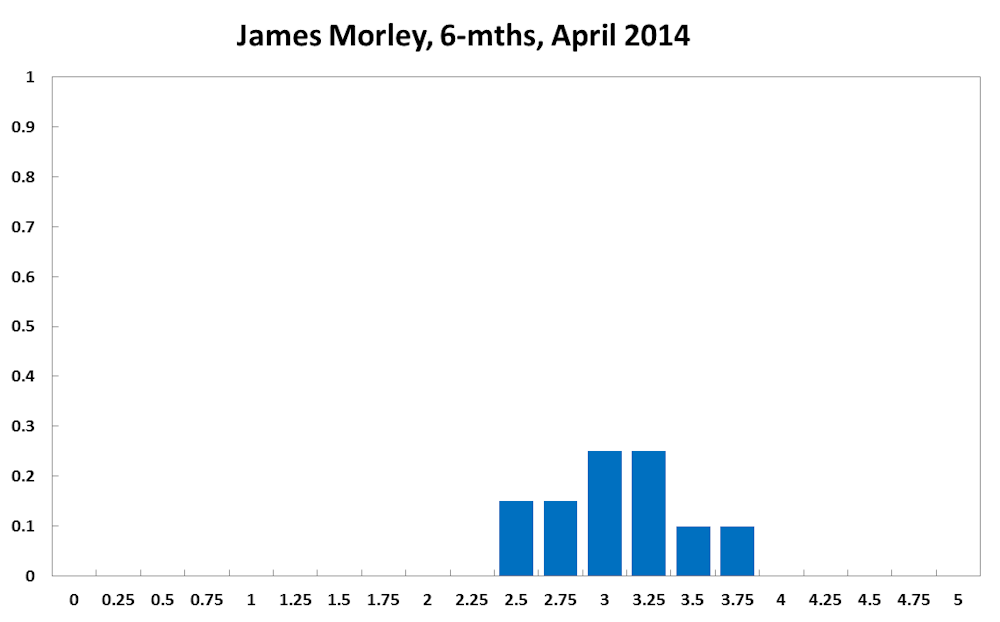

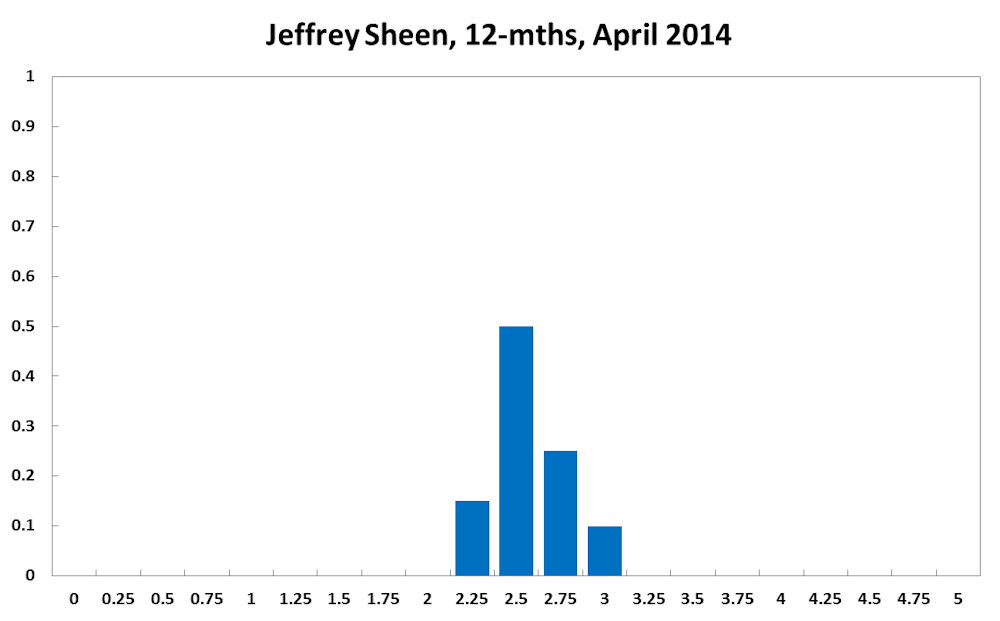

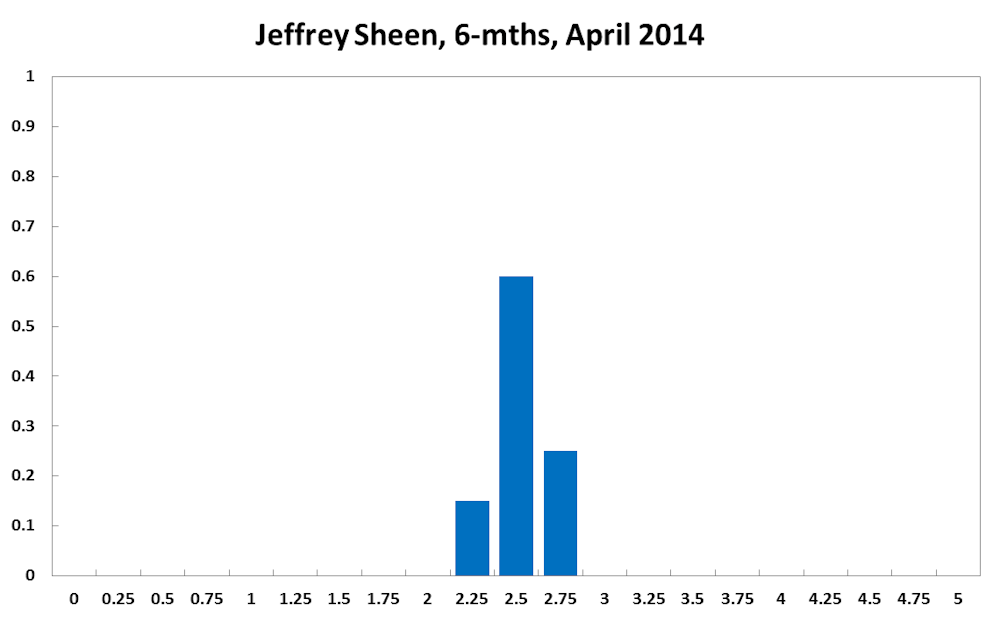

The six months probability that the cash rate should remain at 2.5% is unchanged at 39%. The estimated need for an interest rate increase has increased from 43% to 49%, while the need for a decrease has fallen to 12% (19% in March). A year out, the Shadow Board members’ confidence in a required cash rate increase has risen to 67% (54% in March), the need for a decrease dropped to 14% (down from 19% in March), while the probability for a rate hold has fallen to 19% (down from 26% in March).

Note: Mark Crosby, Mardi Dungey and Bob Gregory were unable to vote in this round, so the linear opinion pool aggregate is based on the remaining six members.

