General Electric is retreating from the financial sector and returning to its industrial roots seven years after its finance unit nearly brought down the company.

After Lehman Brothers’ collapse in September 2008, GE was saved only by the largesse of the federal government, borrowing billions through several different programs set up to fight the financial crisis.

The company’s shift, announced in April, is a crucial development and is in part the result of the passage of the Dodd-Frank Act, which turned five years old this week.

GE, which reported revenues of almost US$150 billion from dishwashers, jet engines and other products last year, is an iconic American company and a bellwether of the economy. Its embrace of finance to boost stagnating profitability in the 1980s mirrored changes in the broader US economy. That shift triggered a host of socioeconomic problems such as increased inequality and almost caused the global economy to collapse in 2008.

GE’s retreat from finance might signal that the role of industrial companies in the US economy may once again be on the rise. Such a “de-financialization” could boost American innovation in more productive sectors – especially those in research and development (R&D) and capital-intensive industries – help reduce inequality, and make it less likely that the next financial crisis will snowball into an existential one.

Seeking profits in finance

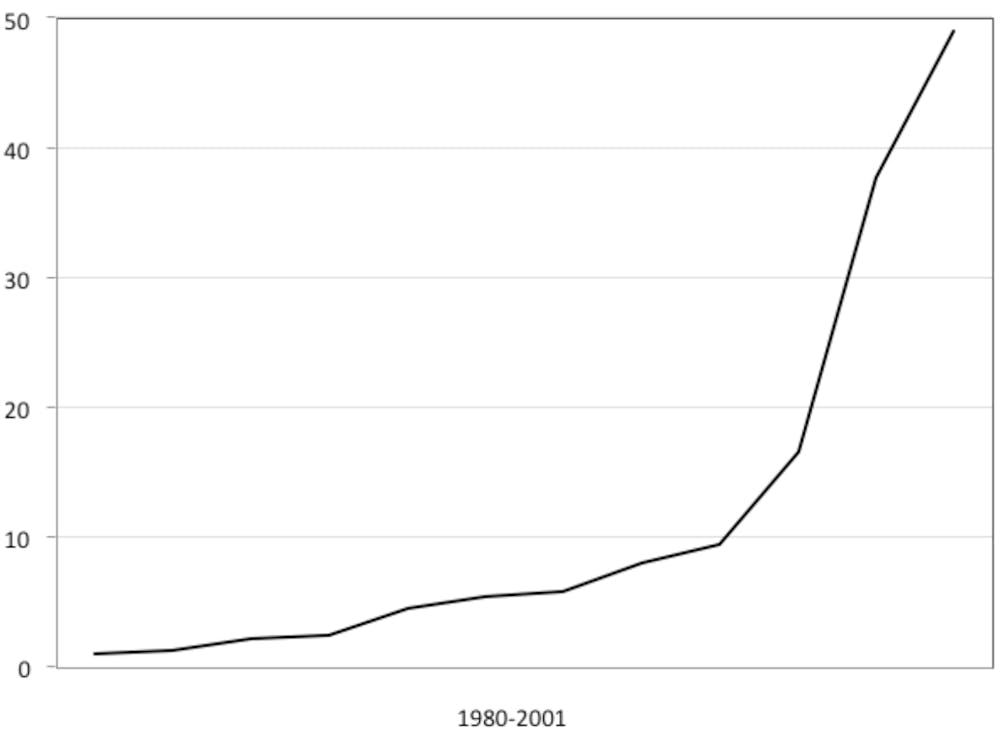

Since the early 1980s, economic activity in the US has steadily moved away from manufacturing to more financially oriented activities.

For example, the financial services sector contributed 7.9% to US GDP in 2007, up from 4.9% in 1980. A major part of this development was the increasing dependency of nonfinancial corporations on financial activities and institutions.

For industrial companies whose profitability had begun to decline in the face of growing foreign competition, the turn to finance meant continued growth and profits, thanks in particular to high interest rates.

Nowhere was the turn to finance more visible than at GE under then-CEO Jack Welch. As a 1997 BusinessWeek article noted, “Welch barnstormed through GE shutting factories, paring payrolls and hacking mercilessly at its lackluster old-line units.”

By the time Welch’s tenure ended in 2001, finance accounted for more than half of GE’s revenue and more than a third of its profits.

