Companies are getting shy about going public. The number of firms choosing to list their shares on UK stock markets hit a decade-long low in 2016. So what, you might think. Well the trend for firms to stay private, outside the glare of public scrutiny, is a worry for us all.

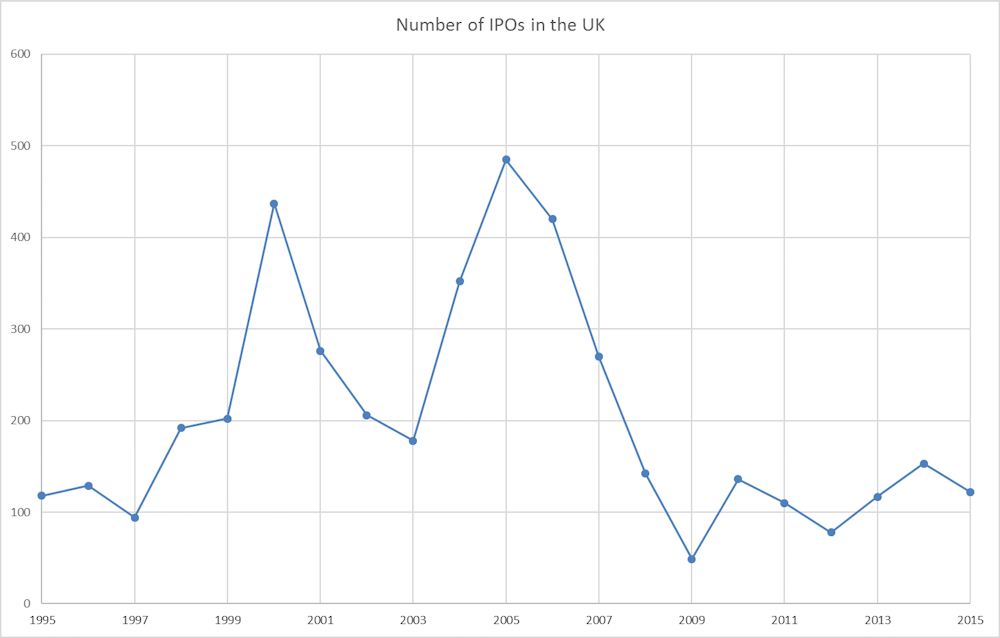

Just 97 UK firms made initial public offerings (IPOs) last year. This compares to an average of 155 a year over the last decade and a peak of 480 in 2005. These trends are consistent with the US. Over the last 18 years, American IPOs have come in at an average of 180 a year. In 2016, it was just 105. In fact, the number of publicly-listed US firms fell from 7,322 in 1996 to just 3,671 in 2017. In the UK, it has fallen to about 2,000 from close to 3,000 in 2011.

IPOs do come in waves. The recent peaks arrived with the tech boom in the early 2000s, and there was a clear and understandable slowdown in the aftermath of the financial crisis. But the latest data from the London Stock Exchange shows the trend at a time of relative confidence in markets.

Staying private essentially means that a company’s shares are not traded on public stock markets, like the FTSE in London or the Dow Jones in New York. The company still has shares, but these are held by the company founders, their families, or a select group of investors. If you want to buy shares in this firm, you have to make a request to the existing owners. The question is, why is this approach becoming so popular?

In control

First, founders and bosses get full control over senior executive pay. Because a small group of existing shareholders dictate who buys the shares, it makes it far less likely that activist shareholders will reject controversial pay awards.

Staying private also avoids the onerous disclosure requirements from stock exchanges. Some companies fear that a small failing in due diligence could lead to troublesome interest from regulators, or even expulsion from a stock exchange.

The costs can be significant too. A firm listing on London’s AIM stock exchange for small companies will have to pay in the region of £350,000-£400,000, with a further 6% of any funds raised being paid to brokers.

Horizons

Shareholders who buy stocks on the public markets may be in it for a quick buck. That can mean publicly-listed companies get railroaded into strategies that deliver short-term gains so investors can sell up and book a profit.

Private investors, by contrast, will tend to have a more long-term view, and can wait for a number of potential risky innovations or strategies to bear fruit. Some long-term private equity funds have a standard investment timeframe of as much as a decade, meaning they can sit tight waiting for investments in research and development to pay off – family-owned firms have a similar advantage.

Now, all of these disincentives for public listing can be swept away by the incredible fundraising power of public markets. It used to be the only reliable way to raise large amounts of capital. And prior to the Jumpstart Our Business Startups (JOBS) Act of 2012, firms in the US had to go public if they had more than 500 shareholders. This is the ruling that forced Facebook to go public in search of more capital. Now that firms can have up to 2000 shareholders, fewer firms need to go to the public markets.

And at the same time, crucially, private markets have evolved to provide sufficient wealth for many firms to remain outside the stock market. Poor returns from bank deposits have sent more large investors in search of higher returns, often to those private equity funds.

Simply put, if the money is available through private markets, then the appeal of public markets is limited. In fact, public markets can hold you back. The time taken to seek shareholder approval for major strategy changes can slow down a business. Uber founder Travis Kalanick was able to take his privately-held firm through several changes of direction before settling on a virtual ride-sharing service.

It starts to sound like an easy decision to stay private. The trouble is, the shrinking of the public market brings unwelcome effects.

Public goods

The stock exchange has long been a redistributive mechanism of wealth. The general public can buy into new firms and share in their success through dividend payments and shares. Anyone with a company pension scheme gains access to corporate success. Without a healthy market in IPOs, the market gets smaller, capital becomes more tightly held, and in theory, inequality gets worse.

Going public can also be a stimulus to recruit top talent. A company preparing for IPO is advised to bring in the best CEO and chief financial officer one to two years before so they can build relationships and galvanise staff. And an IPO can be a reward for those patient staff and investors whose hard work and loyalty can now be rewarded with shares.

Companies can also derive a moral benefit from the transparency of public markets. This is particularly true of growing global stars, like Uber and AirBnB, that are changing employment and social practices. A broad base of public ownership is more democratic than ownership by wealthy and invisible individuals, and opens up boardrooms to the views of more of society.

In truth, the argument that secrecy looks bad, and that more voices should be heard, is unlikely to tempt today’s more retiring plutocrats to go public. Many of these individuals value the privacy and flexibility of private ownership, and are nervous of entering into the costs and publicity of a public market. They will happily ignore the strongest argument of all that companies should share their wealth in what is becoming an increasingly unequal society.