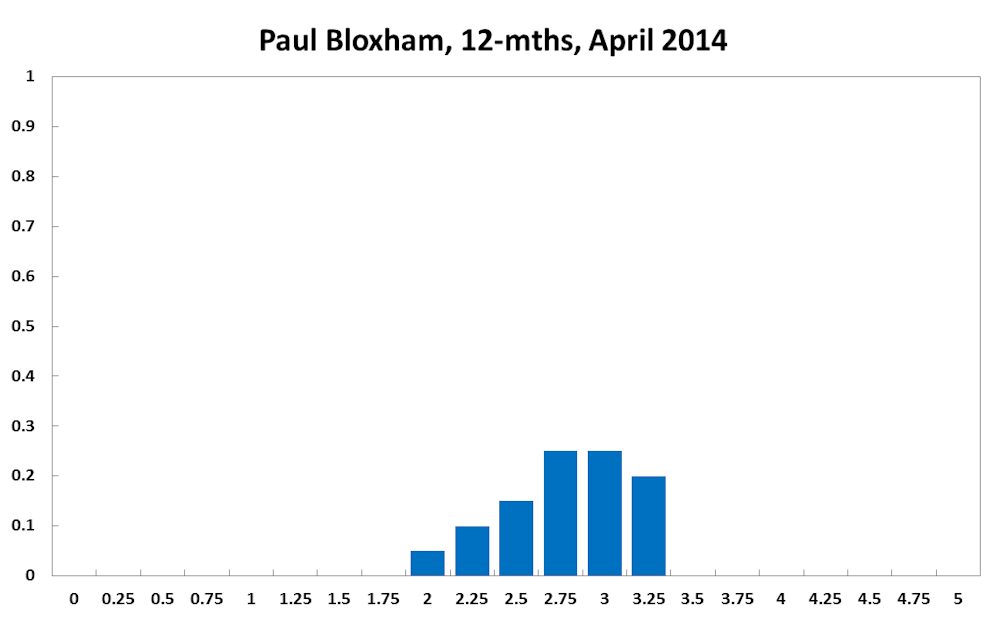

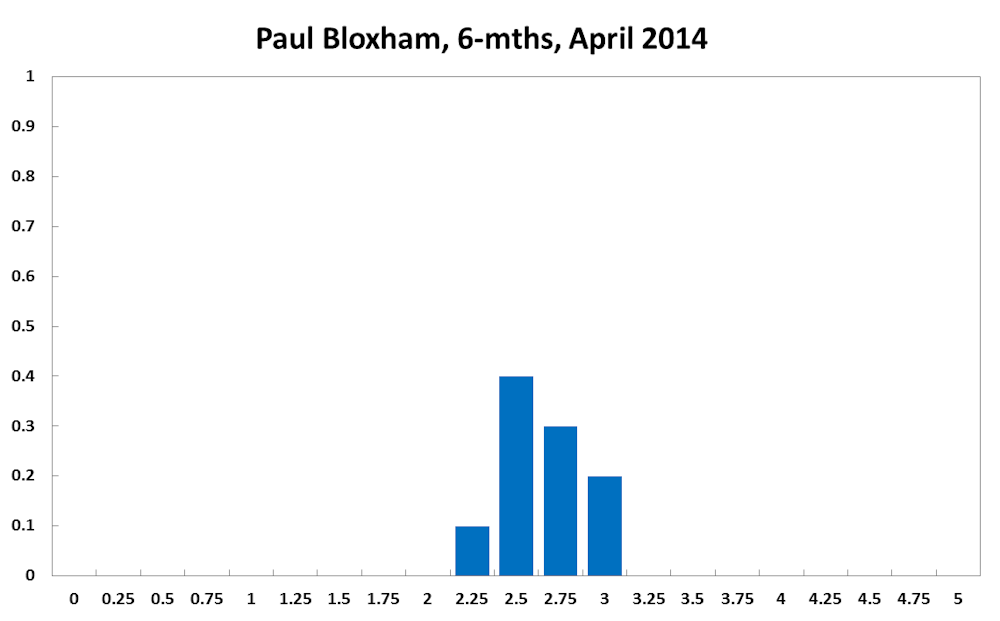

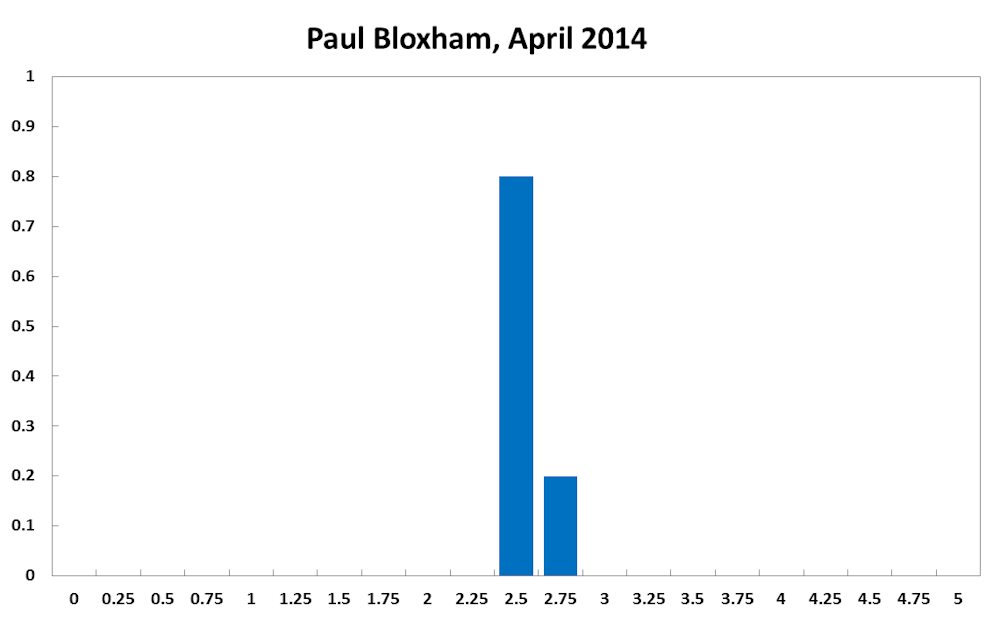

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

Local activity indicators are continuing to show that growth is picking up. Retail sales are growing at their fastest rate since 2010, housing prices continue to rise at low double digit annual rates, forward-indicators suggest that residential construction activity is picking up pace and the business surveys report an improvement in conditions.

