Today Treasurer Jim Chalmers released a consultation paper on “Legislating the Purpose of Superannuation”.

This is a long-awaited piece of work that has been the subject of ongoing discussion since it was recommended by the Rudd government’s Financial System Inquiry in 2014.

A subsequent bill introduced by the Morrison government failed to obtain agreement and lapsed in 2019.

The 2020 Retirement Income Review, of which I was a panel member, also agreed an objective was required to “anchor the direction of policy settings, help ensure the purpose of the system is understood, and provide a framework for assessing the performance of the system”.

{kind=link}

In the consultation paper, Treasurer Chalmers proposes that:

The purpose of superannuation is to preserve savings to deliver income for a dignified retirement, alongside government support, in an equitable and sustainable way.

I find it hard to argue with this statement as it reflects much of the detailed research undertaken by the Retirement Income Review.

The fact is super is there to provide retirement income. It should be seen, not as a nest egg, but as a source of income in retirement.

Not a nest egg

In order to achieve this, it needs to be preserved for that purpose and that purpose only. There are currently many leakages in the system which are exploited by members, among them the use of super to fund elective surgery.

Hopefully, super funds will provide retirement income projections to reinforce this point and prepare members to think about the level of income they want in retirement and how much they can safely draw down balances.

To do this properly, people need guidance and advice, a subject addressed in the report of a separate Quality of Advice Review released this month.

Read more: The super giveaway that allows the wealthy to amass even more tax-free

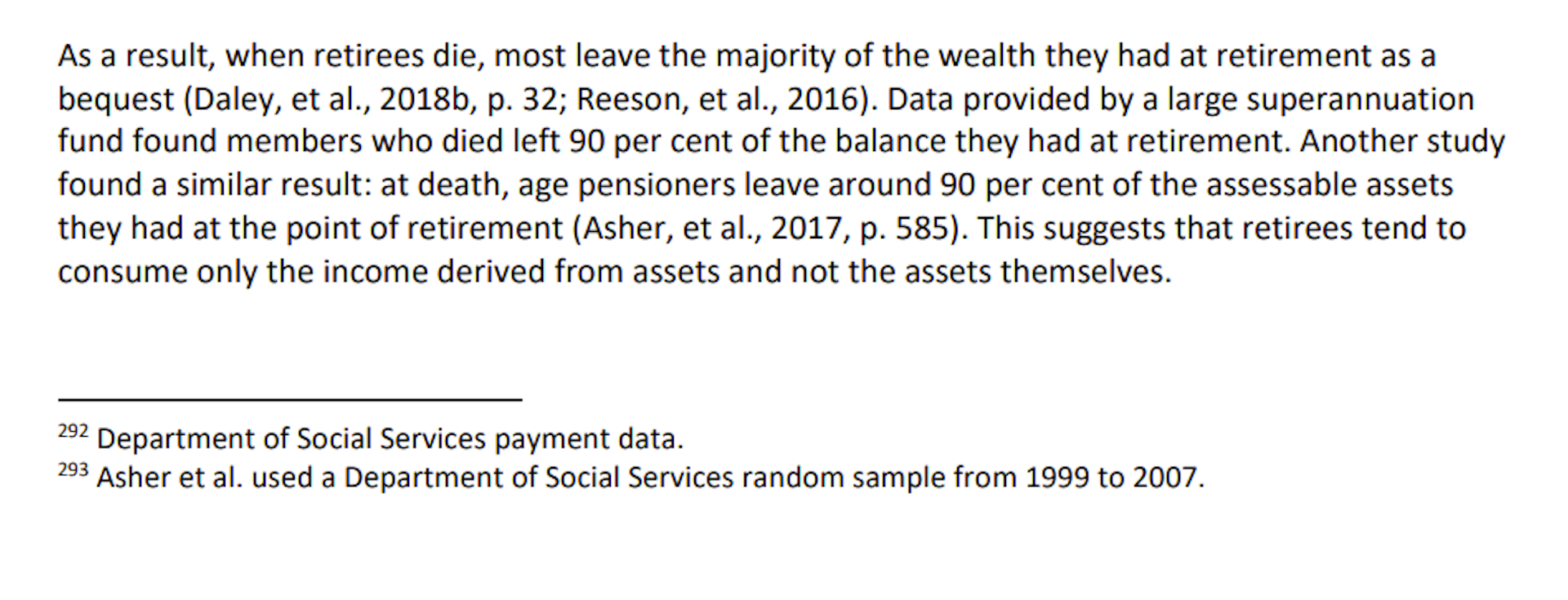

Right now many retirees are intent on preserving their super as a nest egg, to ensure they don’t run out of funds. The Retirement Income Review heard that most go to their graves with 80-90% of their super as an unintended bequest.

{kind=link}

As to a “dignified” retirement - the word proposed by Chalmers in the Consultation paper – the age pension already provides a floor for retirement income to ensure people are not at risk of poverty in retirement. It has grown faster than both wages and prices since 2009 and works well as a safety net.

The proportion of retirees receiving the pension increases with age. In mid-2019, 42% of people aged 66 received the age pension, compared with 80% aged 80.

A retirement that maintains standard of living

As super balances grow and the system reaches maturity so retirees have had the super guarantee all of their working lives, reliance on the age pension will decline, particularly for those on middle incomes.

A good goal for super is to allow retirees to maintain a standard of living commensurate with their pre-retirement income. A good way of measuring this is by use of a replacement rate - say 65-75% of pre-retirement income. Absolute targets make little sense when people have become used to different incomes throughout their working lives.

