CAMA’s Shadow Board, which gives its views ahead of the decision by the Reserve Bank of Australia, continues to support the current setting of the cash rate at 3.5%.

But economists are seeing a greater likelihood than last month that interest rates should fall, citing weakening global growth, declines in bulk commodity prices, ever-present rumours of a Greek exit from Europe and rising unemployment over the next 12 months.

HSBC Chief Economist Paul Bloxham said he believes domestic growth is easing but said there were tentative signs that looser monetary policy is supporting the interest rate sensitive sectors of the economy.

Bank of America economist Saul Eslake said he expected an “upwards drift” in the unemployment rate over the remainder of this year.

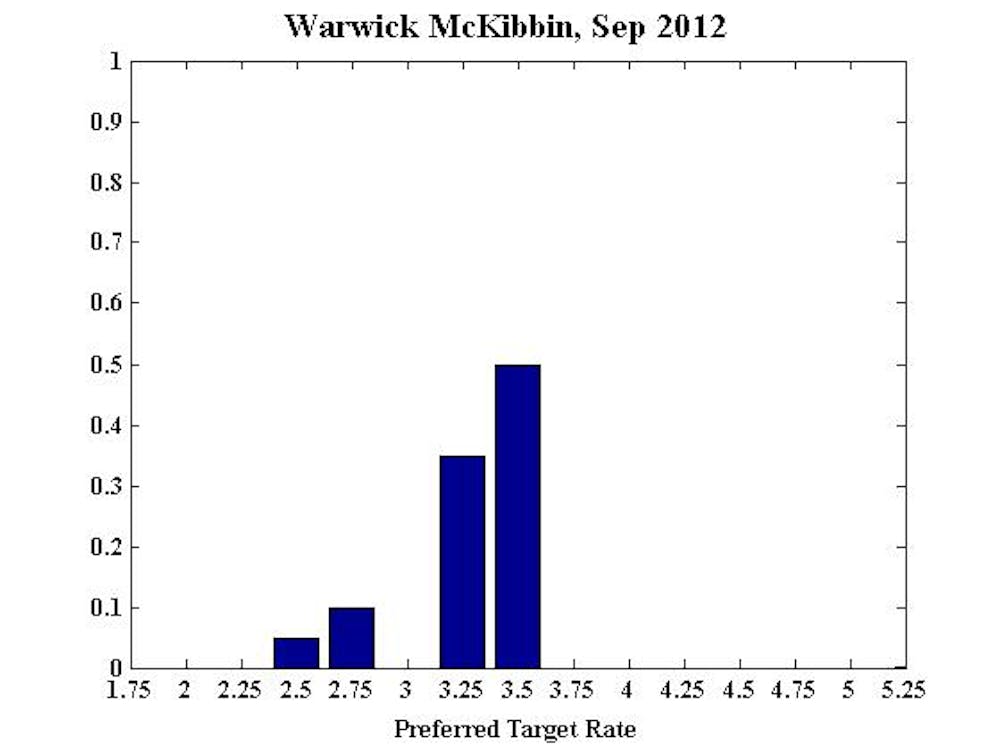

Professor Warwick McKibbin has questioned the federal government’s commitment to a surplus, saying it would now require either more substantial spending cuts or increases in taxes, “just at a time when income growth is being slowed by falling export prices”.

