The EU has been busy promoting its business interests abroad in an attempt to boost exports, underpin a faltering economic recovery and raise the competitiveness of European member states. Trouble is, smaller businesses face an intimidating obstacle far closer to home.

Of course, the EU is not the only horse in the race, with the US and China both banking on exports to deliver sizeable contributions to GDP growth. And Europe’s small and medium sized enterprises (SMEs) must battle not just against these direct international rivals but against a banking sector which has left them struggling to raise cash to invest and grow.

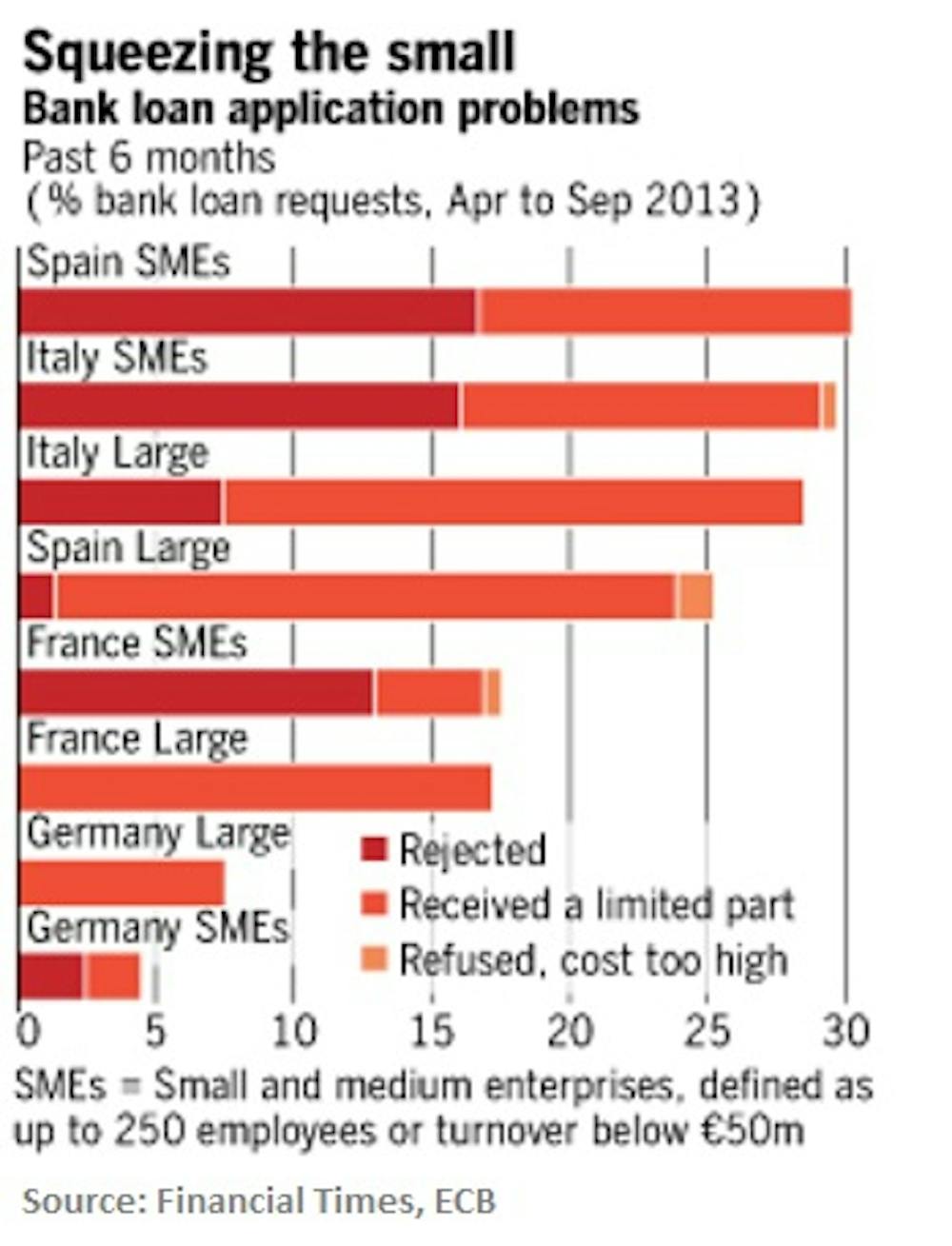

Traditionally, smaller businesses turned to banks for funding as the quickest way to gain access to the capital they needed. However, the financial crisis left banks hoarding cash to meet ever more stringent capital requirements and repair their balance sheets rather than putting the money to work in the entrepreneurial economy.

A debt deficit

The result is that firms are simply not bothering to go to the banks. According to a recent report conducted in the UK, 38% of the SMEs surveyed claimed that various aspects of the borrowing process, such as time, hassle and expenses, made them unlikely to borrow from banks. Those companies with 10 to 249 employees were more likely to feel discouraged.

At the same time, 9% reported that they had not applied for bank loans because they had assumed that the banks would reject their applications. Perhaps the most worrying aspect is that 40% of the businesses interviewed in the report declared themselves to be “permanent non-borrowers”, effectively sidelining themselves from external financing.

Of course, not all companies need external financing to grow. However, even as the cost of borrowing continues to fall, an increasing number of smaller firms have become content to leave their borrowing as it is. This might be an appealing trend in times of crisis, as companies try to reduce their dependency on finance-based solutions and preserve employment, but it becomes more worrying the longer it continues. It signals that SMEs will accept slower growth in exchange for lower funding needs. This may read as justifiable caution, but it has significant consequences for those innovative products and services that tend to be the sector’s greatest contribution to the economy.

Backbone of the economy

Such a slowdown would matter a great deal: the 87.5m SMEs in the EU account for 67% of employment and produce 58% of GDP. Lower growth in both size and numbers among smaller businesses would result in the creation of fewer new jobs and lower growth in national income. They are the backbone of Europe’s economy, and it means that if they intentionally “degrow” because of difficulties accessing capital, this will also deprive many EU countries of the consumption they need to boost their GDP. Competitiveness is likely to deteriorate as well, and a scarcity of new jobs will likely drive youth unemployment even higher.

As banks have become reluctant to lend, entrepreneurs have opened up to a more diverse range of financing options, but the outcome is still far from being significant. A report indicates that, in the UK at least, 7% of SMEs would prefer to seek financing from venture capital or private equity, while 16% of businesses would be willing to sell equity in exchange for hands-on help. The BBC television programme Dragons’ Den might make these options seem more popular, and available, than they really are.

The problem is that alternatives remain few and far between. One such option is the good old equity markets, and some Italian SMEs have started raising financing in this way. Another up-and-coming, and maybe more promising, option is peer-to-peer lending. So-called crowdfunding might still be in its infancy, but it has been growing in Germany and France, with the UK taking the lead on exploiting the this new seam of funding, according to our research. We have also seen how this enticing new alternative has led the European Commission to express a strong interest in crowdfunding, but let’s not get too excited. The diverse laws and regulations in different EU countries mean crowdfunding platforms are not yet able to create economies of scale across Europe. It may have potential, but the regulatory issues mean European smaller companies are still likely to rely on banks for external financing.

The message here is clear. Creating more funding options for smaller businesses is crucial for economic growth, but efforts to diversify sources of capital are still too tiny to carry any significant part of Europe’s economic needs. No matter how hard various European governments try to promote their countries abroad, such efforts will be wasted if SMEs are starved of the financing they need to ensure their economic survival. It is time for policy makers to modernize the legal frameworks for capital if we want to give new emerging business models a decent chance of success.