The people who manage pensions and investments are locked in a constant battle to win our custom, often dazzling us with examples of how well they have beaten the market in the hope that this success will continue. Careful scrutiny, however, blows that hope right out of the water.

Fund prospectuses like to show a fund has historically out-performed. This is often accompanied by a warning that “past performance is no guarantee of future success” but the reader is surely meant to draw a conclusion about its future ability to outperform. Otherwise, why include it at all?

Fortunately, it is very easy to put the question of out-performance into a scientific form. We have some data (the fund’s track record), a hypothesis (that the fund systematically outperforms the market), and methods to explore this relationship. The basic tool is to compare our hypothesis to a very basic alternative called the “null hypothesis”. In this case we can make the null hypothesis a simple assertion that in the long run the fund performs at a market average produced by random chance – hardly the stuff to stir the imagination of a potential investor.

If we can exclude the null hypothesis, then we can entertain the idea that a star fund manager consistently outwits markets. Scientists typically say that if the chance of getting a result like the data provided using the null hypothesis is greater than 5%, then the null can’t be rejected. It turns out that our hypothesis of average performance produced by random chance is enough to explain almost all track records that an investment fund could show us.

High stakes game

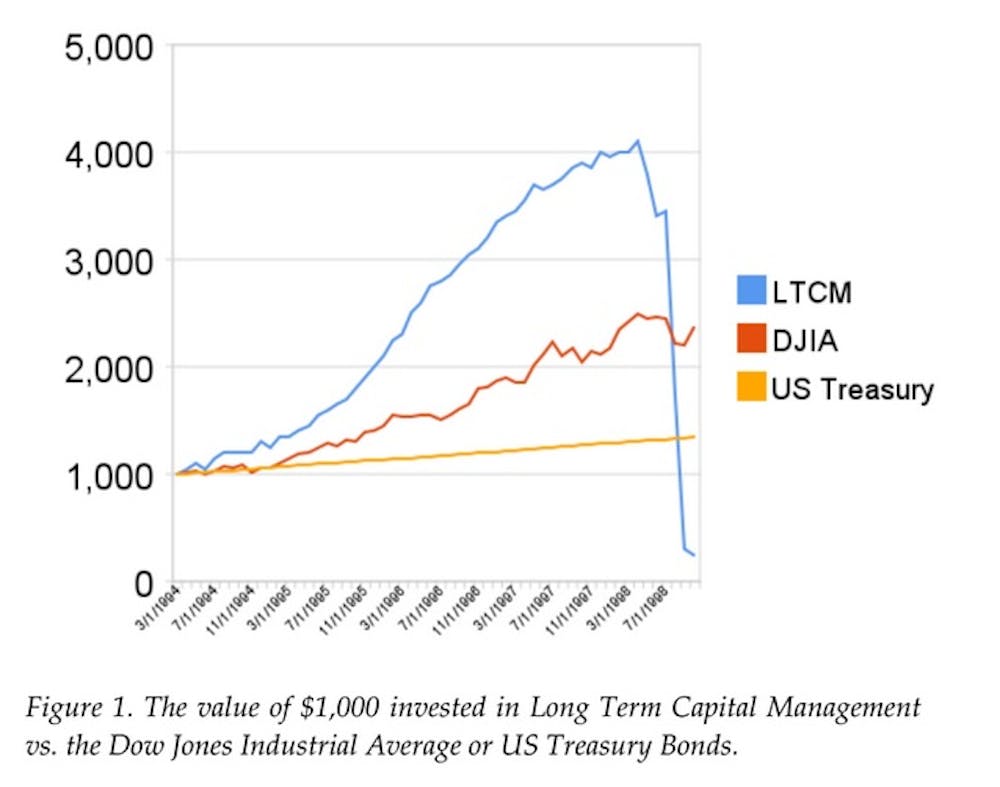

Let’s start by considering the famous case of Long Term Capital Management (LTCM). The track record was dazzling, with an annualised rate of return of over 40% for the first four years. To the financial world this seemed incredible, but there was an exciting, high-profile team, and cutting-edge computerised prediction methods to select stocks. Maybe that was enough?

Probably not. First, this was a period where the entire market was doing very well, meaning LTCM was only 13% per annum above the Dow Jones index of major companies. This is still very impressive. At its peak, LTCM was worth 1.6 times what an investment in the Dow Jones would have got you over the four-year period. Three months after the peak, the investments crashed, losing almost all their value.

{kind=link}

Surprisingly, our simple null hypothesis is enough to explain this track record. I don’t have any flair for picking stocks successfully, but there is a simple randomised strategy I can follow to allow me to run an investment fund which predictably gets a track record like this. My strategy to match this is to simply go to a casino, bet 90% of my cash on a 50-50 chance and then put the proceeds in a market index fund. At this point, I’ll either have 190% of my initial funds or 10% of them. Every four years, I take the money out of the index fund for a day and make a similar double-or-nothing bet on 90% of the money. How far would we expect this process to get before crashing? On average, I’d get one near-doubling before the crash – and this is all LTCM got.

Their curve was a lot smoother than mine would be, but I could mimic that too simply by making more trips to the casino and skewing the bets towards a greater likelihood of winning. People used to playing the lottery are less familiar with bets like this, with a small common upside and a large rare downside, but they are not uncommon. It’s the type of bet an insurance company takes with you. Mathematically, these are known as negative-skewed bets, and in the finance industry have helped encourage risk-taking by bankers and fund managers who would happily build a lucrative career in the shadow of that large, rare downside.