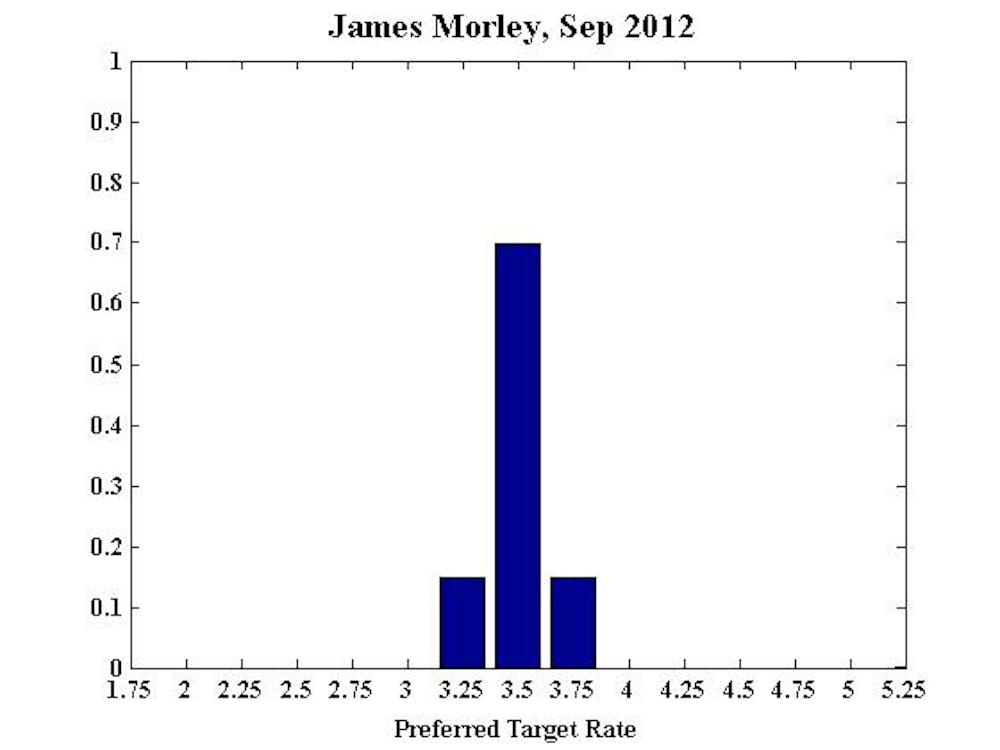

However, Professor James Morley said incoming data continues to suggest solid conditions for the domestic economy, with strong output growth and a low unemployment rate.

He said concerns around the global effects of ongoing problems in the Eurozone has diminished, with the European Central Bank hinting at a “more accommodative policy”.

Keeping the interest rate unchanged at 3.5% received around 65% weight, considerably above the next most popular setting, a decrease to 3.25%, with nearly 20% weight.

Support among the Shadow Board Support for a decrease in the cash rate (of 25 basis points or more) received a weight of approximately 25%.

In contrast, the support for an increase (of 25 basis points or more) is less than 10%.

In August, the corresponding figures suggested both more upside risk, and less downside risk. On the 12-month horizon, CAMA’s Shadow Board sees more uncertainty, with a greater range of interest rate settings envisaged than for the current month, with upside risks balanced by downside risks.

The Shadow Board is made up of influential economists from the private sector and academia. They were asked to rank their preferred outcomes for the cash rate.

Read the comments in full below.

