“The changes to lifetime health cover will increase [private health insurance] premiums by up to a reported 27.5%. This is hitting many local residents very hard, with some struggling to find the money to pay an annual increase of more than $1000.” Liberal member for the marginal seat of Boothby in South Australia, and shadow parliamentary secretary for primary health care, Andrew Southcott, e-newsletter, 5 July.

The Lifetime Health Cover (LHC) loading is an additional charge of 2% on top of an individual’s private health insurance hospital premium for every year that an individual is aged over 30 before they take out cover. Introduced by the Howard government in 2000, it was designed to encourage younger, fitter people to take up private health insurance and to penalise them if they delayed. The maximum loading on top of their normal premium is 70%, which is removed once a person has held hospital cover and paid the loading for 10 continuous years.

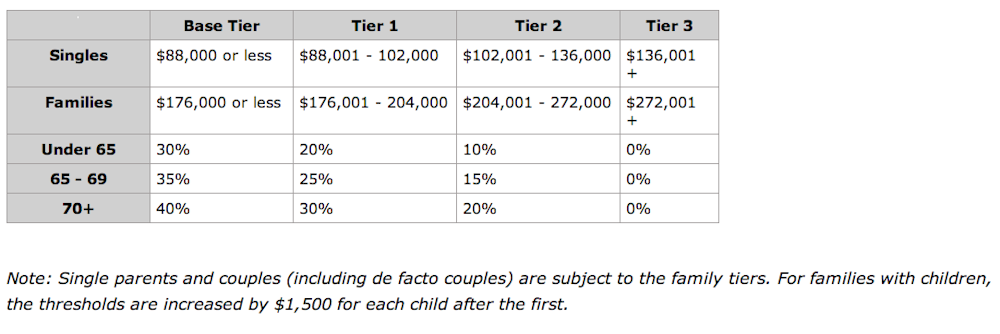

Changes under the current Labor government have tightened up who is eligible to receive an up to 40% government rebate towards paying for private health insurance.

Since 1 July 2012, the private health insurance rebate has become income tested. Individuals aged below 65 years with incomes below $84,000 receive a 30% rebate, rising to 35% and 40% for individuals aged over 65 and 70 years, respectively. (Click on the table of rebates by age and income below for more detail.) The rebate gradually reduces to zero for incomes above $124,000.

And from 1 July this year, the government will no longer pay this rebate towards an individuals’ lifetime health cover loadings. This provides a further incentive for people to take out insurance at an earlier age. The Australian Tax Office uses this example to illustrate how the change will reduce people’s rebates:

“On 1 July 2013, Rebecca pays a premium for two months cover under a complying health insurance policy of $220. Due to Rebecca’s circumstances, she incurs a 10% increase in her premium because of the LHC loading. The base premium for the policy is $200 and the LHC loading is $20. Rebecca’s income is $59,000 and she is eligible for the 30% rebate. Rebecca receives a rebate of $60, which is 30% of the $200 base premium. Rebecca does not receive any rebate on the $20 paid for LHC loading.”

What’s the source of this $1000 claim?

The Conversation’s Election FactCheck contacted Dr Southcott’s office to request a source for his claim about “an annual increase of more than $1000” for some residents. His communications officer replied:

“Andrew was contacted by a married couple who had received notification from their private health provider [Medibank Private] of the increase in their premiums and were concerned about their ability to find the extra funds, on what was already an extremely tight budget.

"I have attached a copy of those letters for your information. As you can see, the combined increase to their premiums for the couple comes to $1,011.60 annually. (Note that due to the identical figures we were very careful to establish with them that this increase was, in fact, being borne twice by the couple and that figure did not represent a joint cover. While we have redacted the details for privacy, the membership numbers are different on each letter.)”

