The Reserve Bank of Australia should leave interest rates unchanged this month according to the consensus of Shadow Reserve Board members.

Amid market uncertainty over whether the RBA board may choose to cut Australia’s cash rates or maintain the current cash rate of 3.00%, some of the nine Shadow Board members see evidence for lower rates now, and in the future.

But others feel that a gradual tightening to a more neutral policy stance, following the recent period of monetary accommodation, remains the prudent path for Australia.

Retail data released by the Australian Bureau of Statistics showed spending fell 0.4% in March from February. But nevertheless it was slightly higher than expected over the March quarter.

Despite disagreement over the appropriate direction for interest rates in the future, support for holding rates this month remains strong at about 60%; the Reserve Bank of Australia should bide their time, and wait for stronger evidence.

Paul Bloxham, Chief Economist of HSBC Bank Australia said he believed lower rates could risk inflating “excessive growth” in housing prices, which have been flat in most capital cities following a brief rally earlier this year.

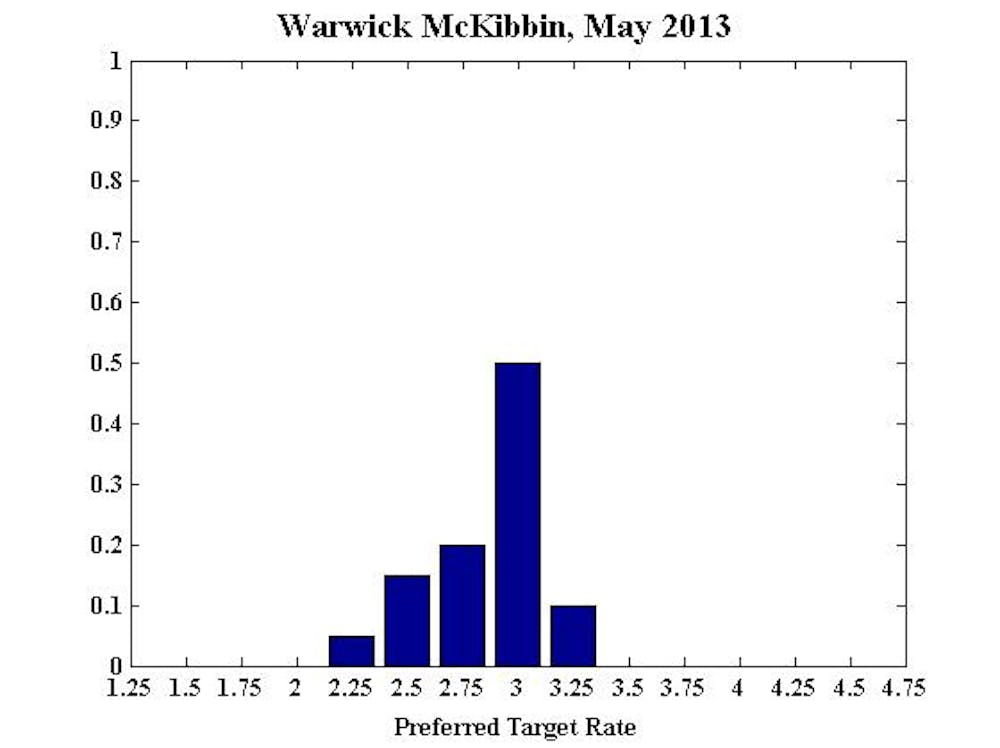

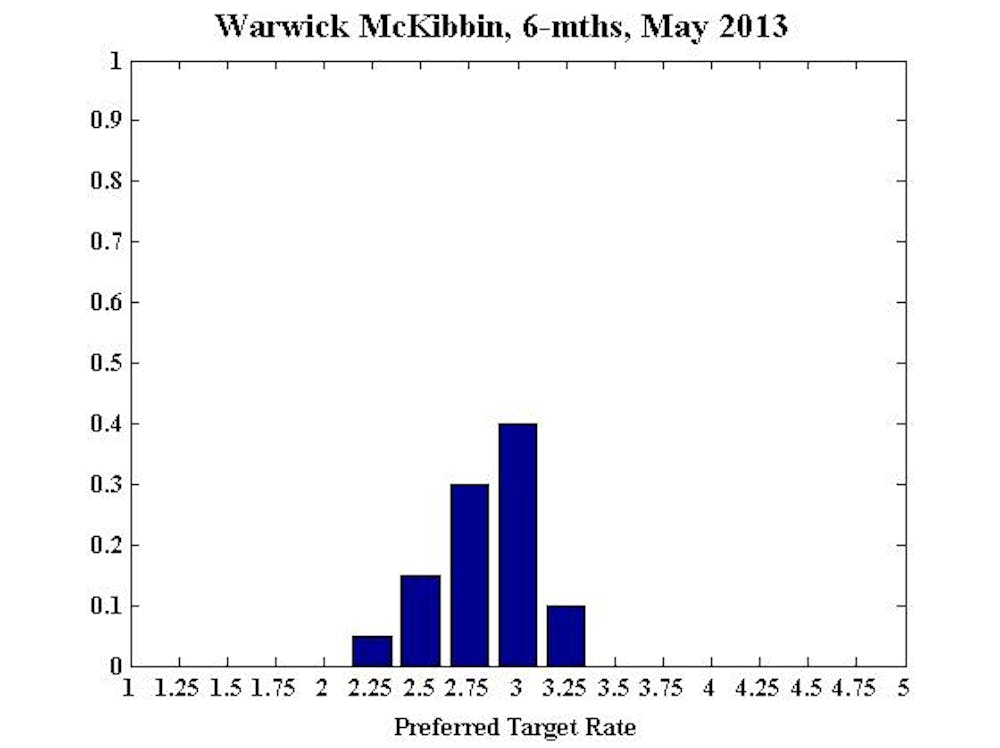

Shadow Board member Professor Warwick McKibbin has also warned Australia risks a sharp exchange rate correction leading to a rebound in inflation if foreign investors lose their appetite for the Australian dollar, currently trading at 1.03 US cents.