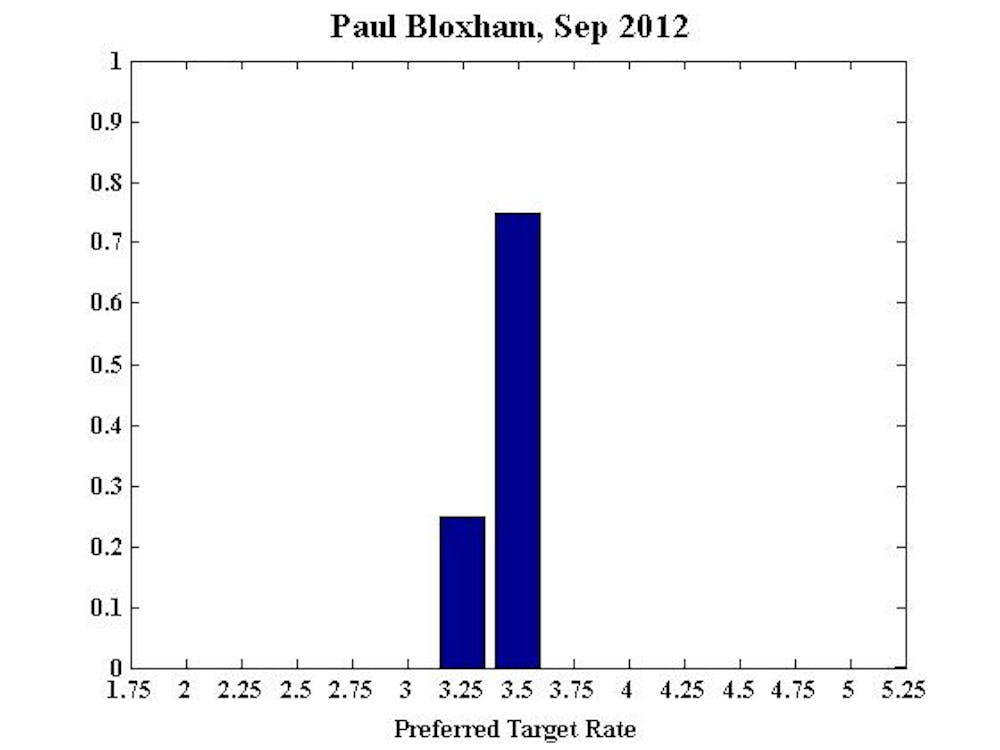

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

I would recommend the RBA keeps the cash rate steady this month, though am more willing to accept that a cut should be considered than I was last month. This reflects that the global data have weakened further and particularly that Chinese growth has continued to slow.

Weaker Chinese growth has been reflected in declines in bulk commodity prices, which will put further downward pressure on income growth in Australia. While domestic economic conditions appear to have been very strong in the first half of this year, it seems likely that growth will ease into the second half of the year.

There are tentative signs that looser monetary policy is supporting the interest rate sensitive sectors of the economy, which is part of the reason I would recommending holding rates steady this month, but it is still a bit too early to see the full impact of the May and June rate cuts on the economy. Another month or two of data would help to clarify if monetary policy is loose enough yet.

Another month or two would also allow a better assessment of whether the recent falls in bulk commodity prices reflect genuinely weaker demand or are part of the usual seasonal easing in prices that occurs around this time. Inflation appears low enough to allow for further policy easing, if necessary, though further clarification that domestically produced (non-tradeables) inflation is easing would allow more consideration of further cuts. This information will not be available until late October.

Further out, I view that there is an equal probability that the cash rate will be static as 25 basis points (bp) lower than its current rate in six months time. Given downside risks to the global economy I think a lower cash rate than now is still more likely in six months time than a higher one.

Twelve months out, though, I view it as being almost as likely that rates are higher than now as that they are lower than now. If the economy gets through the next six months without a significant negative shock then the current looser monetary policy settings are likely to have provided enough support to mean demand is solid and inflation will start to lift.

Also see Paul’s six month and 12 month projections.

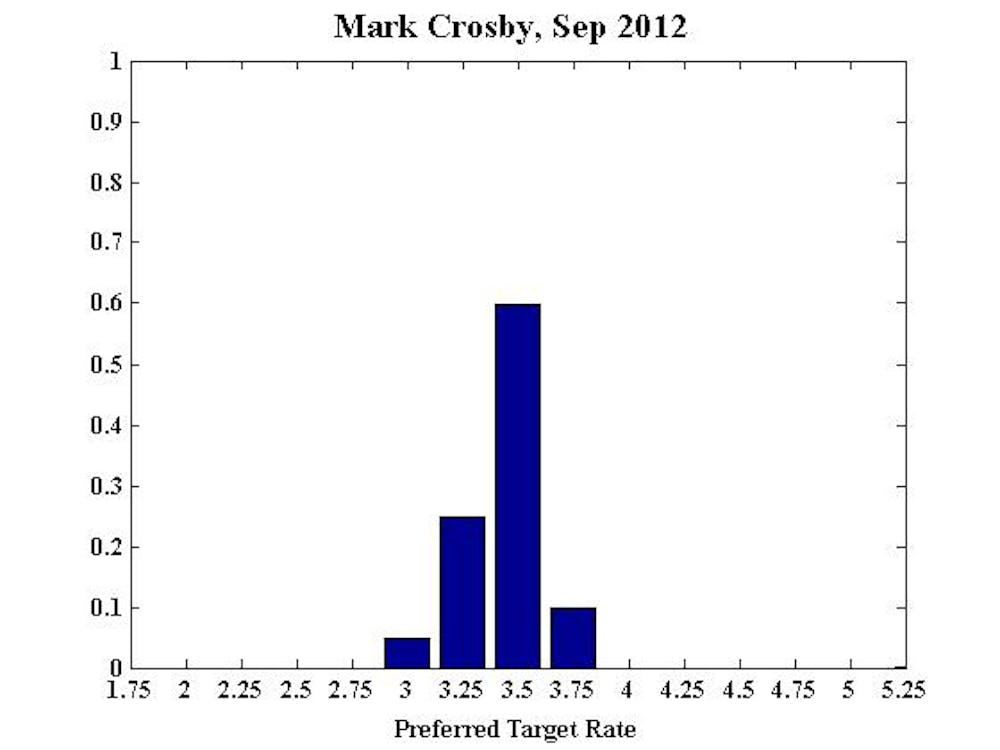

Mark Crosby, Dean of the Global MBA Program, Acting Dean of the Global BBA Program, and Professor of Economics, SP Jain Center of Management in Singapore:

