Australia exported A$94.4 billion in goods to China last year, making China by far the single most important destination for Australian merchandise.

Similarly, China is also the most important destination for Australian services exports – around $6.7 billion in 2012-2013, 12.7% of total services exported.

But a growing number of commentators have begun speculating about whether there is a significant downside to these numbers – specifically, has Australia become too dependent on China?

That’s what the Sydney Morning Herald’s international editor Peter Hartcher recently wrote: “A source of strength can also be a source of vulnerability. So it is for the China factor in Australia’s economy.” A similar thesis can be found in Ross Garnaut’s book Dog Days – Australia after the boom.

The fact that the apparent exposure is to China – as opposed to, for instance – OECD countries, only serves to heighten vulnerability concerns.

Commentators routinely express fears of an impending property market collapse in China, or a meltdown in the shadow banking system and widespread local government debt defaults.

But be reassured. The Australian economy’s growing export exposure to China should be looked upon with relief, not alarm.

Continued growth

Most countries worry about being too dependent on another country for imports, as European countries are, for instance, on Russia for natural gas. However, Australia’s chief exposure to China is with respect to exports.

In 2013, merchandise exports to China were precisely double that of merchandise imports from China, resulting in a A$47.2 billion surplus in Australia’s favour.

China might be concerned about being too dependent on imports of natural resources from Australia, but it is difficult to conceive of concerns running in the opposite direction.

And while there is talk regarding the wisdom of diversifying and “hedging our bets”, these investment allocation concepts do not translate well in the trade arena.

Australia does not get to choose where the demand for its goods and services will come from. While demand can arise unexpectedly, it is difficult to predict where this will be.

The real question is if Australia is likely to be better or worse off being exposed to China rather than another country or combination of countries.

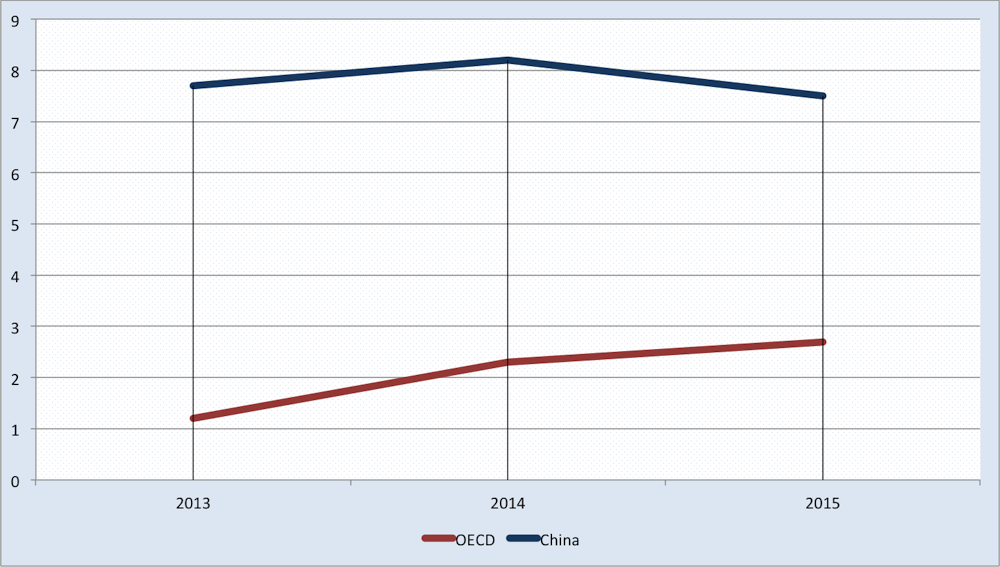

It is almost certainly the former. The benefits of Australia’s exposure to China during the global financial crisis has been well documented, and international economic institutions project China will grow at a much more rapid rate than any OECD country over the next decade at least.

And with good reason. China continues to have a low capital to labour ratio compared with countries like the US, and hence can be expected to enjoy high returns to investment into the foreseeable future.

It continues to have access to relatively easy sources of productivity gains, with ongoing urbanisation and entire industries that remain behind the international best practice frontier.