Professor McKibbin said a softer currency would help sectors such as manufacturing, which according to Australian Industry Group’s April Performance of Manufacturing Index (PMI) slumped to the same levels experienced in the global financial crisis.

But he said it could also “raise imported inflation and push the inflation rate well above the target band, especially given the currently high rate of non-traded goods inflation”.

The CAMA Shadow Board is comprised of influential economists from the private sector and academia. They were asked to rank their preferred settings for the cash rate.

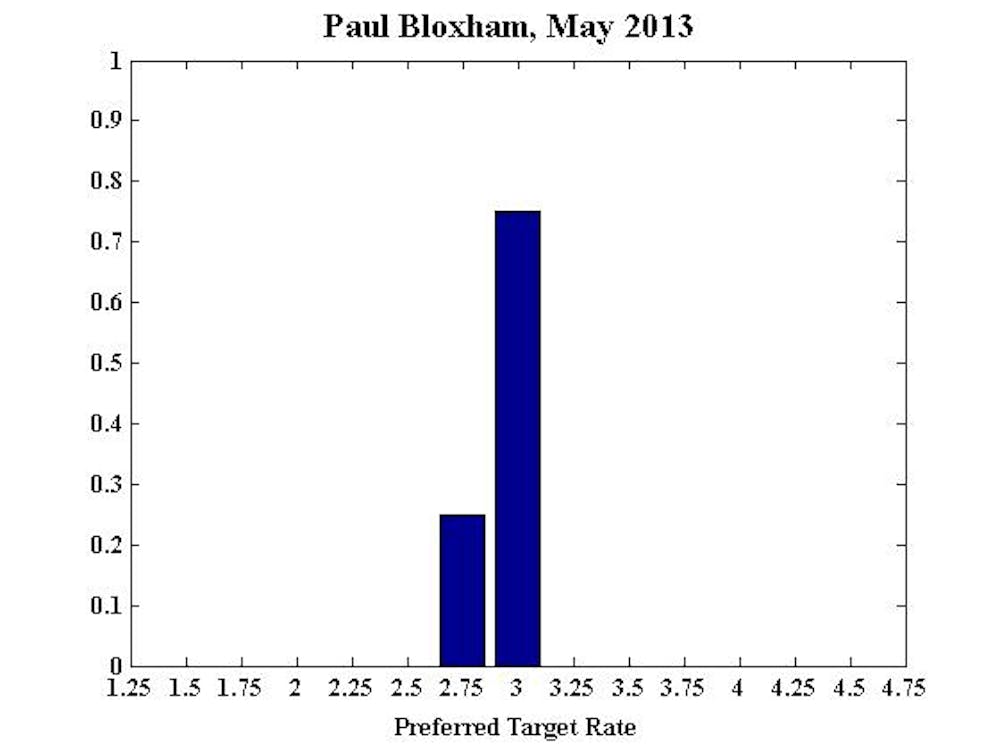

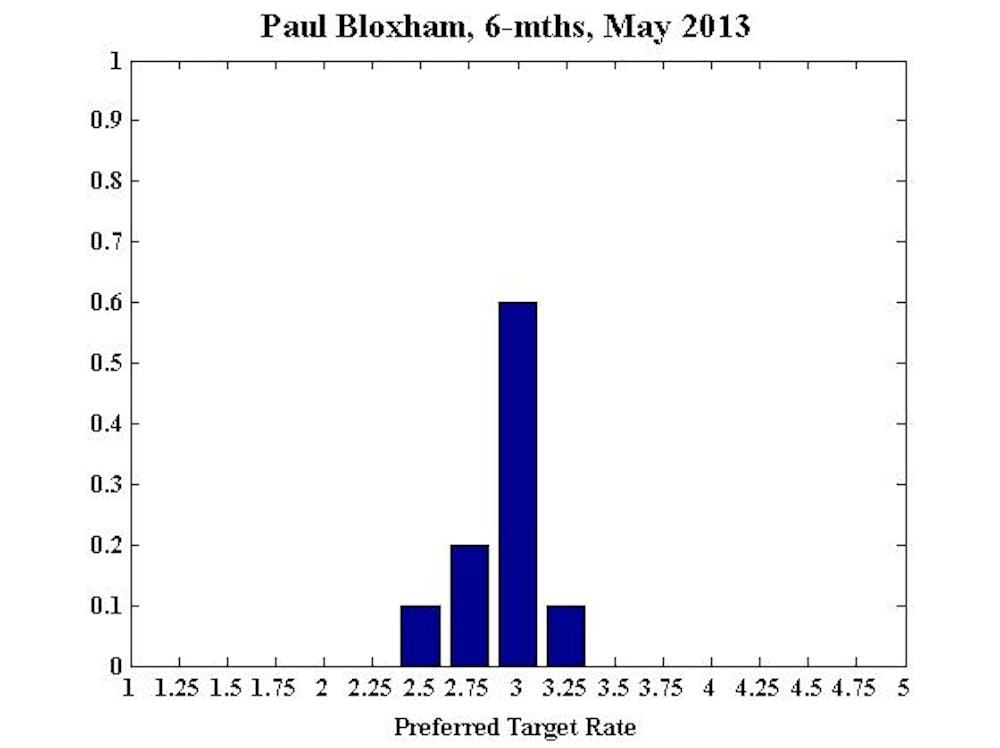

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

Inflation is low enough to allow the RBA to cut rates further if needed. But rates are already very low and there are signs that monetary policy is working. Lower rates could also risk creating other problems, such as excessive growth in housing prices. While a further cut in rates could be needed to support growth at some point, I think there are enough signs that the setting of monetary policy is getting enough traction to warrant leaving the cash rate steady this month.

