The European Central Bank’s announcement of a potentially indefinite, albeit tapered, extension of its quantitative easing (QE) programme appears very different to what is happening elsewhere. The US halted its programme last year, while the UK’s return to QE in response to Brexit seems, for the moment, to be temporary. The US also raised interest rates on December 14 and signalled more rises next year, a move in the opposite direction. What are we to make of it all?

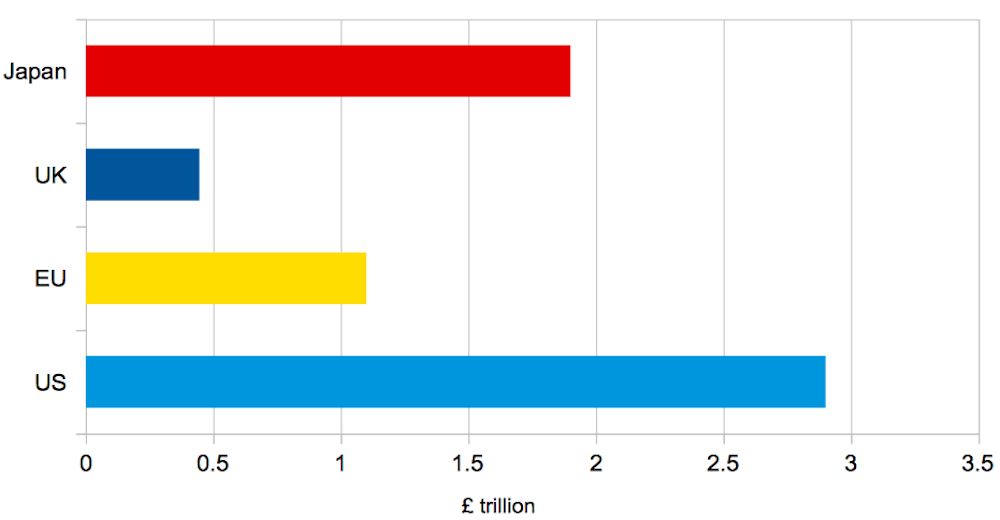

The ECB was late to quantitative easing, the stimulus system that sees central banks create new money to buy assets from other banks. It launched its programme to spend €60 billion on bonds each month as recently as March 2015. Having increased to €80 billion/month in April of this year, the new announcement extends the current end of the programme by nine months to the end of 2017 and cuts monthly buying back to €60 billion. By the current end date, the total stimulus will have been €2.2 trillion (£1.8 trillion).

By comparison, quantitative easing in the US ran from 2008-15 and totalled US$3.7 trillion (£2.9 trillion), while the UK’s £375 billion programme ran from 2009-12 before its August revival for a further £70 billion of purchases. On the other hand, Japan is still aggressively using QE, and will hit about £1.9 trillion by year end and £2.4 trillion by the end of 2017.

Quantitative easing around the world

QE is the ECB’s response to deflation in the eurozone in the aftermath of the 2007-08 financial crisis. These years of debt reduction by households, firms and countries have the potential to lead to a widespread contraction. QE helps prevent this by pumping money into the system, thereby putting a floor on the money/liquidity supply and hence asset prices and aggregate demand.

Under the programme, the ECB buys sovereign and corporate bonds from banks within the eurozone. This drives up the prices of the bonds, which simultaneously reduces their yields (interest rates) and improves the balance sheets of the banks that hold such assets. This should enable them to lend at the most competitive rates possible.

QE also causes currencies to depreciate, meaning it should stimulate exports – and sure enough the euro promptly fell against the dollar and pound after the latest ECB announcement. This more favourable climate then props up share markets and the prices of other assets such as commodities and bonds as investors snap up what they see as bargains.

Apart from the fact that the monthly stimulus has been cut by a quarter, the other notable change to the ECB’s programme is that it is now prepared to buy bonds with a maturity of less than two years and with a yield of less than -0.4%. This is basically a signal that there are not enough longer term, higher yield bonds available, which has important consequences.

As was demonstrated after the announcement, the yields on the short-term sovereign bonds of especially Germany fell sharply, but the yields on longer term debt rose – meaning market demand for the short-term bonds was up while for the long-term bonds it was down. The effect was particularly pronounced for the sovereign bonds of Italy, Spain and Portugal. It is long-term bonds that affect interest rates for businesses and consumers. By stimulating demand for short-term bonds, the ECB is instead offering an opportunity for governments like Germany to access cheaper money by issuing more of them.

The limits of QE

The benefits to the private sector from eurozone QE in the future look limited – it is unlikely to make money much cheaper for them and in any case the evidence is mixed that QE stimulates aggregate demand over the medium term. Business investment and consumer spending are therefore only likely to pick up in a sustainable way when people and companies become more positive about the prospects for the economy.

In the meantime, public sector investment on the back of the cheaper short-term bonds has a key role to play in stimulating growth. The cost of public sector borrowing in the eurozone is at historical lows, making it affordable for governments to cut their deficits at a slower pace.

This has made a stronger economic case for greater government investment in public goods like infrastructure, research funding, higher education, training and skills, and green technology. One attraction of such policies is that they encourage business investment in the longer term by tempting companies with everything from better educated workforces to infrastructure contracts to lucrative subsidies.

One stumbling block is that less competitive countries such as Greece have been expected to adjust their economies with severe cuts to public spending (since the old solution of devaluing the drachma is not an option in a currency zone). If we are relying on governments to take advantage of the conditions created by QE, we have to stop hampering them in this way. The eurozone potentially needs to look instead at the case for creditor countries like Germany spending more – potentially changing the rules by which the eurozone is run.

The instability caused by very different economies using the same currency remains the key policy concern in the eurozone, but other issues will not go away. These include underlying anxieties about inequality, the impact of an ageing population on the sustainability of the welfare state and the relative power and privilege of Western economies. This points to the need for reforms to things like state pension systems and healthcare and restructuring struggling economies.

What eurozone QE is doing is to give governments the breathing space to make changes that will unlock private investment and make national finances more viable before national debts become unmanageable. But QE cannot go further and be a substitute for these kinds of reforms. Policy reform that encourages innovation, education and trade will eventually lead to more growth in the eurozone. The challenge is to hold the bloc together and avoid a financial crisis long enough to let them take effect.