This month also brought indications that the pick-up in activity is starting to feed through to a lift in employment. If coming months bring further signs of improvement in the labour market, this would start to suggest that the current very stimulatory setting of monetary policy may be unnecessary.

A further pick-up in activity could also tilt the inflation risks to the upside and, with inflation already in the upper half of the target band, would suggest that rates may soon need to rise to keep inflation comfortably within the target band. I recommend that the cash rate is left unchanged this month, but looking forward, I see it as more likely than not that the cash rate will need to be higher than its current level in 12 months time.

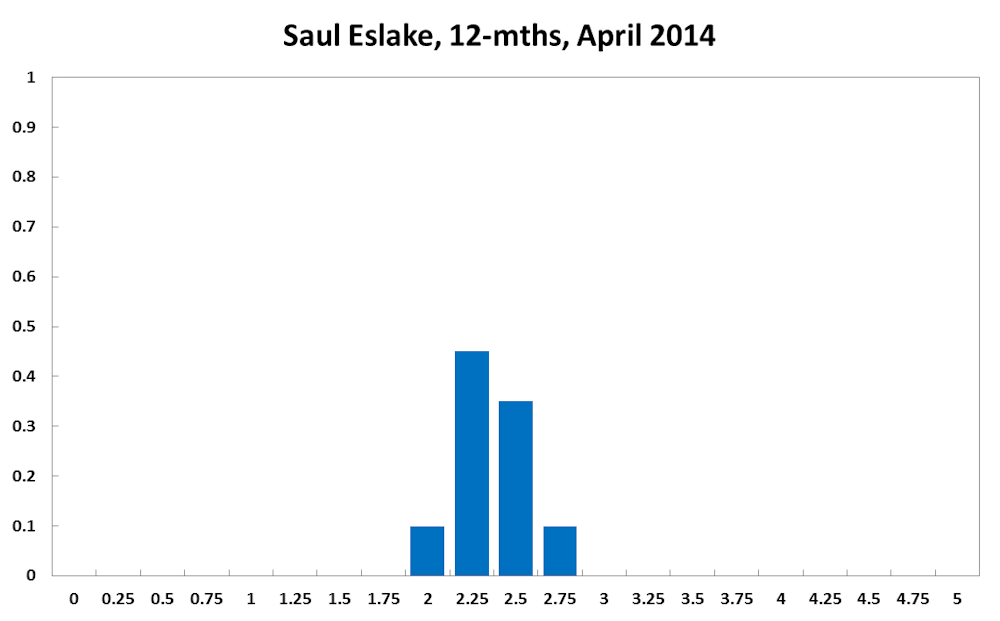

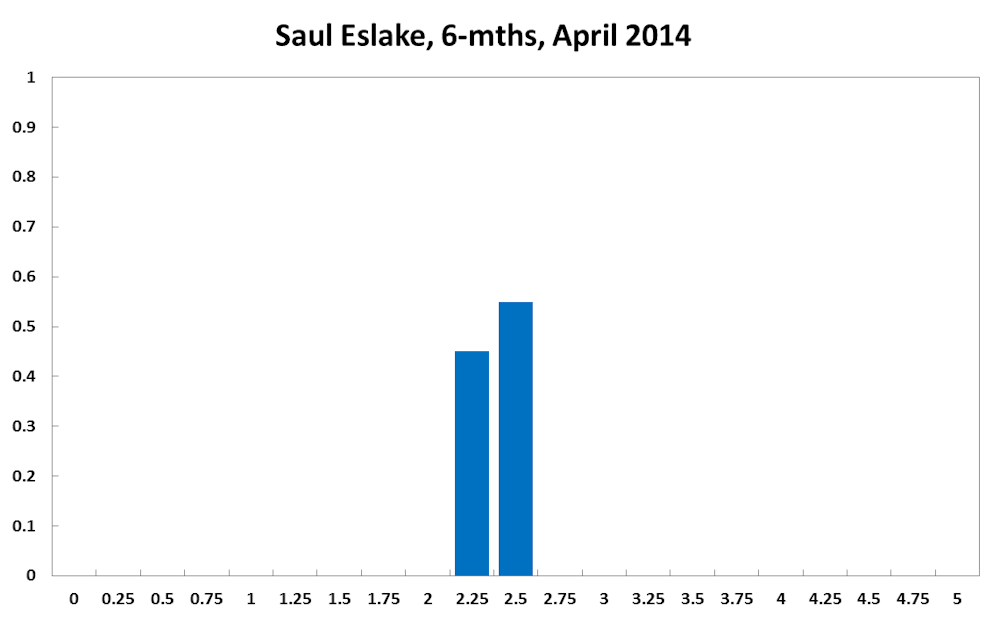

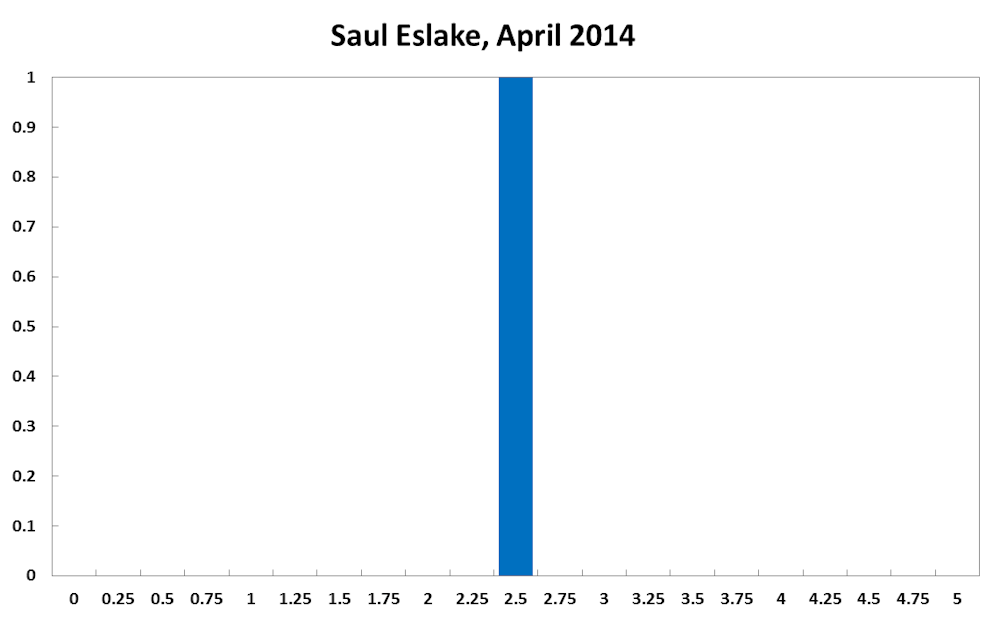

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia:

No comment.