There are a wide range of government programs that help provide this, in addition to super and the pension. Programs such as health and aged care services, tax benefits, and various concessions play an important role as well.

Read more: Yes, women retire with less, but boosting compulsory super won't help

“Equity”, another word used by Chalmers, indicates that people in similar circumstances should receive similar benefits. This isn’t the case right now.

At the moment the age pension assets test favours home-owners; high income earners benefit more from super tax concessions than low earners; and women tend to benefit less than men. Some of the reasons for this are outside the retirement system itself, as are the poor situations facing renters who receive inadequate Commonwealth Rent Assistance and involuntary retirees who spend an extended period on unemployment benefits.

A sustainable system

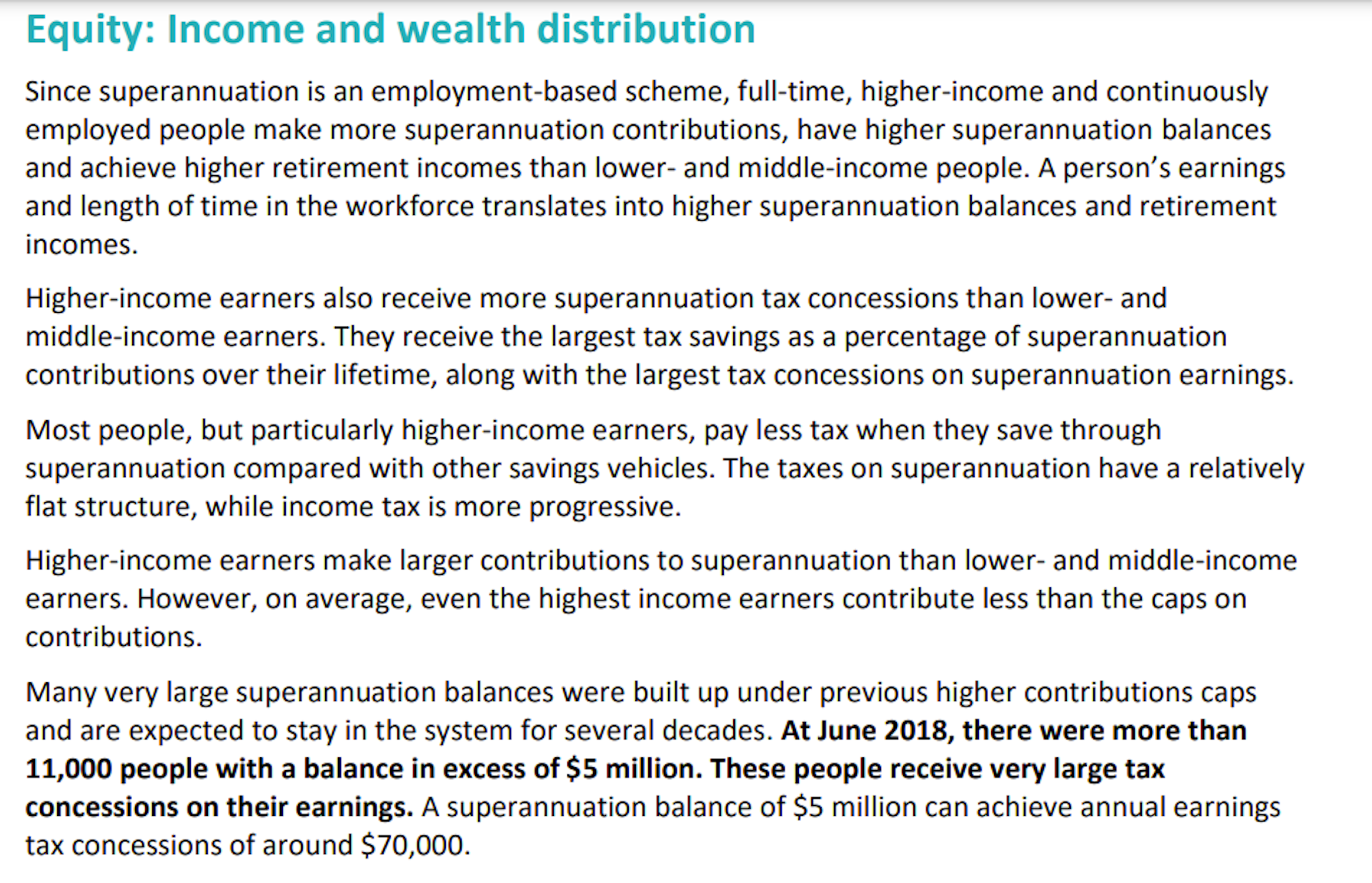

“Sustainability”, another word used by Chalmers, is needed to ensure tomorrow’s workers are not unreasonably burdened supporting today’s retirees. At present those with large super balances benefit the most from tax concessions.

The Retirement Income Review found that in 2018 there were 11,000 people with super balances over $5 million, and by now there are many more.

{kind=link}

These balances are arguably well in excess of what is needed for retirement income and the tax concessions which accrue to these accounts could fund a significant number of age pensions.

Over the next two decades these large balances will decline due to caps imposed in more recent years. In the meantime, the concessions are expensive – a tempting piece of low-hanging fruit in tight fiscal times.

Submissions on the Consultation Paper are due by March 31.

The final wording of the sentence that is chosen will be incredibly important.

It will provide a focus to guide deliberations about how much super we need, how much it should be taxed, and what it should be used for. Three decades on from the start of compulsory super, it is overdue.