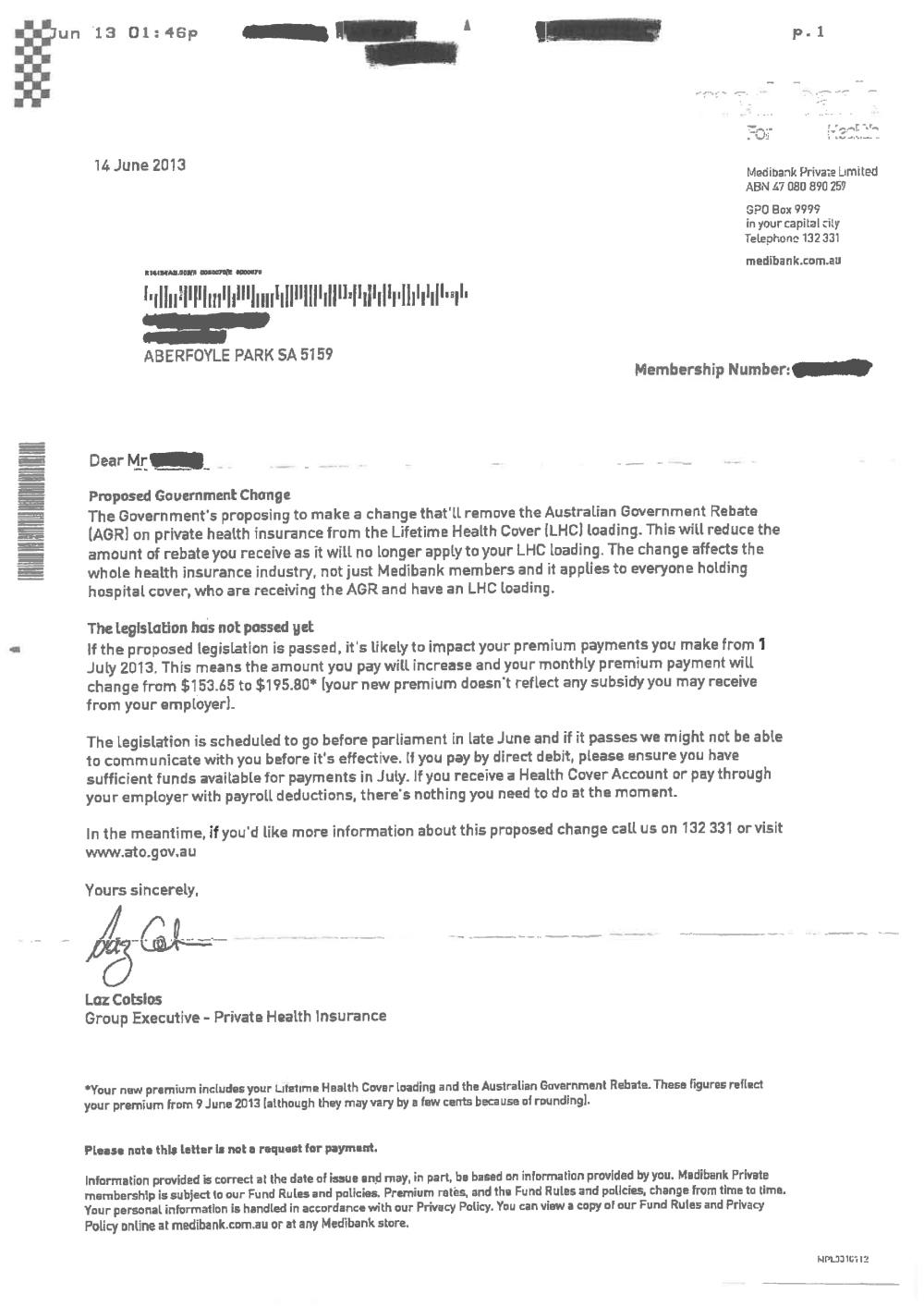

A copy of one of those June 2013 letters to the couple from the southern Adelaide suburb of Aberfoyle Park (right: click to zoom in) shows that each of their old insurance premiums was $153.65 per month, but that that would increase to $195.80 following the government’s new changes to lifetime health cover. When you add that up for this couple, it comes to a combined increase of $1011.60 per year.

The Medibank Private letters suggest that all of that cost increase is due to the new lifetime health cover changes.

Do the numbers add up?

Although the details of this couple’s age and income were not available for privacy reasons, I calculated how Medibank Private came up with this figure, using the premium rates provided in these letters.

I found that the cost increase indicated in the letters would be correct if both individuals are aged over 70 years (and so receive a 40% rebate), they did not take out private insurance until they were aged 65 years or older (and so are subject to the maximum 70% LHC loading), and they have had private insurance for less than 10 years (the LHC loading does not apply to individuals who have held private insurance continuously for 10 years or more).

Given these characteristics, I worked out what their full premium would have been, with no rebate at all. This worked out to be $256 for each individual a month. (40% of $256 is $102.45, which when added to their current premium of $153.65 equals $256.)

Then I calculated the LHC loading component of the $256 premium, which came to $105.40. (The non-LHC component is $150.60, 70% of $150.60 is $105.40, which when added together equals $256).

Finally, if they were getting a 40% rebate on their lifetime health cover component, then that would work out to be $42.16 a month (40% of $105.40). Multiplied by 12 months, that comes to a total increase of $505.80. For the couple, the combined increase is $1011.60.

This couple have very specific characteristics that mean they are subject to such a large impact of the removal of the LHC rebate. Very few individuals pay a 70% loading, whilst receiving a 40% rebate, on a hospital plus general treatment insurance policy.

Let’s look at a couple of other, perhaps more common scenarios. For example, an adult earning $110,000 per year, with hospital cover taken out for the first time at age 50 years, would pay an extra $20.64 per year (based on a monthly premium of $86).

Alternatively, a family with children with an annual income of less than $176,000, where the adults took out hospital cover for the first time at age 40 years, would be paying an extra $67 per year (based on a monthly premium of $186).

Verdict

Dr Southcott’s statement that “some [local residents are] struggling to find the money to pay annual increases of more than $1000” is correct. However, it is important to note that only a small number of Australians would be in the difficult position of this particular couple, given only 13% of individuals pay any lifetime health cover loading at all, let alone the maximum rate of 70%.

Review

In order to check if this analysis was correct, I asked myself what would be the most extreme case of disadvantage brought about by the changed tax arrangements. I modelled a couple who took top hospital cover without excess, for the first time after age 70, and found that, as a couple, they would pay an extra $1230. So in that extreme scenario, the cost for two people would be even higher than in the case Dr Southcott has brought to our attention.

But such cases are outliers. As this author has pointed out, the majority of people who take out private health insurance do so when they’re much younger.

There is a surge of membership at age 30, when the lifetime loadings start to take effect, but there is no surge in membership at later ages. In fact, there are sharp falls in membership at ages 65 and 70, in spite of the higher rebates at those ages. Presumably this is because around those ages, people’s income falls and they are therefore no longer subject to the Medicare Levy Surcharge.

There are a few people who, in a calculating way, may take out cover only when they’re older, but such people tend to take only very specific cover, and are unlikely to take top cover or ancillary cover.

The two final scenarios modelled by this author, showing increases more in the order of $20-$67 a year, are far more typical. Without more information I cannot check them specifically, but in similar modelling I have found similar figures. - Ian McAuley