While the odds are reasonable that Europe will continue to muddle through, it is more likely that issues with public debt will come to a head sooner rather than later. With this being the case central banks are likely to be loosening if they are able to do so in coming months.

Also see Mark’s six month and 12 month projections.

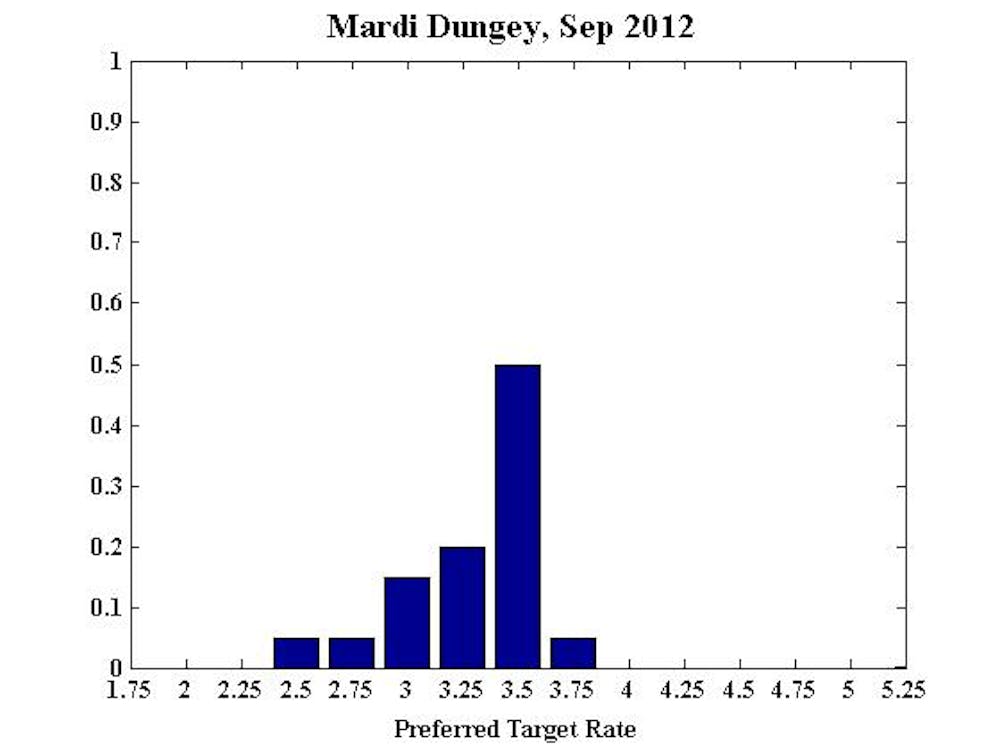

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA

Uncertainty as to the situation in Europe is likely to be pronounced this week, with the first of the post-northern-summer meetings to determine the next moves in the European sovereign debt crisis. Speculation of a Greek exit from the Euro is again rife, and although the most likely outcome is another patch-up, a serious disruption to international financial markets cannot be discounted. In this event, central banks around the world will likely stand ready to provide support.

In the light of the uncertainty over international financial conditions and international demand there is no reason to expect future improvements in demand for Australian exports, but continued strong portfolio support for the Australian dollar is likely to remain. I do not support fx intervention in this instance as I believe the strength of the currency reflects the reality of a relatively stronger Australian fundamentals and good credit rating compared with alternatives.

However, the stronger currency is impacting adversely on many aspects of the economy, and in a number of important sectors there is visible slowing. Monetary policy cannot directly redistribute resources between sectors, but it can influence the overall conditions. My overall recommendation is to remain stable this month, but with the risk on the downside, particularly in response to developments in international markets.