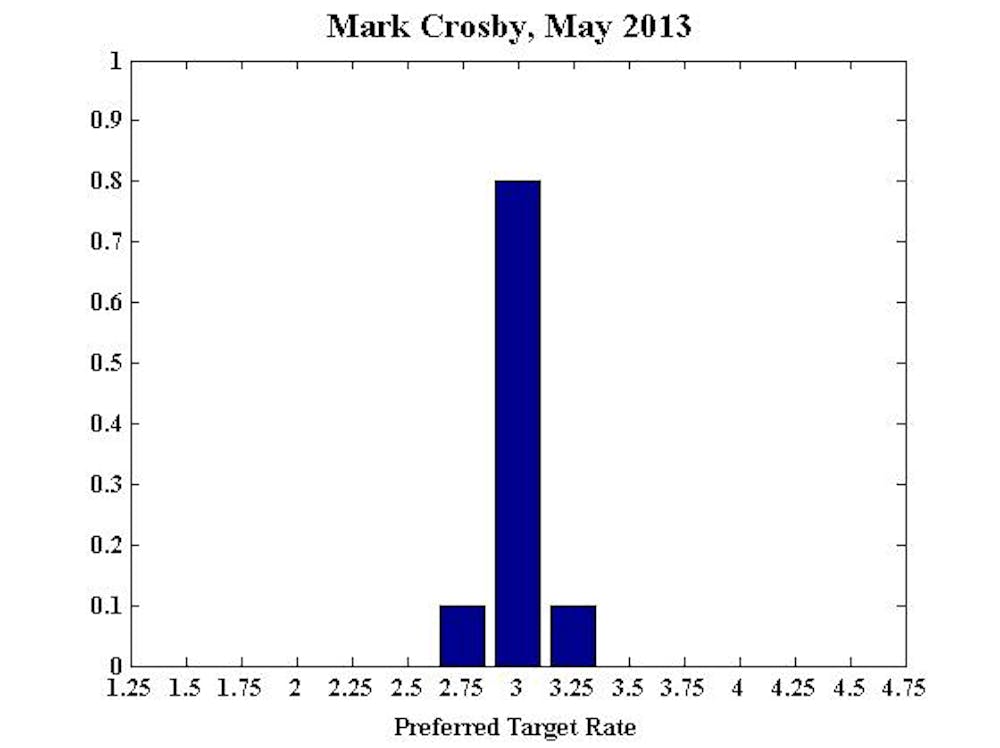

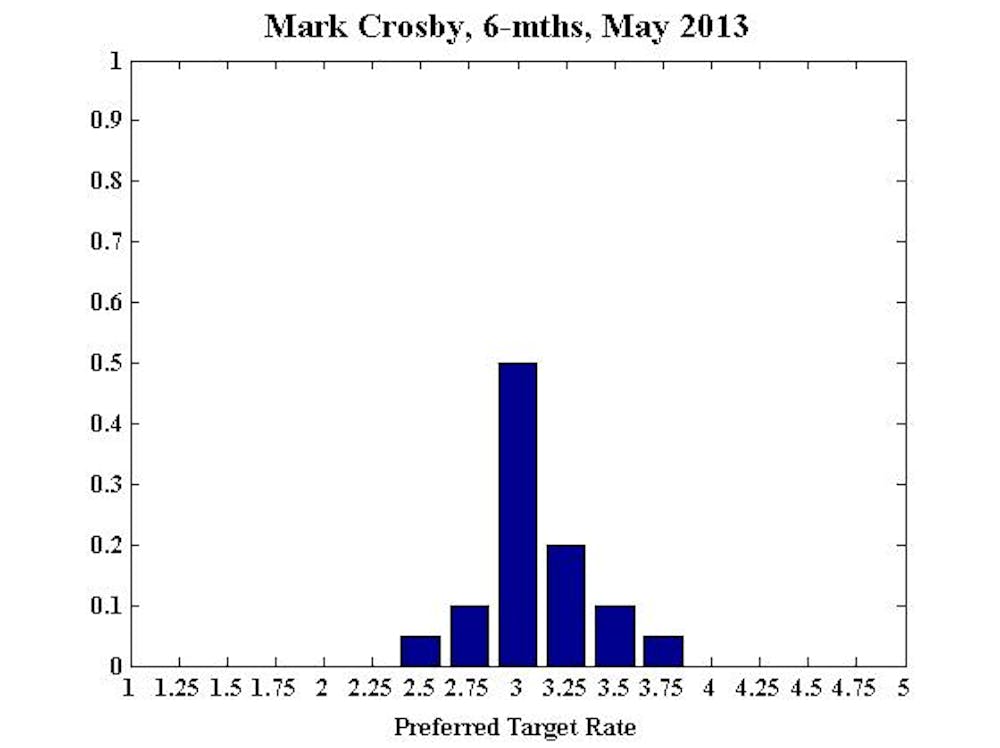

Mark Crosby, Associate Professor, Melbourne Business School:

Low inflation outcomes suggests little need for change to current settings at the May meeting. International factors currently seem stable, though unlikely that Europe will last another six months before the next country crumbles.