The near certainty that there will be some short run bumps along the way – perhaps more frequent than in OECD countries – or the presence of long run headwinds like demographic change, are far from sufficient to overwhelm the general case for optimism.

Focus on fundamentals

Commentators and financial markets may well get whipped into a frenzy by the release of new China data, particularly when it surprises on the downside. But these figures have almost no direct impact on aggregate demand beyond some unmeasurable impact on consumer and business confidence.

Far more instructive are the fundamental linkages between the two economies.

With respect to exports, if China were to experience a downturn, there is little evidence to suggest that its demand for Australia’s natural resources would plummet.

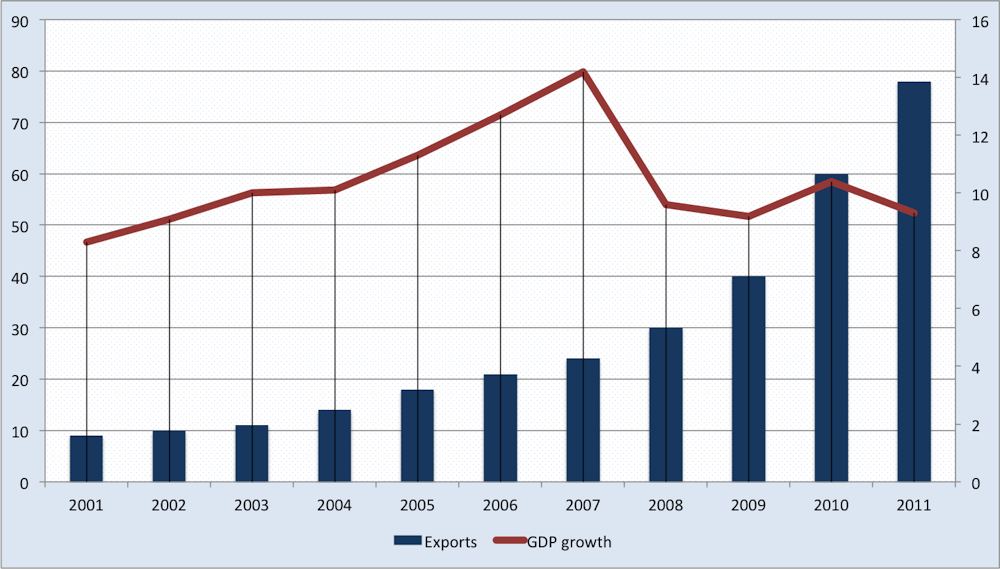

In the fourth quarter of 2007, China’s economy was growing at 13.6%. By the first quarter of 2009, this had slowed to just 6.6%. Yet the value of Australia’s merchandise exports to China over this period grew by 64%.

And this is not only a reflection of increasing export prices; volumes of key export commodities such as iron ore increased as well. Similarly, China’s demand for Australia’s services exports, such as education, has proven remarkably robust.

The Australian economy is also not without its shock absorbers in the face of a downturn in China, perhaps none more important than the exchange rate.

Between 2004 and 2012, when Chinese demand was fuelling a mining boom and the terms of trade were rising, the Australian dollar appreciated by more than 30% against the US dollar.

This appreciation had the effect of moderating the demand associated with the rising terms of trade. The income gains accruing to the mining sector were at least partially offset by income losses to other exporters, like those in manufacturing, tourism and education.

If the Chinese economy were to weaken, the exchange rate would depreciate, providing the non-mining sectors of the economy with a boost. Indeed, this process may have already begun. Since the end of 2012, the Australian dollar has depreciated by more than 10%.

Of course, exports are not the only channel through which Australia’s dependence on China might be evaluated. Another is investment. Yet here the numbers are stark: specifically, they show that the channel is almost entirely absent.

In 2012, net inward investment from China amounted to A$3.9 billion, around 4% of total net inward investment. Inbound net investment from the US, meanwhile, hit nearly A$44 billion, around 47% of the total.

At least at the macroeconomic level then, Australia’s export exposure to, and any associated dependence on, China is very much a good news story.