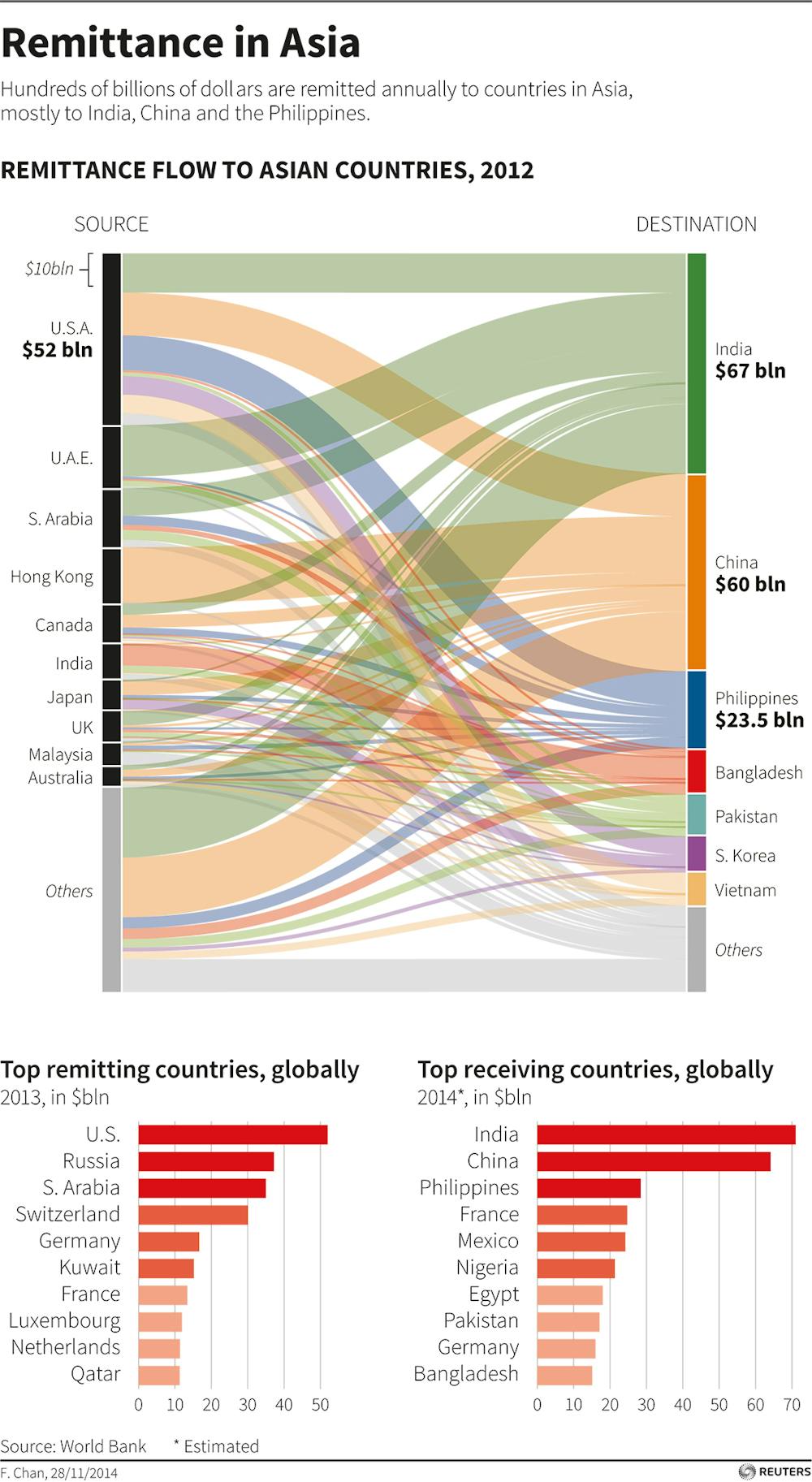

The World Bank recently forecast that remittances to developing countries will total more than US$450 billion this year, a bit bigger than Venezuela’s economy and more than double a decade a go. Given the sheer size of these money transfers, we should expect them to have significant macroeconomic effects on the countries that receive them.