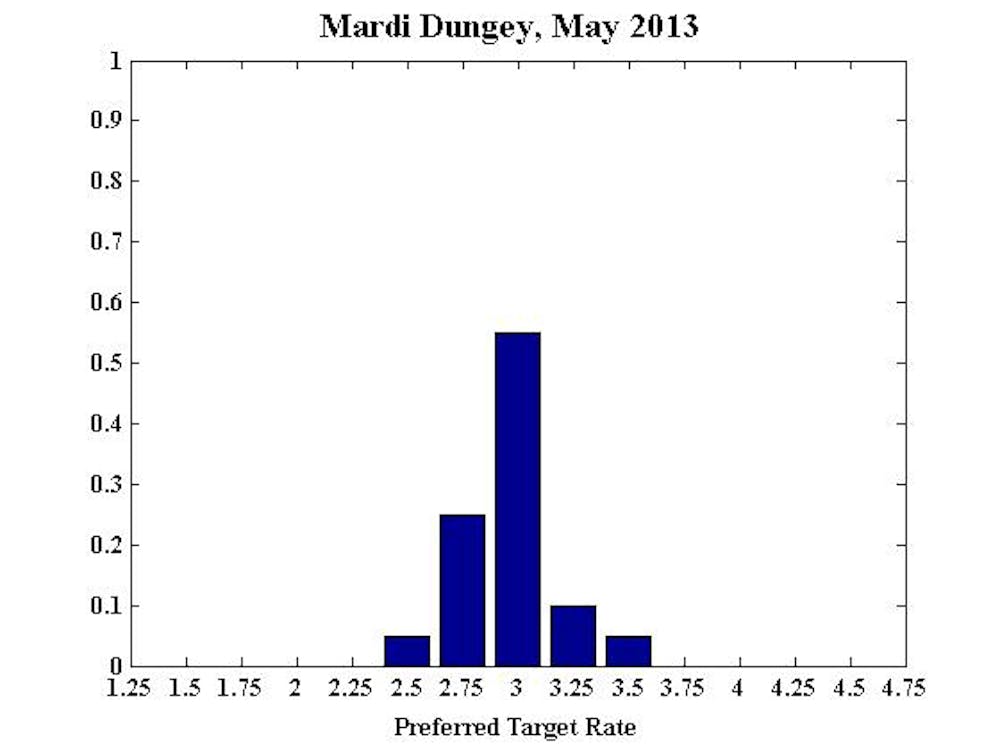

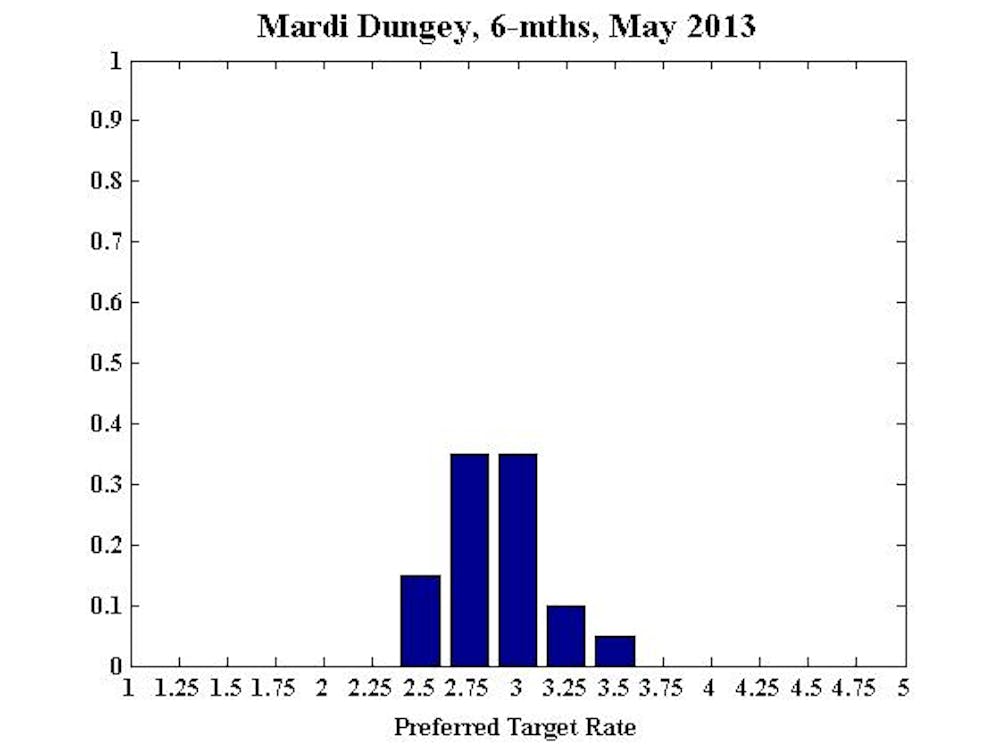

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA:

The weakening economy has caused me to lower my expectations of future inflationary pressures and hence alter my longer term projections. However, I recommend retaining the current stance in May.

