Electricity privatisation is clearly the biggest issue of the New South Wales election campaign. And as the March 28 polling day gets closer, the debate is heating up, with a rush of claims and counter-claims masquerading as facts.

On the pro-privatisation side, the NSW Liberal Party, business groups and others claim prices will be lower and private electricity companies will be more efficient.

Those opposing privatisation, including the NSW Labor Party and unions, claim prices will be higher, jobs will be lost and the state’s financial position will be weakened.

Both sides of this debate are guilty of cherry-picking so-called “facts” to suit their campaigns, rather than presenting the real story to voters.

Let’s look at the claims against the full – not just selectively chosen – facts. For those wanting more detail, I have analysed three of these claims in more depth in an article published by the Economic and Labour Relations Review.

Where in Australia have electricity prices risen most?

Everyone in Australia has experienced substantial electricity price rises in recent years. That’s true whether you live in a state where the electricity companies are privately or publicly owned.

Victoria and South Australia have sold all their electricity businesses, while only some have been sold in Queensland and NSW. The generators have been sold in NSW and the retail businesses have been sold in Queensland and NSW. Everywhere else in Australia, they are still state-owned assets.

From 2000 to 2014, the Australian ABS Electricity Price Index (EPI) shows that household electricity prices in Australia rose by 174%. In comparison, in the two capital cities of the fully privatised states, Melbourne and Adelaide, the prices went up 146% and 178% respectively.

A similar picture is shown by absolute changes in electricity prices. From 2007 to 2014, the increase in average Queensland household electricity prices was 126%, compared to 115% in NSW, 103% in Victoria and 91% for SA.

On the face of it, these numbers don’t suggest privatisation leads to higher prices. If anything, there is some support for the lower prices argument.

But relying on these figures to argue for or against privatisation, as many do, is too simplistic, and ignores the more complicated reality.

Lower or higher electricity prices?

First up, the notion being pushed by both the pro- and anti-privatisation camps that privately owned electricity companies can set lower or higher prices assumes that those companies have considerable control over price setting. The reality is, they don’t.

Our electricity prices are the result of complex regulatory processes. The electricity price you pay includes charges for generation, transmission, distribution and retail services.

The Australian Energy Market Operator (AEMO) determines the generation charges. The Australian Energy Regulator (AER) sets the transmission and distribution charges. Retailers set the retail component in NSW, Victoria and SA, while elsewhere government regulators do. Plus there are charges for environmental programs like the Renewable Energy Target. Your electricity supplier determines the final price, based on all these charges.

Charges for “poles and wires” form the largest component of your electricity price, so any change will noticeably impact. And this is what we have experienced.

More than anything else, higher network charges caused the skyrocketing electricity prices that all households have noticed. NSW’s independent pricing regulator, IPART, estimated that NSW network charges increased by more than 90% in real terms for the five years to 2012-13.

The largest part of these regulated network charges is the company’s rate of return. The AER decides on this rate, taking into account things such as proposed investment.

Importantly, there has been little difference in the high rates of return set for privatised and non-privatised distribution companies. The political pain of those ever-rising electricity prices led to a tightening of the AER’s regulatory powers in 2012, and notably lower rates of return have since been proposed.

During 2009-2014, A$43 billion was invested in networks, of which 84% was for distribution, a 60% real increase over the previous five years. The much larger and aged assets of the state-owned NSW and Queensland networks accounted for the lion’s share. Not surprisingly, these states had greater increases in network charges (and thus electricity prices) than the states with privatised electricity.

But does that mean that public electricity is inherently more expensive than privatised electricity? No.

Much of that investment in NSW and Queensland was to meet higher reliability standards, set by regulation on a state-by-state basis, and (unrealised) demand forecasts issued by the AEMO. Regulators are lurking everywhere in our electricity prices.

One report, upon which the NSW government has placed much weight, claims private network companies have lower charges over the long-term. But this analysis is flawed. Important differences between the size of networks and age of assets are not considered.

There are also unproven claims of “gold plating” – that is, more-than-necessary investment to generate higher profits.

The reality is that Australian electricity prices are driven by a complex web of regulation that does not discriminate between private and public companies. All Australian governments agreed to, and continue to support, this regulatory regime.

NSW Premier Mike Baird has made an election commitment “guaranteeing” lower network charges in 2019 from privatised NSW companies, compared to 2014 charges. Baird has also said he would appoint former competition watchdog chairman Alan Fels to oversee that “price guarantee”.

This suggests Baird either has a poor understanding of the current regulatory regime, or he has no confidence in it driving prices down.

In summary, the evidence does not support either side’s claim that electricity privatisation leads to higher or lower prices.

Loss of jobs?