Even if we only showed someone the above chart up to the peak of the blue curve, before the crash, the null hypothesis could easily explain it away. Using a casino strategy and no stock-picking skill I would have a 63% chance of being able to produce a track record that grows the investment by 60% compared to an index fund over the same period. Given the 5% standard to reject the null hypothesis put forward at the beginning, we certainly can’t reject it here. Even in Warren Buffet’s famous list of nine funds with stellar track records, not one of these passes the 5% significance test.

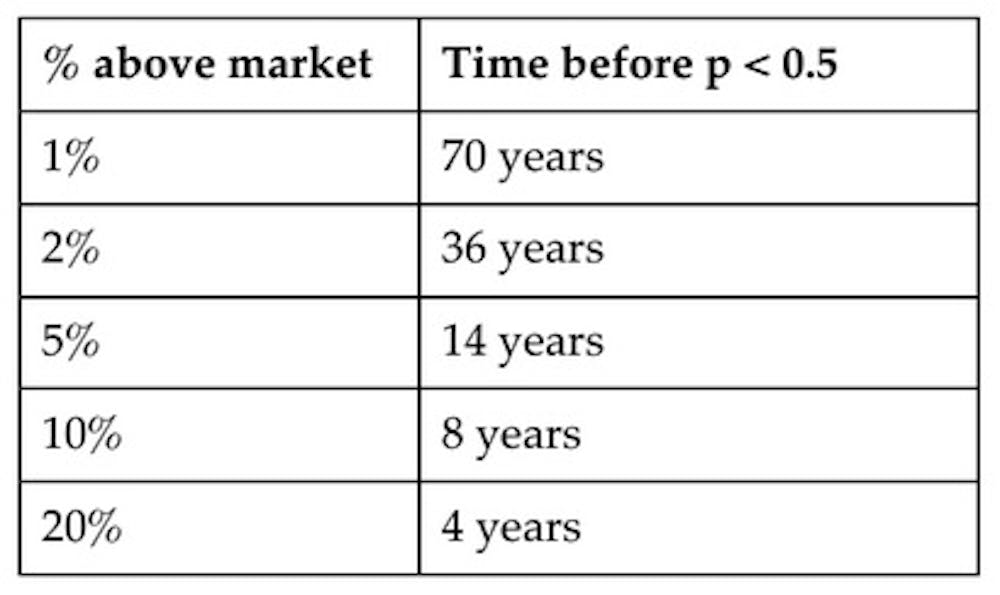

So how impressive does a fund’s track record need to be for us to start cheering those in charge and reject the idea that their performance could be replicated by a simplistic casino strategy? First consider the incredibly weak standard of achieving our market average return just less than 50% of the time (p < 0.5 in the chart).

As you can see above, some apparently very impressive performance is required before it becomes at all difficult to reproduce the track record by chance alone. Many people would be very impressed by a fund beating the market by 5% for 14 years in a row, but this is easy to achieve – so long as you are prepared to use a strategy that does very badly if the run of luck ends. LTCM was getting 13% above market rates for four years, to considerable acclaim, but would have required six years of such returns before the probability of it being achieved according to the null hypothesis dipped below 50-50. If we extend that out to achieve a probability of below 5%, as per scientific convention, then a fund would need to beat the market by 10% for 32 consecutive years – or by 1% for 302 years.

Selection effects

So, we can show that it is very rare for the track record of an investment fund to distinguish it from chance. When we also consider the impact of selection effects, it becomes almost impossible. You see, not all investment funds are brought to our attention. If a fund has done very badly, we are less likely to be told about it; it may even be shut down before it is brought to market. That leads to a “sampling bias” or “selection effect” as past performance fails to factor in the probability of those crashes, while future performance remains all too vulnerable.

We can head off to the casino again to show how this skews our view. Suppose I start 16 funds with $1,000 in each and bet the contents of each one on a fair double-or-nothing game. On average, eight will win. We can do this again with three more games and by the end, on average, one fund will win all four of its bets, taking it up to $16,000. By making opposing bets, I can even guarantee it.

We can then put it back into an index fund in the stock market, wait for a while, then show investors a fund that radically outperformed the market. If the period is ten years, that would translate to outperforming the market by 32%. This is an apparently impressive result for an unskilled stock-picker, but much less impressive if you know that 15 other funds collapsed behind the scenes.

We should allow for such effects in our null hypothesis since they are compatible with performing at the market average and are an industry norm. If we do that, then even a fund generating returns of 10% above the market for 32 years would still have an even chance that this could be achieved under the null hypothesis.

The theoretical wrangling means that it is almost impossible to reject the idea that even some of the best financial track records are simply performing at the market average we have achieved by random chance.

In finance, the market-beating effects we are seeking are so small (a few percent per year) and over such short timescales (tens of years at most) that there is never enough evidence available for us to reliably distinguish a real effect from chance. And even if we did have data for a long enough timescale of 50 years or more, then the factors behind the performance – the brokers, stocks, market conditions – have changed so much as to make any conclusions meaningless.

It is unclear that there has ever been (or ever will be) a fund whose past performance has been good evidence for its future success. It all strengthens the growing case for investing in low-cost index tracking funds, even if those costs mean you are guaranteed to perpetually underperform the market.