Also see Mardi’s six month and 12 month projections.

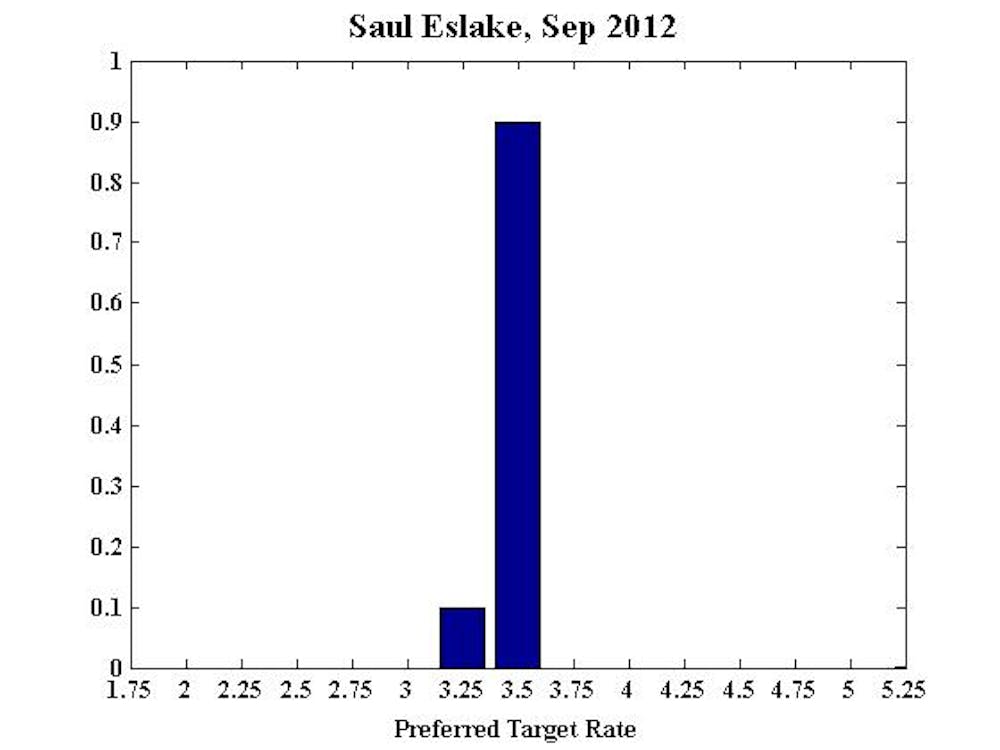

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia

Six months: most preferred outcome of -25 basis points (bp) reflects a view that the RBA should and will respond to what I expect to be an upwards drift in the unemployment rate over the remainder of this year. Small probabilities attached to -50 and -75bp are in recognition of the possibility of a negative ‘shock’ from Europe.

Twelve months: most preferred outcome of -25bp reflects a view that the RBA should and will respond to what I expect to be an upwards drift in the unemployment rate over the remainder of this year. Small probabilities attached to -50, -75bp or -100bp are in recognition of the possibility of a negative ‘shock’ from Europe or (after 1 January) the US.

Also see Saul’s six month and 12 month projections.