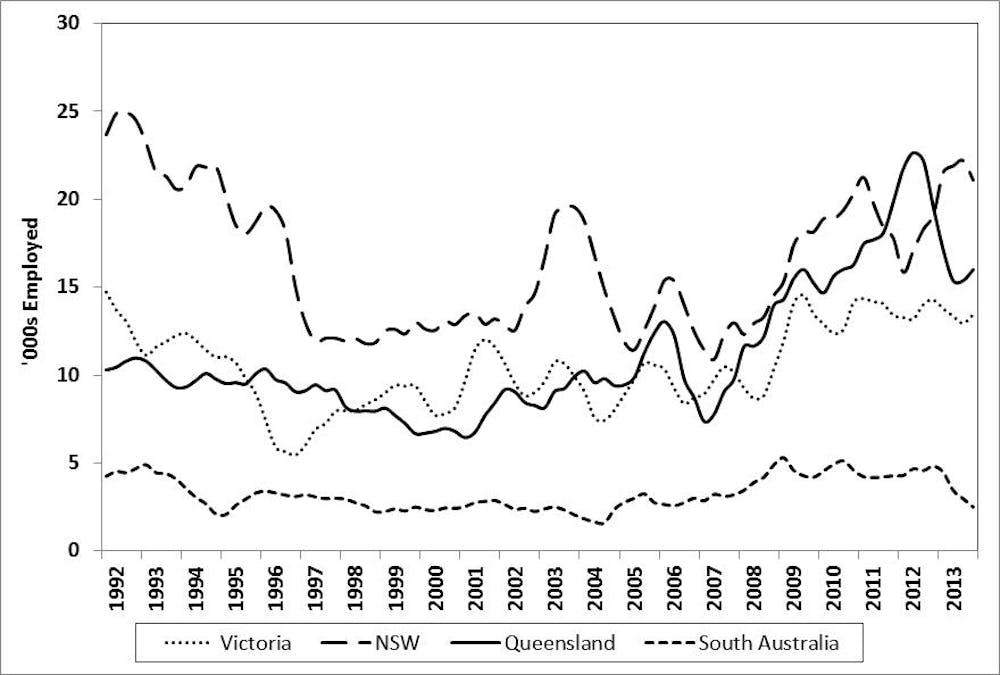

Australia’s electricity sector employs around 66,000 people – more than before the privatisations began – although there was a big 1990s downsizing.

Putting aside the volatility in survey data, the ABS figures show clear trends. Numbers rapidly fell as Victoria and SA _readied _their electricity businesses for sale, and as the other states split and corporatised their businesses.

NSW accounted for 40% of the 1990s downsizing, with a further 20% in Victoria. Both states have since experienced strong jobs growth. In fact, Victorian jobs started to grow before those privatisations were complete in 1999.

The NSW generation and retail privatisations during 2010-12 were immediately preceded by an employment decline, although that was not evident before the 2014 sale of Australia’s largest generator, Macquarie Generation.

Census data shows both privatised and government-owned distribution networks were the big source of jobs growth during 2006-11. This coincided with the increased investment in “poles and wires” in a number of states, particularly in NSW and Queensland.

The Australia Institute has shown employment growth, during the network investment spike, has been accompanied by a stark shift - in both public and private electricity companies - away from technical and trade jobs towards managerial and administrative positions.

The evidence does not show job losses automatically follow a privatisation. Instead, significant labour shedding occurs prior to sale, while still in government ownership.

Greater efficiency?

Many theoretical reasons are given for privatisation leading to greater efficiency. But there is little, and contrary, evidence to prove the impact of ownership type.

Studies by IPART and the McKell Institute found government-owned electricity companies to be either more efficient or comparable with their peers. Yet the AER reported privatised distributors “generally appear more productive” depending on the performance indicator.

ABS figures show substantial labour productivity gains in the electricity sector as output (meaning electricity consumption) grew and jobs fell in the 1990s.

After 2000, productivity growth turned negative as demand flattened and employment steadily rose. This decline accelerated with the huge investment program in “poles and wires” (distribution) networks. That’s not surprising, given distribution accounts for 50% of the sector’s employment, and more than 70% of jobs growth since the mid-2000s.

The evidence is not clear-cut that private electricity companies are more efficient.

The bottom line

Does privatisation always lead to higher or lower electricity prices? No – neither side’s claims on this are supported by the evidence. Our electricity prices are driven by a complex web of regulation that does not discriminate between private and public companies.

Are electricity privatisations followed by massive job losses? No. And there are more electricity industry jobs now than before privatisations started.

Are electricity businesses more efficient in public or private hands? The jury is still out.

Too many of the frequently repeated claims about electricity privatisation are myths, which are not borne out in reality.

It’s time for both sides of this debate to stop recycling misleading, unsubstantiated claims, cherry-picked to suit their arguments, and instead to engage in a debate grounded in the facts.