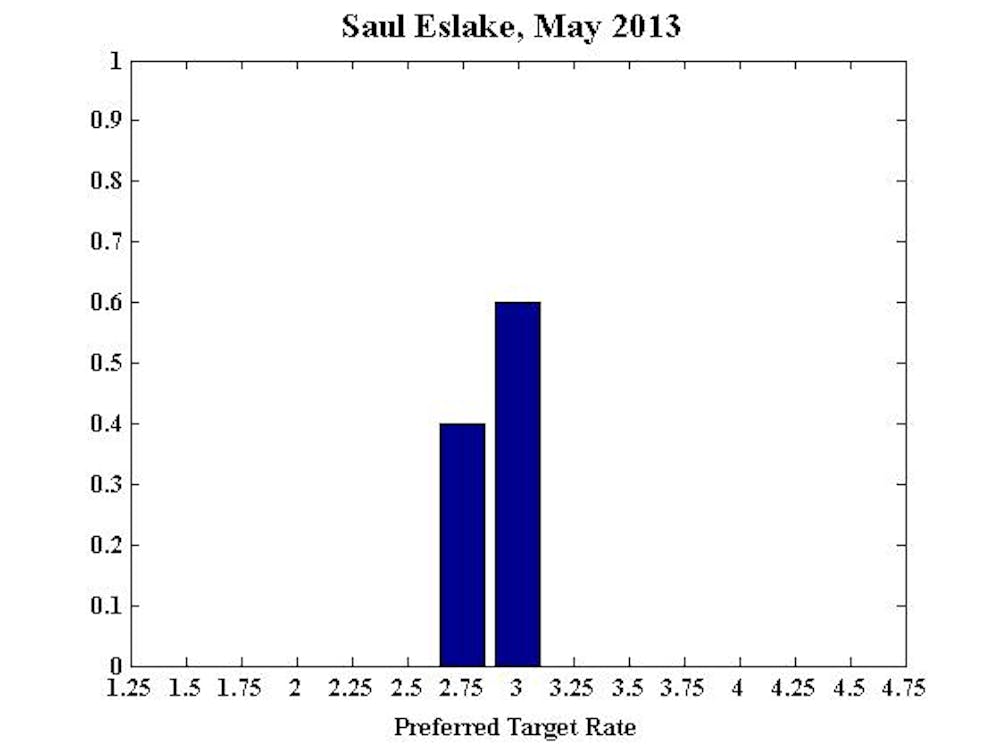

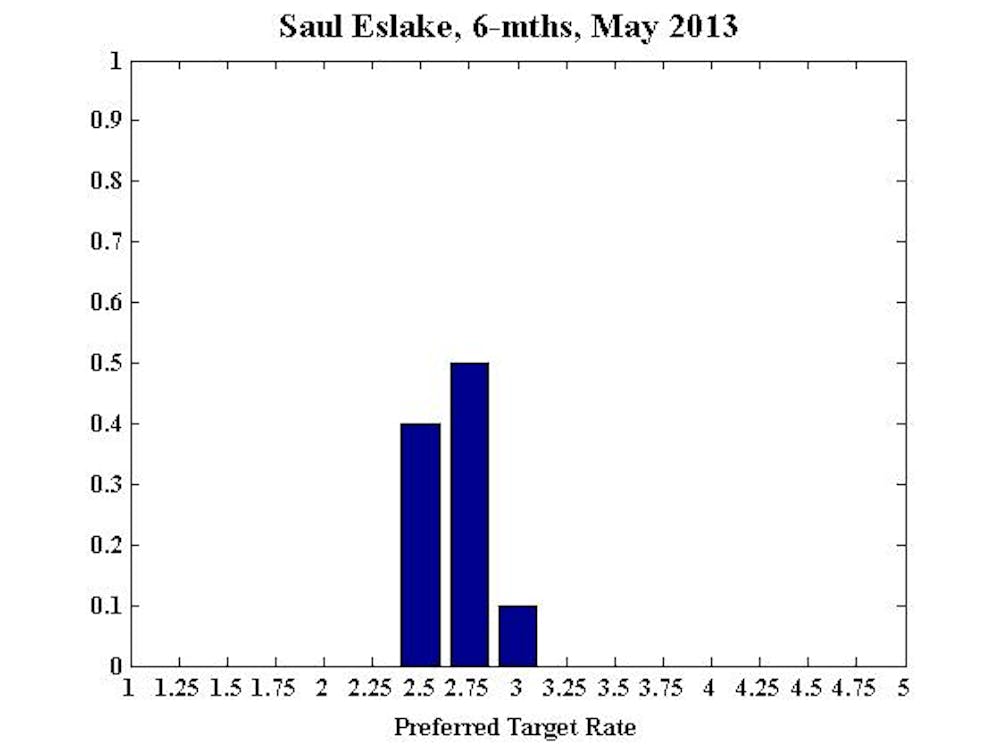

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia:

No comment.

