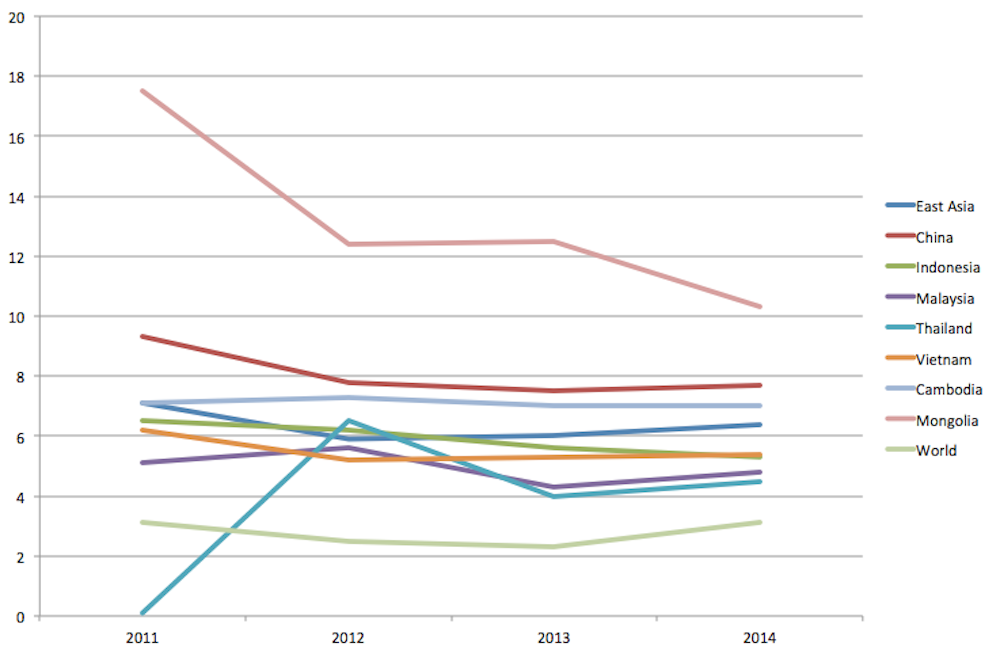

East Asia’s growth is slowing as China focuses on domestic demand growth from weaker exports, according to a World Bank report released last week. But East Asia will still grow faster than other regions, with projected growth of 7.1% for 2013, and 7.2% for 2014.

East Asia contributes 40% of the world’s GDP growth and continues to be the engine for global economic growth. But Chinese investment in the region has slowed more than expected, the report found.

China’s growth is expected to meet its target of 7.5% this year on the back of stronger industrial production in the third quarter of 2013. And growth will head to 7.7% in 2014 amidst growing signs of a global recovery in the second and third quarters of 2013.

This is consistent with the OECD’s forecast. Last week’s Economic Outlook 2014 report said China’s growth would remain around 7.7% per year between 2014 and 2018.

Growth projections

The Chinese economy still faces disruptions as it undergoes restructuring toward greater domestic reliance and modernisation in pursuit of a more sustainable growth path.

And China faces a range of challenging domestic and global conditions, such as speculation on the withdrawal of US quantitative easing and an appreciating domestic currency.

The move to high-value added production – outlined in the mid-term review of China’s 12th five-year economic plan – has seen industrial rebalancing that could result in less investment in low cost manufacturing and more into sectors that provide a more sustainable growth path.

Still making things

Shrinking demand and the increasing cost of labour-intensive exports have seen manufacturing contribute less to GDP growth than in previous years. This will have an adverse effect on the traditional suppliers of capital goods and industrial raw materials to China, as softening of commodity prices – metals, palm oil, rubber and non-oil energy – impacts growth across East Asia.

China experienced a 12% increase in retail spending in 2012, still relatively small for consumption as a proportion of GDP. The OECD’s economic outlook emphasised that private investment would underpin overall investment growth. So China’s success in moving from export to domestic-driven consumption will be critical for investment and growth.

Private Chinese firms instead of state-owned ones are becoming the engine of growth for the economy. These firms traditionally dominate the consumer sectors and their investments will increasingly be a major contributor to China’s growth.

But while these private sector firms constitute some of China’s largest businesses, they lag behind their western counterparts in technology, marketing, and governance skills. And they encounter strong competition from foreign players in the domestic and international markets.

Time for reform

Domestic demand is expected to slow as China’s global financial crisis stimulus programs are slowly phased out. Any expansion of credit is unlikely to boost GDP in the last quarter of 2013 because the most recent expansion in credit has been less effective in generating growth.

There is unlikely to be any significant change in growth projection in the short to medium term. This poses an immediate risk of a decline in investment in China unless major structural reforms to boost demand and the economy take a foothold.

It is good news the new Chinese leadership is encouraging just that by changing the household registration system and reforming the financial sector.

China’s GDP growth is expected to meet World Bank targets in 2013 and 2014, but key economic indicators are likely to move downward in the medium term as its economy continues to undergo rebalancing, modernisation and stiffer competition in the manufacturing sector.

Medium term growth is expected to remain between 7.5 and 7.7% until 2015, according to the World Bank report, but long term growth is expected to stabilise between 5-6%.