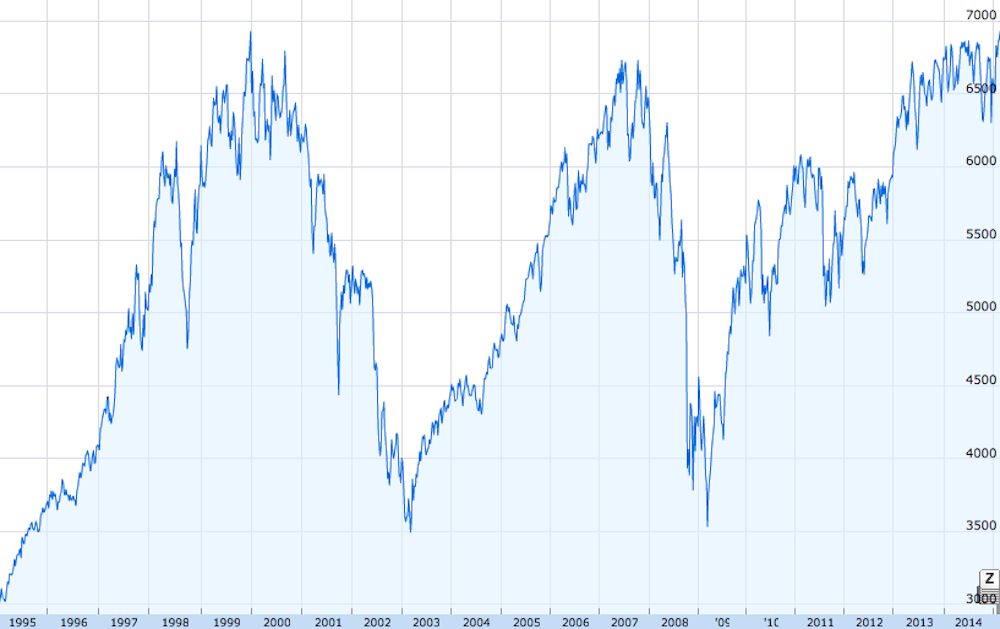

The FTSE 100 may have ticked down slightly since hitting an all-time high of 6,949.24 on February 26, but it remains above the previous record peak of 6,930.2 set more than 15 years ago on December 30 1999.

Of course, for the result to be truly meaningful you have to adjust for 15 years of reinvested dividends, inflation, tax and transaction costs. Having accounted for these adjustments using data from Bloomberg and Thomson Reuters Datastream, I found that the total real return of the FTSE 100 over this period is only negligibly different from zero. Atypically, in other words, this is a case where the nominal and adjusted 15-year returns coincide.

The difference between the highs of December 1999 and February 2015 is that the former occurred just a few months before the peak of the dotcom bubble, the greatest stock market overvaluation of all time.

FTSE 100 over 20 years

Why the FTSE is no longer overvalued

When stocks are grossly overvalued, a long period of poor stock-market returns is naturally what we would expect. The past 15 years’ performance is in line with what was predicted by the historical record of previous bubbles and the valuation models of behavioural finance, not to mention ordinary common sense.

After 15 years of corporate profit growth, albeit with the intervening global insolvency crisis of 2008, the FTSE is now on a respectable dividend yield of 3.6% and a price-to-earnings (P/E) ratio of 16 – compared to a 2% yield and a P/E ratio of 27 at the 1999 peak. When measured against historical averages, the index is now close to fair value.

So having broken one psychologically significant barrier and within sight of another, the 7,000 level, what are the prospects of the FTSE soaring over the coming months? Probably not very great.

Odds and the general election

The UK general election of May 7 is setting another record: the toughest to call since 1974. Pre-election odds consistently outperform the predictions of both professional political experts and surveys of voter intentions. This is true not only in the week immediately preceding the election, but also months in advance.

The betting odds currently predict a better performance for the Conservatives than either political pundits or surveys. They imply a probability of 16% for a Conservative majority, but only a 9% probability for a Labour majority. The predictions of political commentators and surveys, on the other hand, have tended to favour Labour.

The betting odds are giving a probability of more than 75% for no overall majority. Combine this with the much higher probability of a minority government, hung parliament or a variety of potentially unstable coalition arrangements and you can only conclude that the UK is facing more political uncertainty than in the run-up to any election in decades.

The political threat

The outcome has the potential to make a difference to the markets. Labour is perceived to be anti-business and particular sectors are under threat. Utility companies have reason to fear Ed Miliband’s promised temporary freeze on utility prices, while the banking sector faces the possible break-up of the too-big-to-fail banks.

On the other hand, the political risks for the stock market would not disappear on the election of a Conservative majority. David Cameron’s promise of an in-out referendum on membership of the EU would lead to an extended period of great political uncertainty. Needless to say, the consequences for the stock market of the most likely outcome, no overall majority, are complex.

Markets hate uncertainty. Whether caused by political or economic factors, it is generally accompanied by increased volatility and falling stock prices. Many institutional investors are already lowering their exposure to the UK market and adopting a wait-and-see attitude towards future purchases of UK stocks.

Political uncertainty is not the only factor affecting stock prices, of course. The trends for the UK and US economies have been positive for some time, for example, and the recent move to quantitative easing by the European Central Bank is already pushing European stock prices higher.

There appears to be no particular reason why the UK market should crash. But given the exceptionally high degree of political uncertainty and the consequent cautious approach to the UK market being taken by institutional investors, the UK stock market is unlikely to fly in the near future either.