Financialization rewarded GE. Stock prices grew immensely through the 1980s and 1990s, a good indicator that stock investors and analysts favored this transformation. A 1997 Fortune magazine article noted that GE Capital “powers GE’s earnings, drives its stock and scares the hell out of its competitors.”

Financialization’s dark side

For GE, the flaws in this transformation didn’t manifest themselves until 2008, when Lehman Brothers’ collapse caused a short-term credit crisis that nearly destroyed the company. But for the economy and its workers, the negative impacts began much earlier and were far-reaching.

To begin with, starting from the 1980s, it led to a much-changed conception of the firm in the business world. Firms began to be viewed as a bundle of tradeable assets that exist to return value to their shareholders. Major corporations led by finance-oriented managers made the stock price their primary concern.

The linking of executive pay to stock options promoted this trend. The focus of CEOs and boards shifted away from long-term productive investments toward quick financial gains. The profitability of the companies that turned to finance increased, but employment and economic growth stagnated in the largest nonfinancial firms, in part due to this development.

The bargaining power of labor also diminished. The focus on short-term profits gave firms incentive to cut labor costs, while rewarding top executives who made such decisions. All in all, financialization led to shrinking net wages for many workers operating in the productive industries, and contributed to the widening income inequality in the US and across the advanced nations.

The prevailing paradigm shifts

The 2008 economic crisis was essentially a crisis of a financialized economy run amok. The prevailing paradigm up until the crash was to let markets, including financial markets, self-regulate.

As Barney Frank would recollect later regarding his work on the House Financial Services Committee in the US Congress:

When I was about to become the chairman of this committee in 2006, I was told by a range of people that our agenda should be that of further deregulating financial markets. I was told that excessive regulation was putting American investment companies and financial institutions at a disadvantage.

The crisis disrupted this paradigm. Even Alan Greenspan, who had shepherded financial deregulation and promoted financialization during his 19-year term as chairman of the Federal Reserve, admitted that he had put too much faith in the self-correcting power of free markets.

The result of this change of heart was the Dodd-Frank Wall Street Reform and Consumer Protection Act, which President Barack Obama signed into law in July 2010. The act led to the establishment of the Financial Stability Oversight Council (FSOC) to detect and preclude excessive risks to the US economy arising from the distress of large, interconnected bank holding companies, or nonbank financial companies.

The council is authorized to designate companies whose financial failure could pose a threat to US financial stability as systemically important. Such companies will be subject to increased regulatory supervision by the Federal Reserve and other relevant prudential regulators.

So far, the council voted to designate American International Group, General Electric Capital, Prudential Financial and MetLife as systemically important. With their hundreds of billions of dollars invested in finance, these companies were believed to have a significant impact on the health of the financial sector and the overall economy. Or put another way, they were simply too big to fail.

Dodd-Frank changes the game

Although Dodd-Frank might not be the most effective piece of legislation one would hope for after a crisis of this size, it has clearly changed the playing field – certainly for GE.

GE Capital, which was once deemed the overall company’s most dynamic component, suddenly became its riskiest. GE’s stock price began to fall, reflecting the concern that investors and analysts had over the risk GE capital imposed.

In retreating from finance, GE’s leadership not only aims to relieve itself of the burden of being considered too big to fail and the extra regulatory scrutiny, but also hopes that the shareholders will give its stock a more favorable valuation.

Last week the company offered its first report card on the transition when it released second-quarter earnings, which showed better-than-expected revenue thanks to growth in its core industrials business. This suggests its plan to move away from finance is working.

GE said that it had already signed $68 billion worth of sales for its lending business, putting it on track to meet its $100 billion goal by the end of the year. GE Capital had about $500 billion in assets at the end of 2014.

There and back again

GE’s journey from an industrial firm to a highly financialized one and back encapsulates some of the most critical elements of the transformation of American capitalism over the past few decades.

It is rather soon to tell whether GE’s retreat from finance is harbinger of a more structural and long-term transformation in the American economy. After all, the logic that seems to be driving the company’s retreat is the same logic that once drove it into finance: increasing its stock price.

Still, this development suggests that times are changing, however slowly, and Dodd-Frank deserves some credit for altering the incentives and calculations of the investment community. Let’s hope more companies join this trend.