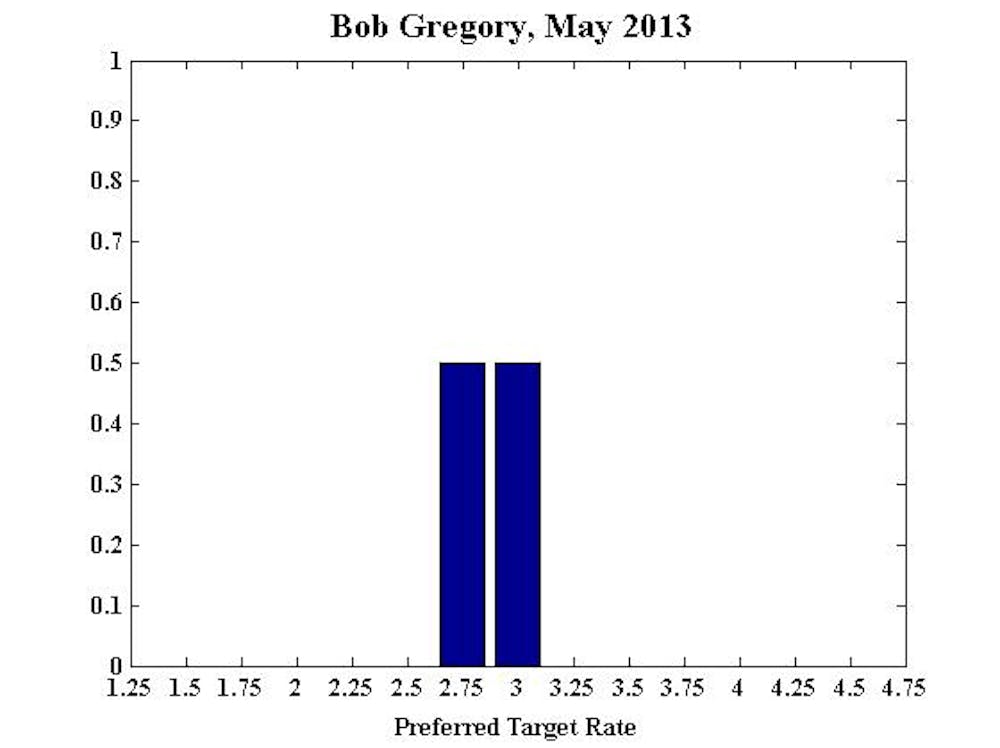

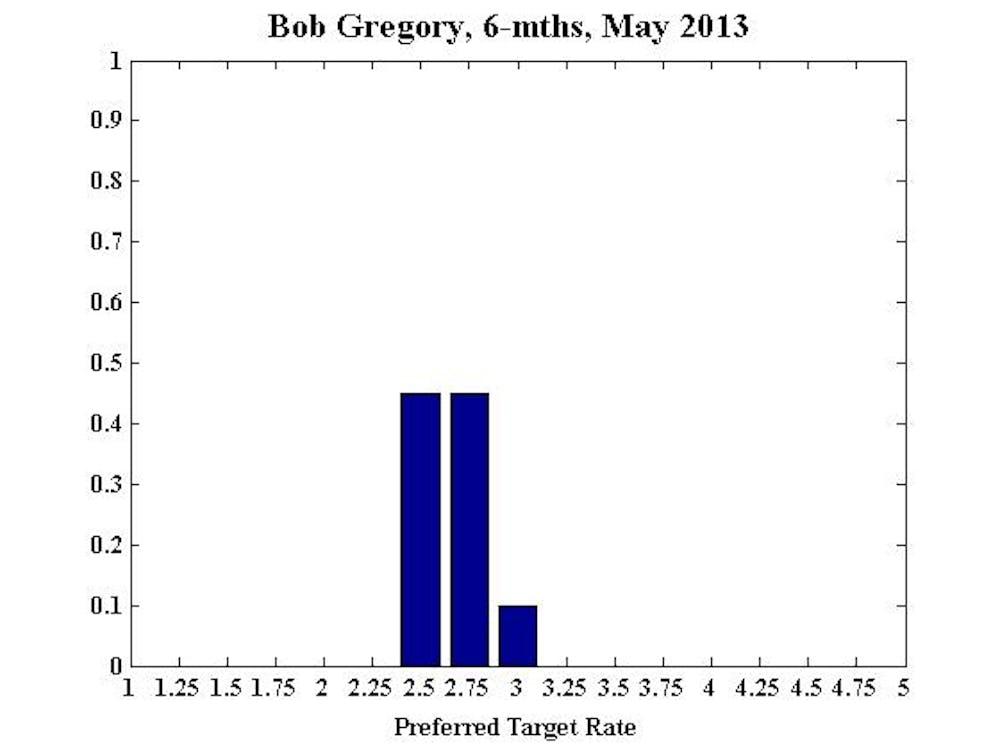

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology:

No comment.

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University:

There are clearly weak patches in the Australian economy driven by a strong currency, high input costs, the end of the first stage of the resources boom and uncertainty about government policy. These factors together with a deteriorating fiscal position suggest greater future fiscal drag on the economy as the excessive spending which has driven structural fiscal deficits will have to be cut back. The economy is particularly vulnerable to an inconvenient set of conditions, some of which were preventable. There are many uncertainties for monetary policy to balance.

Apart from attempting to accommodate fiscal negligence and the uncertainty about the nature of policies generally after the September election, in the near term the major issue is whether foreign investors will continue to want to hold $A assets and therefore keep the exchange rate a high level. A loss of foreign investor appetite will cause a sharp exchange rate correction which, while good for some sectors of the economy, would raise imported inflation and push the inflation rate well above the target band especially given the currently high rate of non-traded goods inflation.

Cutting interest rates in the face of rising inflation of goods and/or asset prices would undermine monetary credibility and risks unhinging inflationary expectations. Holding interest rates is the least bad option in this complex environment.