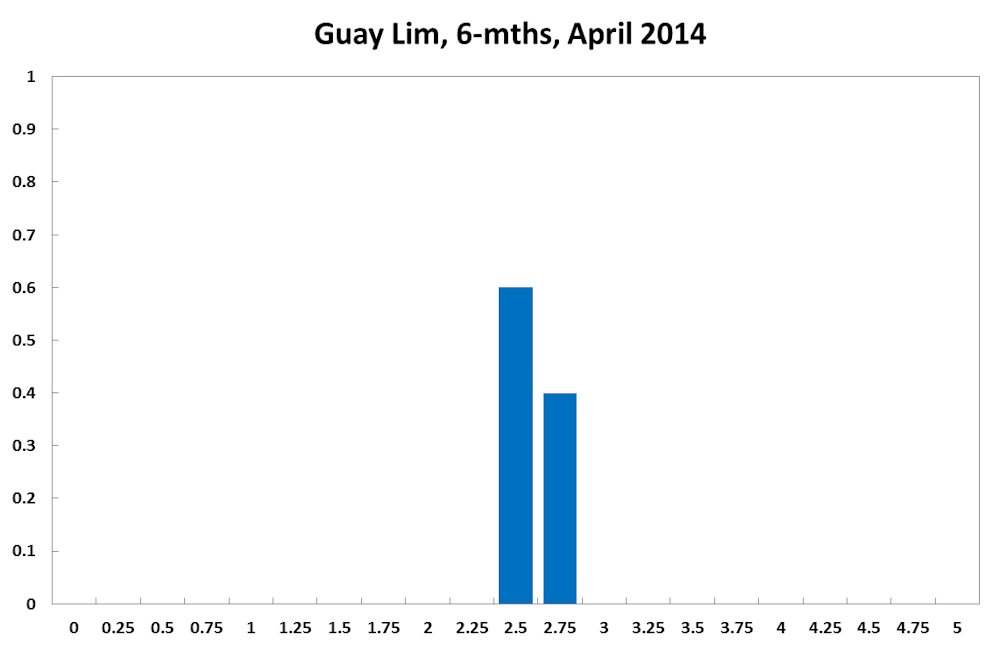

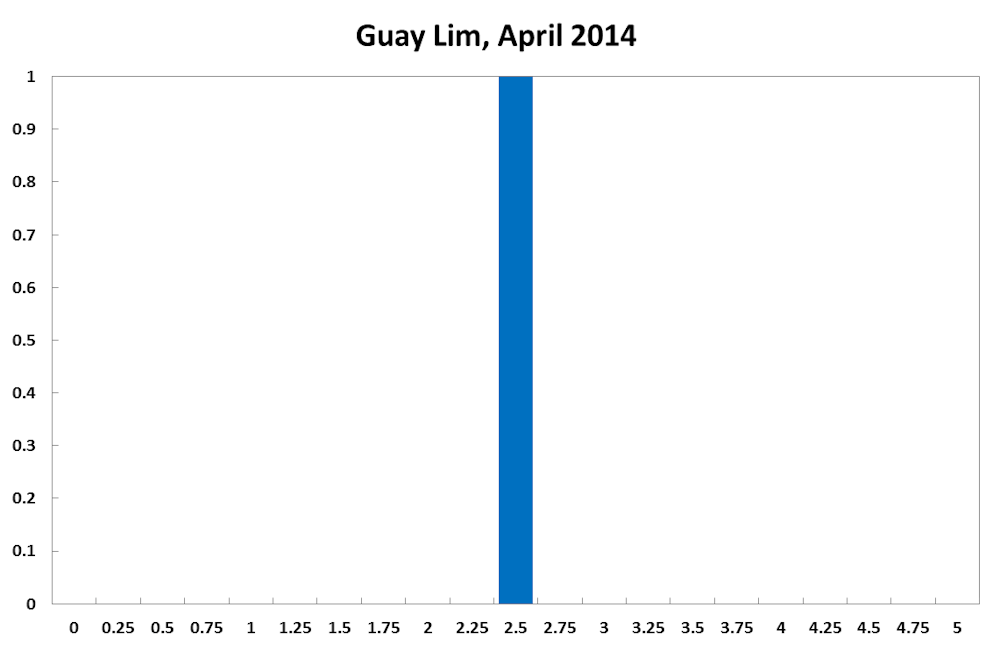

Guay Lim, Professorial Research Fellow and Deputy Director, at the Melbourne Institute of Applied Economic and Social Research, Melbourne University:

No comment.

