I was trained as an economist, but that does not mean I think economics determines absolutely everything. However on occasion the impact of economic factors proves so strong that the causality is obvious. So it is with the results of the elections to the European Parliament, when far-right parties achieved phenomenal success.

Some commentators report that centrist parties maintain a parliamentary majority in Strasbourg. But this view of the elections makes Pollyanna seem a pessimist. So how did the nightmare of a resurgent authoritarian right in Europe come to pass?

In 1950 Robert Schuman, the French foreign minister, proposed a co-operative and mutually supportive association of European countries which no one country could dominate. Then, 20 years later, Willi Brandt would propose a common currency to complement the common economic framework (the Werner Plan). The creation of the euro is about as clear an example of “be careful of what you want because you might get it” as you will ever find.

As I explain in some detail in Economics of the 1%, the economic policies fostered by the European Commission, with the support of the German government and the Bundesbank, were (and continue to be) a disaster for the countries of the EU – with the exception of Germany itself.

This of course runs counter to the dominant media narrative, perfectly summed up by Claire Jones of the Financial Times who recently told us: “Recovery spreads across eurozone.” This claim is worth examining.

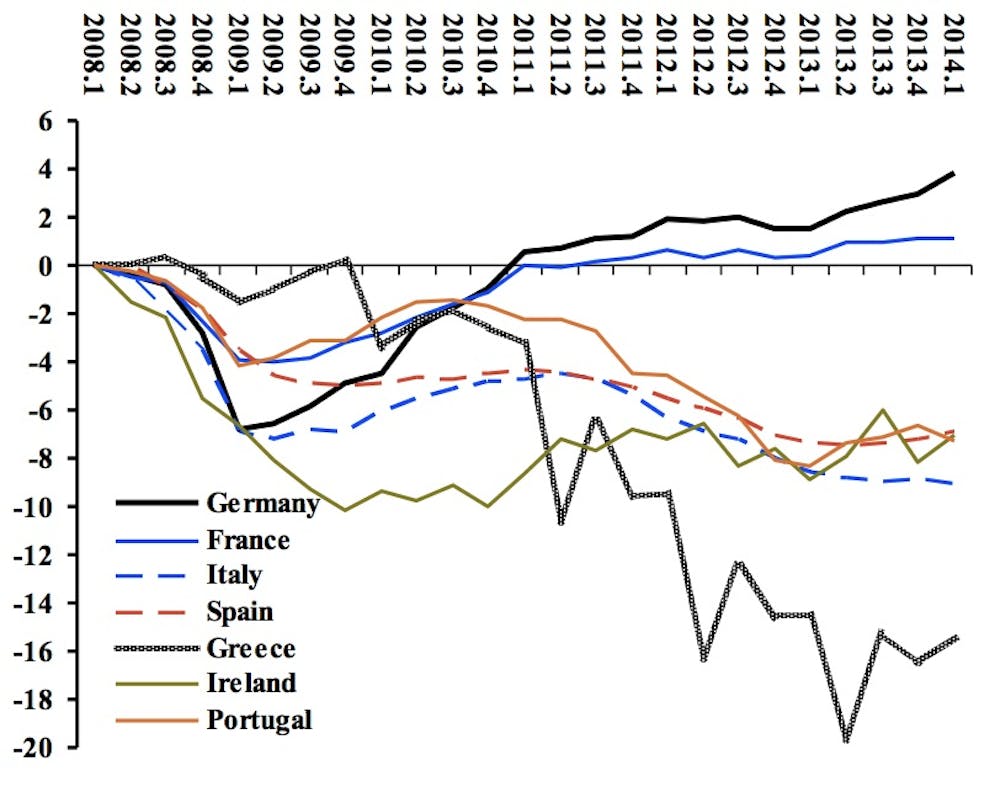

The chart below shows GDP at constant prices for seven eurozone countries, Germany, France and the five so-called PIIGS (Portugal, Ireland, Italy, Greece and Spain). As in my previous article, on the unimpressive UK recovery, I set each country’s GDP to zero for the second quarter of 2008 (the pre-recession peak for all but one of the countries). The value for every subsequent quarter is the percentage point difference compared to that peak quarter.