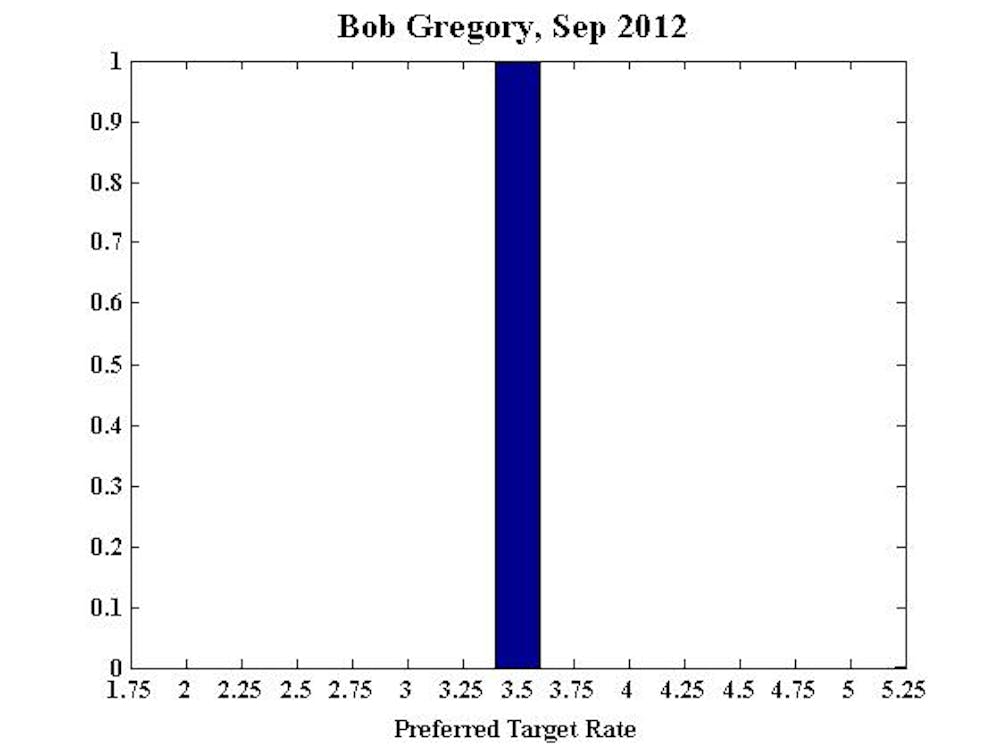

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology

No comment.

Also see Bob’s six month and 12 month projections.

Warwick McKibbin, Professor, RSE, ANU, CAMA

The rapid downturn in the terms of trade will take income and spending out of the Australian economy in coming quarters.

It is now unlikely that the RBA will need to raise rates in the near future to contain the positive terms of trade shock. There is also now considerably more downside risk to the economy if the government attempts to meet the promise of a fiscal surplus in 2012/13.

A surplus this financial year will now require even more substantial cuts to spending and/or increases in taxes just at a time when income growth is being slowed by falling export prices. It is hard to believe that a political promise would be more important than sound economic management but the risk of severe pro-cyclical fiscal policy cannot be ruled out over coming months.

This increases the downside risk to interest rates as the RBA steps in to prevent the economic slowdown that would result from a combination of negative terms of trade outlook accentuated by severe fiscal contraction. The problems in Europe are no better than last month and probably worse given the mounting fiscal liabilities and the lack of a concrete way forward.

There is a reasonable probability that Greece will exit the Euro zone by the end of the year thus the six month ahead prognosis for interest rates is difficult to predict but likely interest rates will be down across the yield curve.

In twelve months it is likely that inflation pressures will be widespread in emerging economies and central banks around the world will be raising rates to offset the monetary stimulus that is currently sloshing around global financial markets.

Also see Warwick’s six month and 12 month projections.

James Morley, Professor, University of New South Wales, CAMA:

Conditions remain balanced. Incoming data continue to suggest solid conditions for the domestic economy, with strong output growth and a low unemployment rate, yet little immediate inflationary pressures.

International conditions also provide no clear case for adjusting the target rate in either direction. Foreign demand is unlikely to boom in the near term. But even the small risk of another global financial crisis resulting from the ongoing problems in the Eurozone has diminished somewhat as the ECB has hinted at a more accommodative policy.

The near-term focus of monetary policy should be on responding to surprise developments for inflation, including cutting the policy rate if inflation remains persistently below the target range.

Also see James’ six month and 12 month projections.