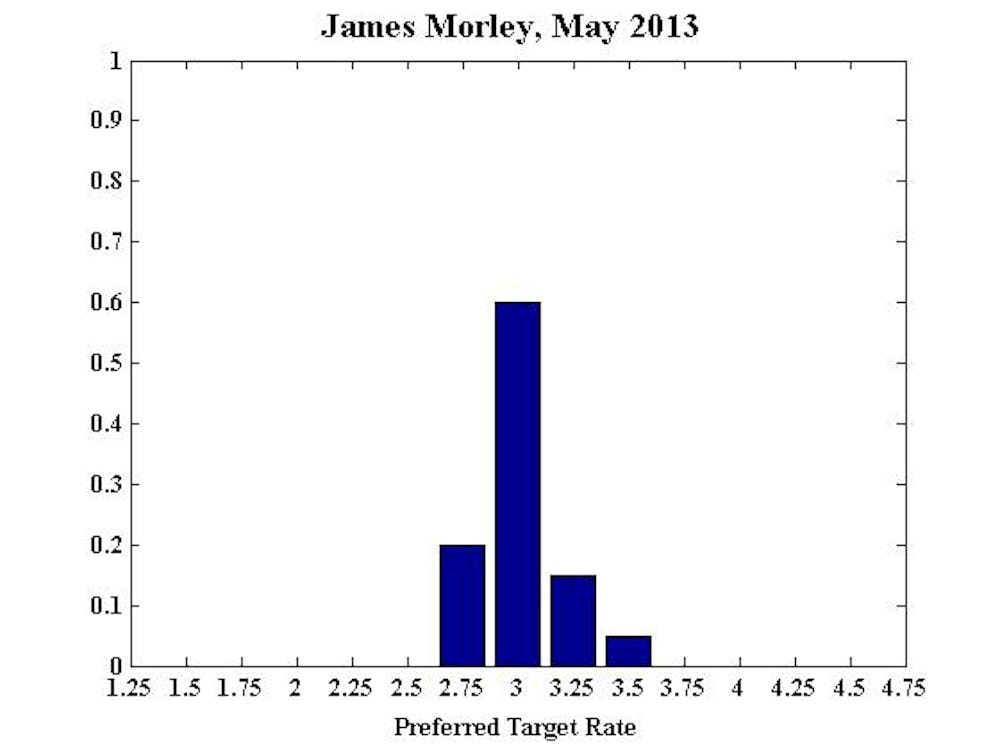

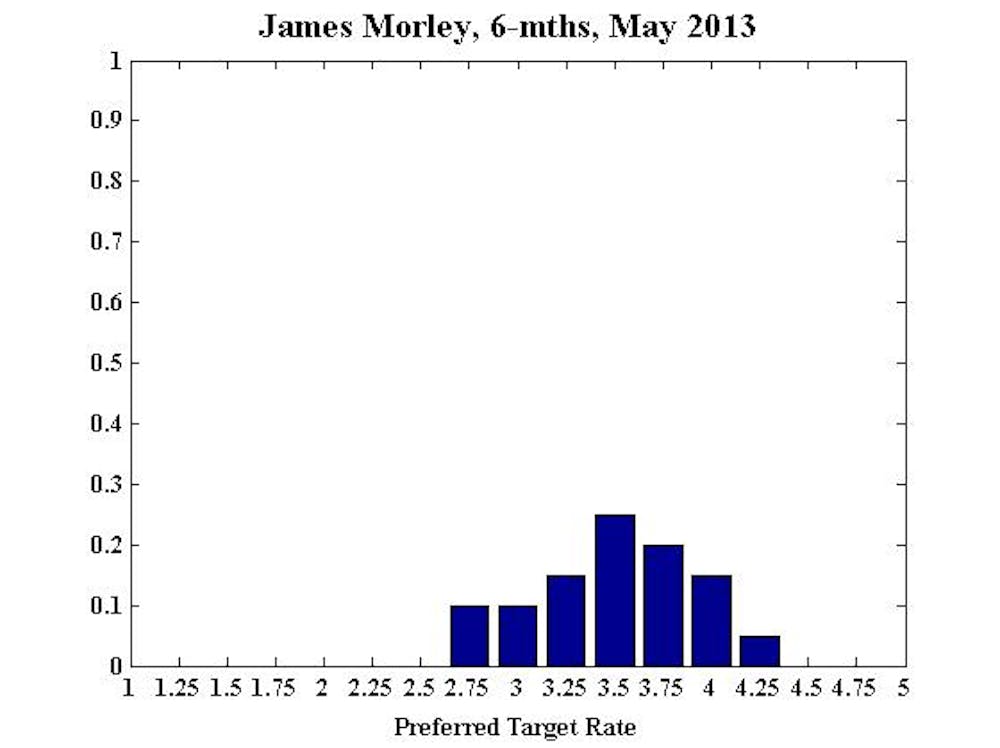

James Morley, Professor, University of New South Wales, CAMA:

Inflation is slightly higher than last quarter, but is right in the middle of its target range at 2.5% (up from 2.2% in Q4 2012). Meanwhile, the unemployment rate increased from 5.4% to 5.6% in March. The weaker labour market conditions, due to less growth in employment than new participants in the labour force, remove any immediate tightening bias in monetary policy. However, the need to gradually adjust the policy rate back to its neutral level over the medium term remains in place, although any further weakening of the labour market should delay this adjustment.

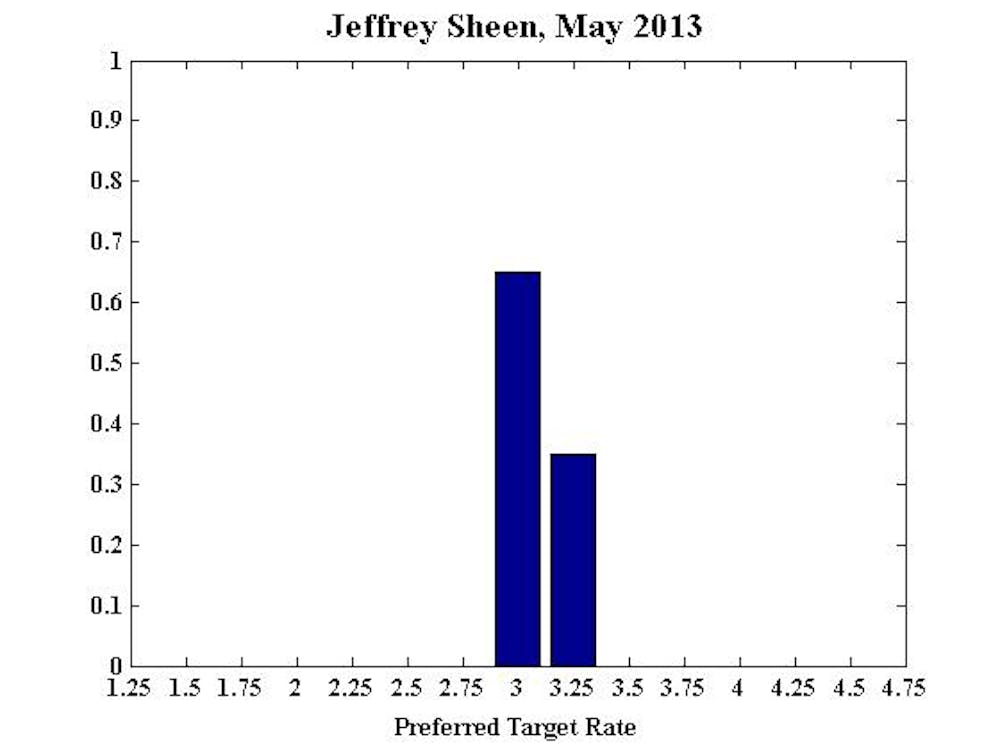

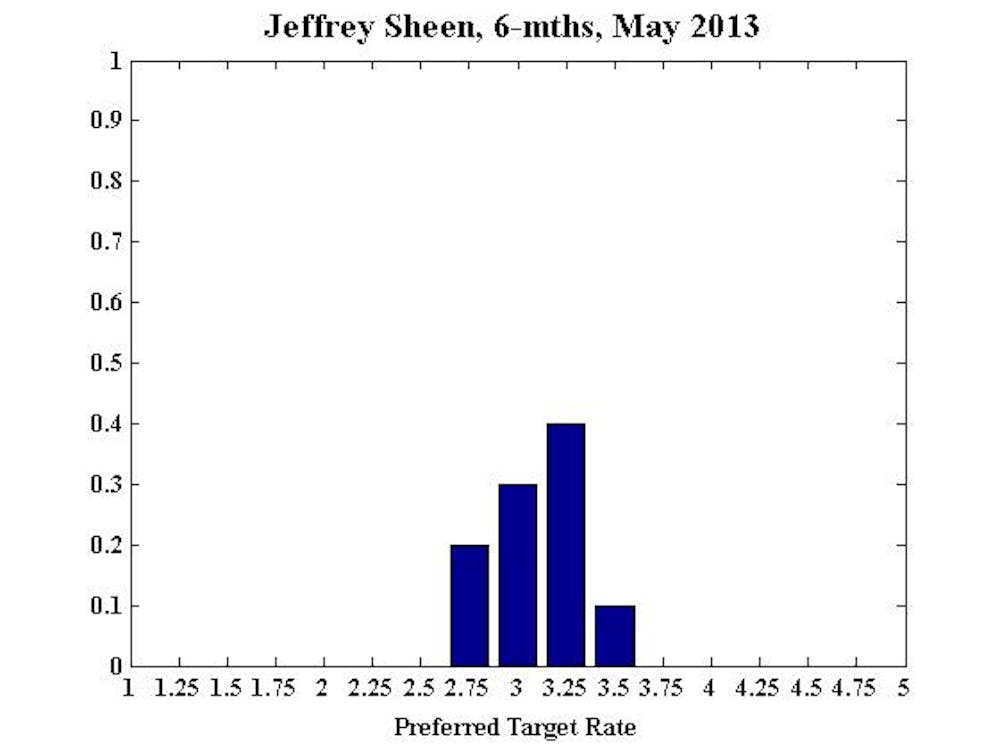

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

There were more signs in April that the long global growth slowdown will persist longer, particularly with China growing slower than many expected. This has affected commodity prices and thus consumer confidence in Australia. The small rise in unemployment to 5.6% and the fall in the participation rate to 65.1% were further signs of the continuing weak recovery here.