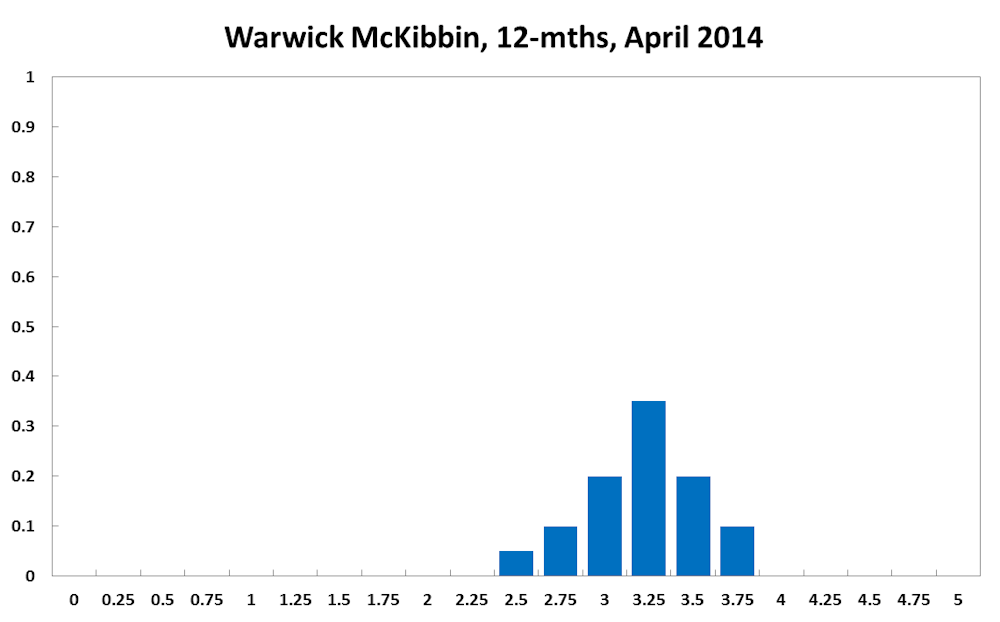

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University:

No comment.

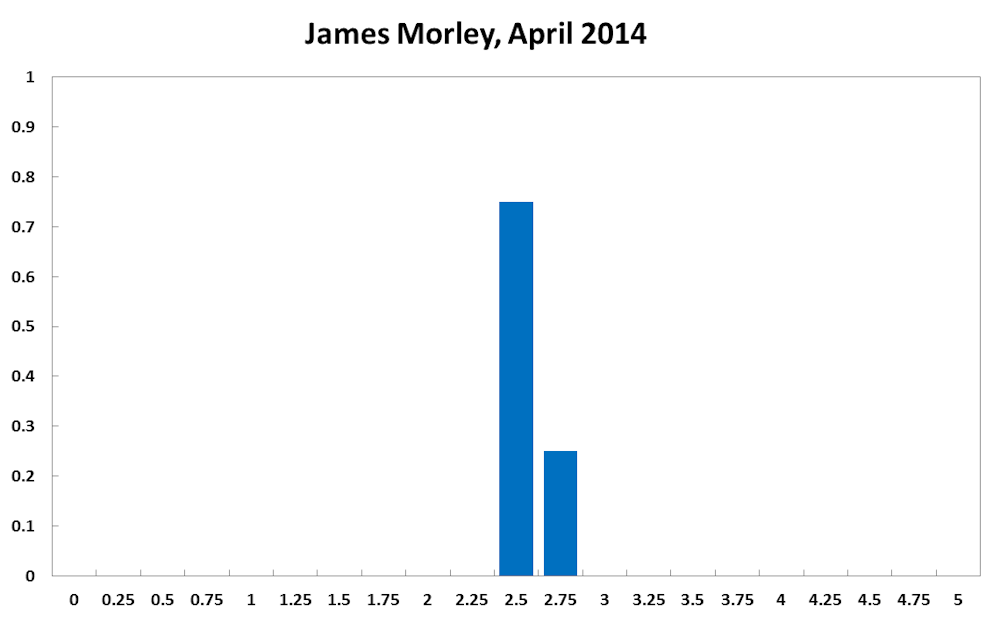

James Morley, Professor, University of New South Wales, CAMA:

Given a weak labour market and stable inflation expectations, the RBA should hold the policy rate at its current accommodative level for the time being. But the next move in the medium term should be to raise the policy rate in order to return it to a more neutral level.

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

In the last month, any positive news appears to have been balanced by the negative, so I see no reason to change my recommendations. Australia’s labour market has not improved much with unemployment constant at 6%, employment higher marginally, but hours worked down. Output growth in Australia marginally improved in 2013 Quarter 4, but this was led by a marked decline in household saving overcoming the demand effects of a decline in real investment. Globally, the advanced economies are now growing more, and while this growth will be helpful for the Australian economy, it will mean the winding down (or tapering) of quantitative easing in the US (and perhaps later in Japan and Europe), which will begin to push up interest rates in the next few years. The gradual improvement in growth in the advanced countries is counterbalanced by the possible effects of realised credit risks in China for its growth, and the danger of energy price rises from an escalation of the Ukraine crisis.