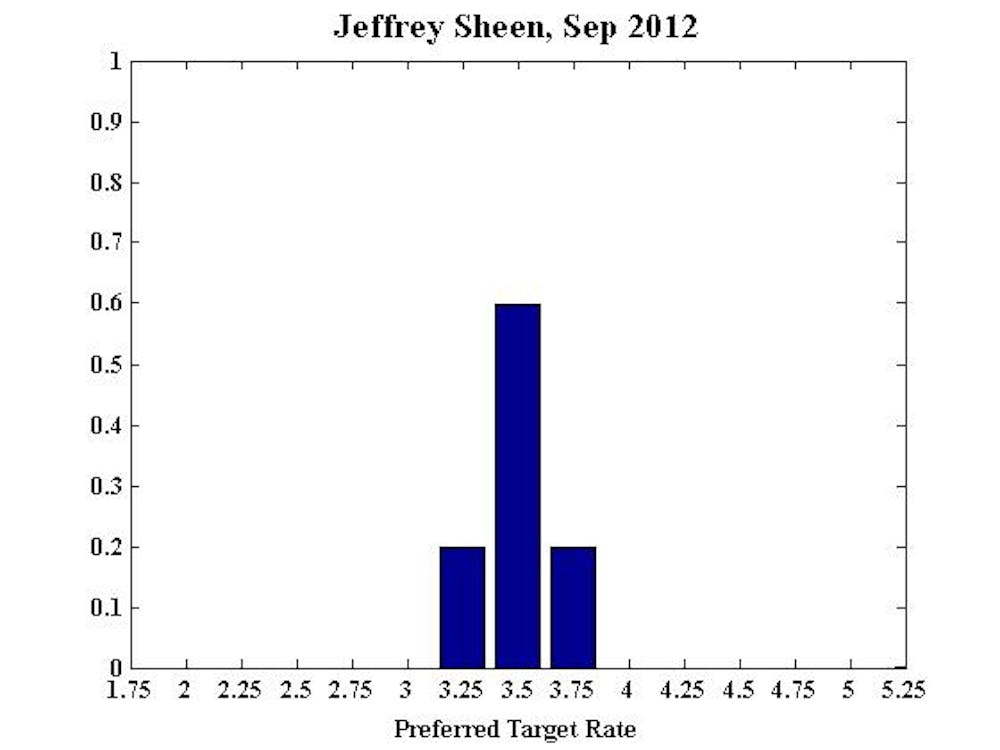

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

My recommendations have been marginally adjusted down because current and expected capital expenditure of all types have significantly declined in non-mining sectors.

Also see Jeffrey’s six month and 12 month projections.

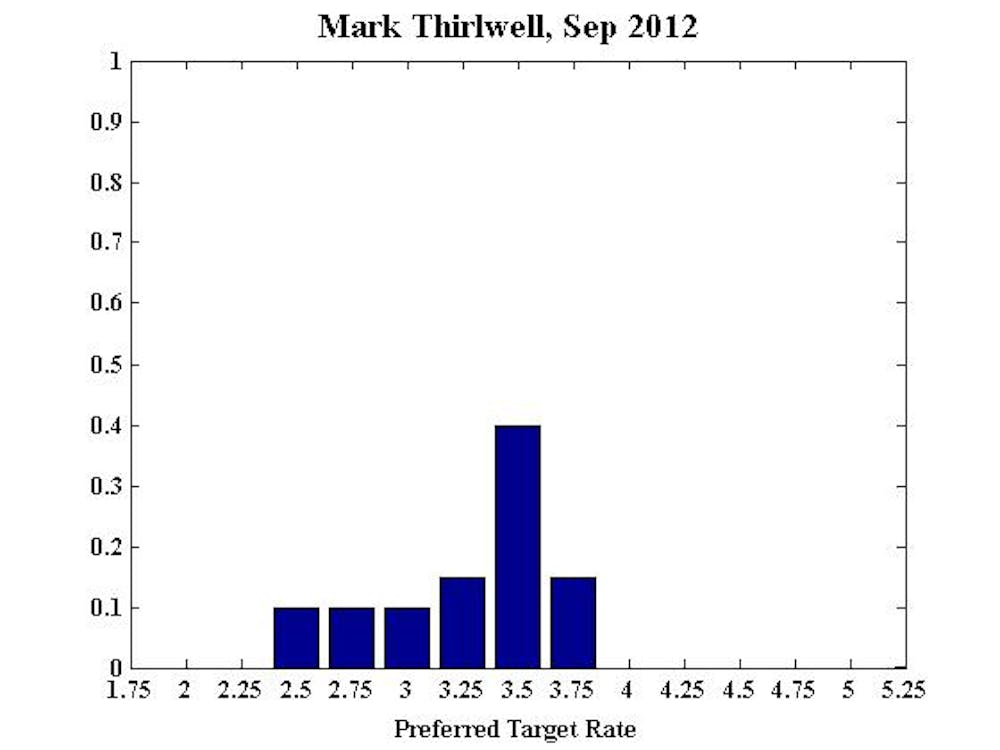

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy

No comment.