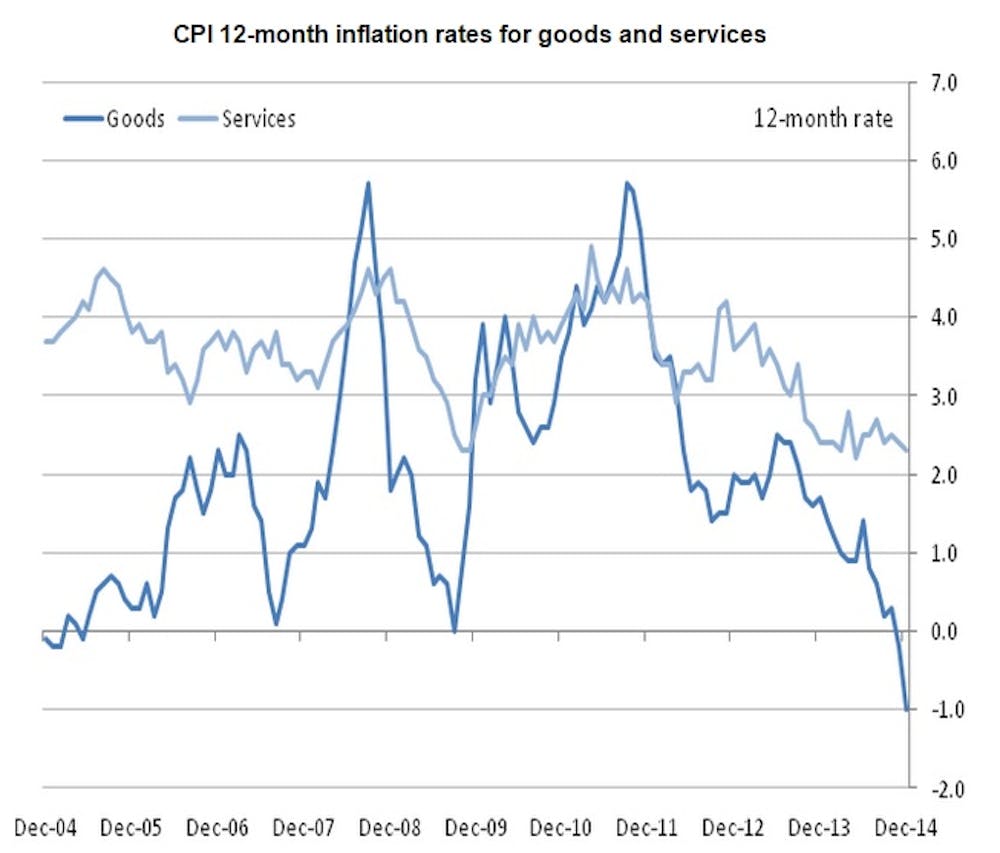

UK inflation is low. It is well below the government’s 2% target and is expected to stay that way for at least the next 18 months. On Tuesday, the Office for National Statistics reported it had dipped to just 0.5% – the joint lowest since records began. It marks a rapid change in the UK economy and it may offer chancellor George Osborne and the Conservative party a useful electoral tool.

Until late 2013, inflation had been well above the target, reaching nearly 5% in 2011. At first sight, this is surprising. If inflation was well above the target when the economy was suffering from the near-collapse of the financial system in 2008, how can it be so low in 2014 when the economy is expanding rapidly, at close to 3% a year? The answer partly reflects developments in the global economy, but also reflects an interesting and possibly fundamental change in the UK labour market over the past decade.

Oiling the wheels

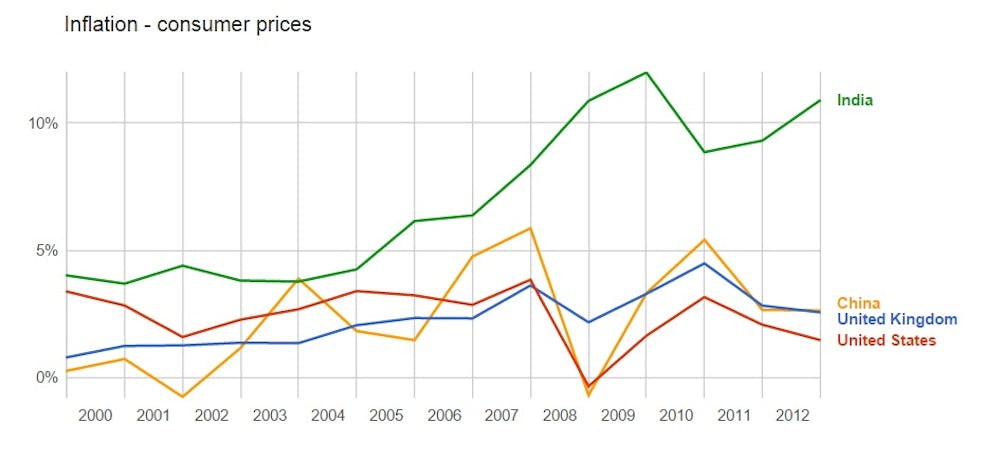

Part of UK inflation is imported. Inflation is close to zero in the eurozone, less than 2% in the US and slightly higher than 2% across the G20 (which includes higher inflation economies such as China and India). The price of oil is low and falling. Much of this reflects the depressed prospects for the global economy.

We might have expected these downward pressures on UK inflation to be offset by upward pressure from the recovering UK economy. There is a sustained rebound in output, employment is rising rapidly and all measures of unemployment have been heading down for some time now. In previous recoveries, this situation would be associated with inflation of around 4-5%.

So why is inflation so low at the moment? A key indicator of domestic inflation is the growth rate of unit labour cost – the ratio of wages to productivity. This has fallen over the past year, matching the reduction in inflation. Rapid productivity growth reduces unit labour cost growth and so is a potential explanation of low inflation. But this explanation does not fit the facts since productivity is below 2007 levels and productivity growth remains worryingly low.

Pay restraint

The best explanation for low inflation is a very low rate of growth for wages. Low wage growth has been a feature of the UK economy for the past five years; real wages for the average worker have fallen by around 6.5% since 2007.

There is no single good explanation for why this should have happened. Some point to a highly flexible labour market in which workers may have preferred static wages to job cuts. But that effect should have unwound when employment began to recover.

Others point to a high rate of immigration, especially from Europe. But that would suggest a larger squeeze in cities like London where new immigrants are concentrated; this has not happened.

Others point to a change in the composition in employment, with most new jobs being low paid. But that doesn’t explain why existing workers have suffered falling real wages.

This leaves others to point to a shift in the balance of power in the workplace, with managers being able to suppress the pay of most workers.

At this point, we do not know which, if any, of these factors is the real driver of low wage growth. Until we do, we cannot be confident that this trend will be reversed any time soon. This is becoming an important policy issue; even the CBI recently encouraged its member firms to be generous in their wage offers. More widely, low wage growth has led to much lower than expected revenue from income tax wages.

Until the economic recovery is reflected in increased wages, there is little prospect of the UK fiscal deficit being reduced. Ironically, and perhaps usefully in an election year, Osborne might do well to enact policy measures that serve to increase the wages of workers.