And in some respects, remittances do live up to the hype. For example, research shows that remittances can reduce the volatility of the economies that receive them by stabilizing overall demand for goods and services.

They also inject significant cash into government coffers because recipients spend a large share of the transfers on imports and other taxable products. In this way, remittances have created a fiscal cushion for cash-strapped governments and even enabled some countries to avoid debt crises.

But one highly anticipated effect of remittances has failed to materialize. Although many observers hope or expect remittances to promote economic growth, research in this area consistently fails to find a strong connection between the two. Some studies find that remittances contribute to growth only weakly, while others find that they actually reduce it in the receiving countries.

Perhaps most disappointing is that despite the fact that many developing countries receive very large amounts of remittances – relative to the size of their economies – there is not a single remittances success story. In other words, there is no example of a country for which remittances have clearly driven its economic development.

Why they don’t spur growth

There are two main reasons why remittances don’t seem to automatically lead to higher long-term growth. First, there are multiple ways remittances can affect an economy. And for every path that promotes growth – such as when remittances enable children to go to school or someone to start a business – there are other, equally potent pathways that have little effect or actually lead to lower growth.

For example, in many countries, remittances are often used to purchase land or existing homes, which does not contribute to GDP. Even worse, in some cases remittances may have fueled property-market speculation, such as the recent housing bubble in Manilla, capital of the Philippines.

Another important way that remittances can reduce growth is through the moral hazard problem. People who receive remittances have an incentive to reduce their own labor, because they know that their relatives working abroad will send them money regularly.

Moreover, the worse things are at home, the more money the remitters will send, because these transfers are intended in large part to insure the family against hardship. This only strengthens the recipients’ incentives to reduce their productive efforts. Thus, remittances can lead to lower growth because recipients have an incentive to work and invest less.

Another reason why remittances aren’t strongly associated with higher growth is that they simply aren’t intended to promote it. As mentioned above, the main motivation behind remittances appears to be to provide for the family’s basic needs of food, clothing and shelter. In short, they are intended to insure families against poverty, and they are very effective at this.

Therefore, it shouldn’t be surprising that remittances are mainly spent on consumption and on acquiring shelter, rather than on education or investment projects.

Dangers of dependence

All this evidence suggests that remittances do play an important role in economies as a consumption stabilizer, and therefore also as an overall economic stabilizer. But this means that if remittances fall unexpectedly, this could lead to recession. The world saw some evidence of this after the recent financial crisis, which caused global remittances to decrease for the first time in decades.

In Africa, for example, some countries lost 0.2% to 0.5% of GDP growth because of the decline in remittances. And a few North African countries that were highly dependent on remittances from Europe lost as much as 1% in 2009. Analysis of central Asian economies showed that consumption fell faster than remittances, indicating that the latter’s decline was perceived to significantly reduce household resources.

This also places fiscal stress on governments as revenues from consumption taxes such as import duties slump. This limits their ability to plow more money into the economy to counteract the decline in remittances and resulting drop in consumer spending. Therefore, remittance-dependent economies can receive a double shock when these payments fall.

Misunderstanding remittances’ real role

Fortunately, however, these occasions have been very rare. Remittances have proven to be a dependable source of income that millions of families use to meet their basic needs. This suggests strongly that expecting them to drive long-term economic growth misunderstands the role they actually play in most remittance-receiving economies.

This isn’t to say that remittances cannot facilitate growth. But they most likely do this by stabilizing consumption and creating conditions that are conducive to economic growth.

By fostering a stable macroeconomic environment, remittances give governments fiscal space to invest more of their tax revenues in infrastructure and public institutions. It is up to policymakers to take advantage of these growth opportunities and to use the money transfers to indirectly spur economic activity.