The Federal budget is due on May 13, and this may well have a contractionary effect if the government is determined to severely limit the expected deficit. However, given the coming election, it would be surprising if that remained true. Taking all of this into account, and noting that the real cash rate is 0.5%, monetary policy is sufficiently loose now to justify the highest probability recommendation of no change. Six months and one year out, the probabilities skew towards a slow improvement in conditions, and thus towards moderate increases in the interest rate towards its neutral value.

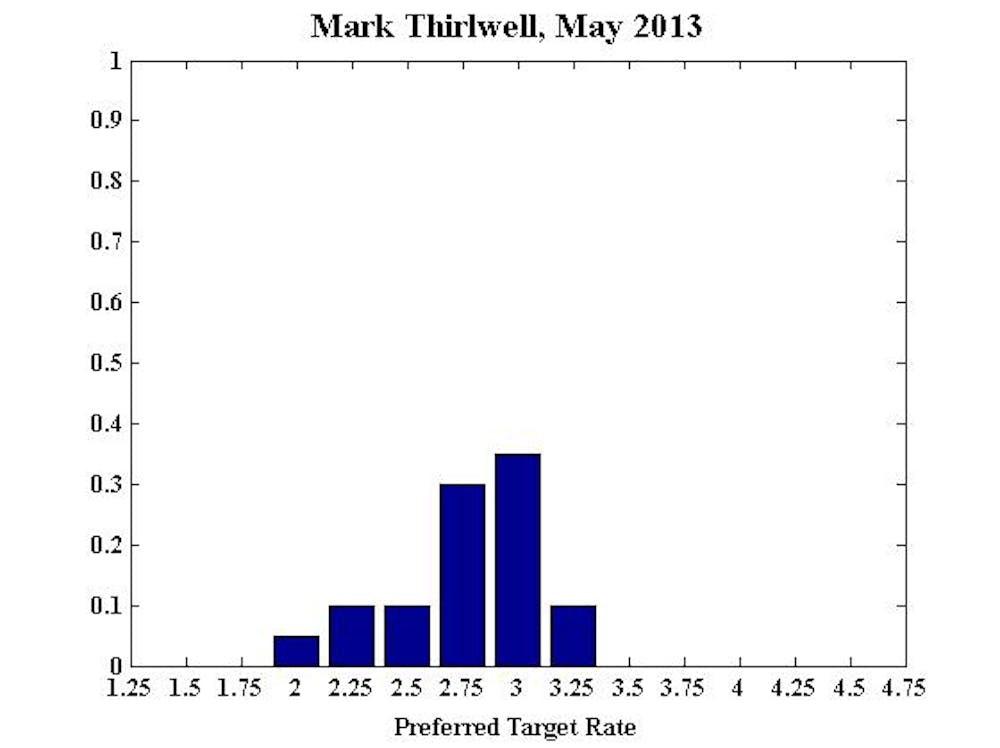

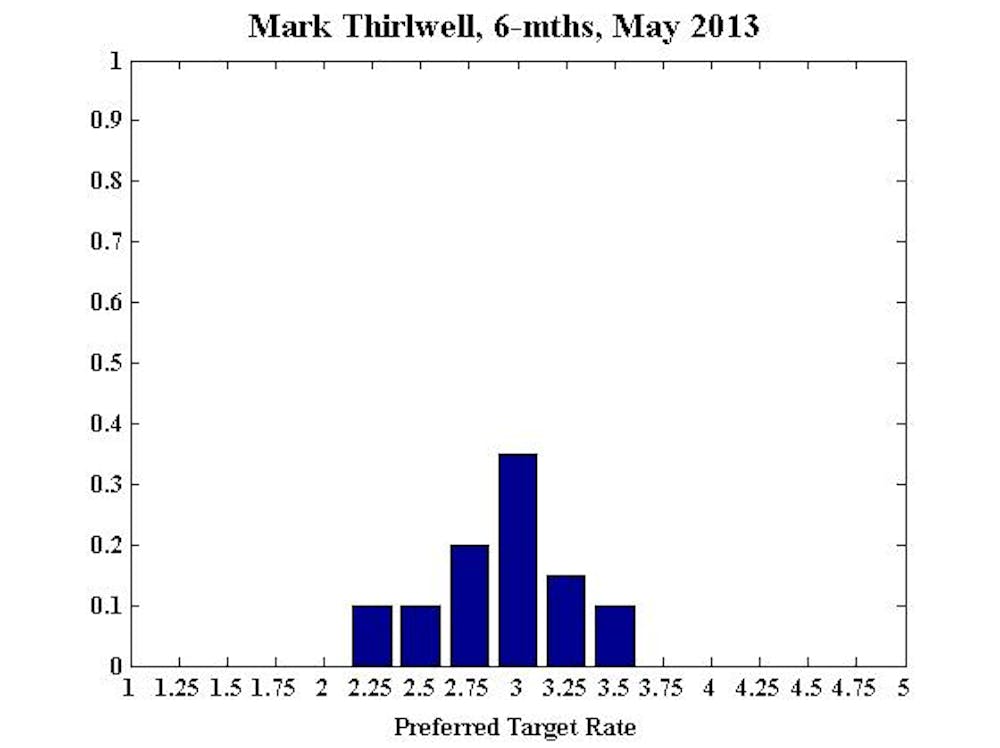

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy:

No comment.