GDP measured as percentage difference from mid-2008

The first and most obvious message from the chart is that the national income of five of the seven countries is at least 5% below mid-2008, and more than 15% below for Greece.

Look closer at the chart and you see that in three of the countries, Italy, Portugal and Spain, national income began to recover in 2011, then suffered a reversal. And the chart reveals the much-praised Irish recovery as a very modest improvement during 2010-2012, followed by stagnation at around 6% below 2008. Then we have France, which recovered to the 2008 level in mid-2011, followed by near-stagnation.

And what about Germany, whizzing along to 4% above 2008? As I and many others have argued and documented, the German recovery represents the success of a mercantilist beggar-thy-neighbour policy.

At the end of the 1990s, Germany’s Social Democratic government and its mainstream trade unions reached a pact to freeze real wages. As a result, the country’s exporters – almost all larger corporations – cut export prices. Subsequent changes in VAT rules cut taxes on the part of production that companies exported, further enhancing German “competitiveness”. If mercantilism is your thing, then give German “competitiveness” a round of applause.

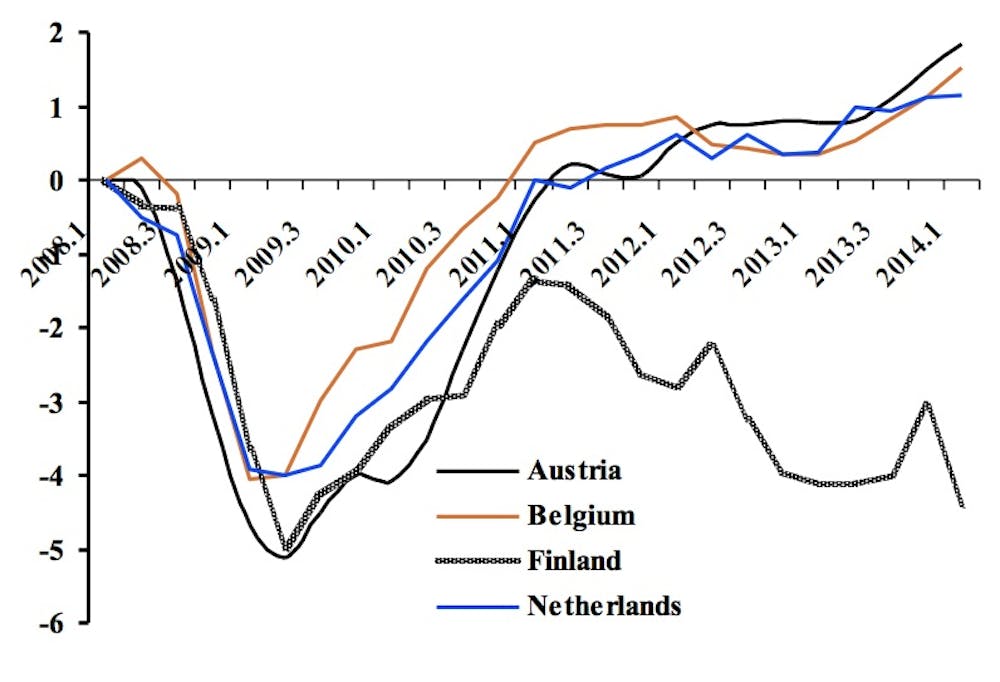

The second chart shows four northern European countries and how they fared – not very well for Finland, to say the least. As for the others, what passes for recovery is national income between one and two percentage points above 2008.

GDP measured as percentage difference from mid-2008

Looking over these numbers, we find six of 11 countries at least 5% below their pre-recession peak after six years and three with less than 2% improvement. Meanwhile, the largest and most influential member of the eurozone enjoys the greatest and most robust improvement in national income, along with a trade surplus second only to that of China – and in some years larger.

So it should come as no surprise that EU voters delivered an electoral shock in country after country. The message sent by a startlingly large proportion of voters is: “if this is recovery, we want none of it”. A sustained and strong eurozone recovery requires abandoning the austerity policies that burden every government except Germany.

To put the same point another way, a true recovery in the eurozone requires a change by German policy makers, especially in the Bundesbank. Until that occurs stagnation will be the fate of almost all the other euro countries.