Inflation is rising again in the UK, according to the Office for National Statistics. Prices in March rose 0.7% compared to a year earlier, against a 0.4% rise in February. One of the main drivers was that fuel prices have seen their biggest increase since January 2020.

This rise in inflation is roughly in line with what analysts were expecting. The Bank of England has been expecting inflation to rise this spring as well, but thinks it will then settle down.

In my view, inflation will go much further than the Bank expects. The twin policies of creating new money, known as quantitative easing (QE), and extra government borrowing to pay for COVID support measures could lead to prices surging in the months ahead – with unsettling implications for the UK economy’s recovery from the pandemic.

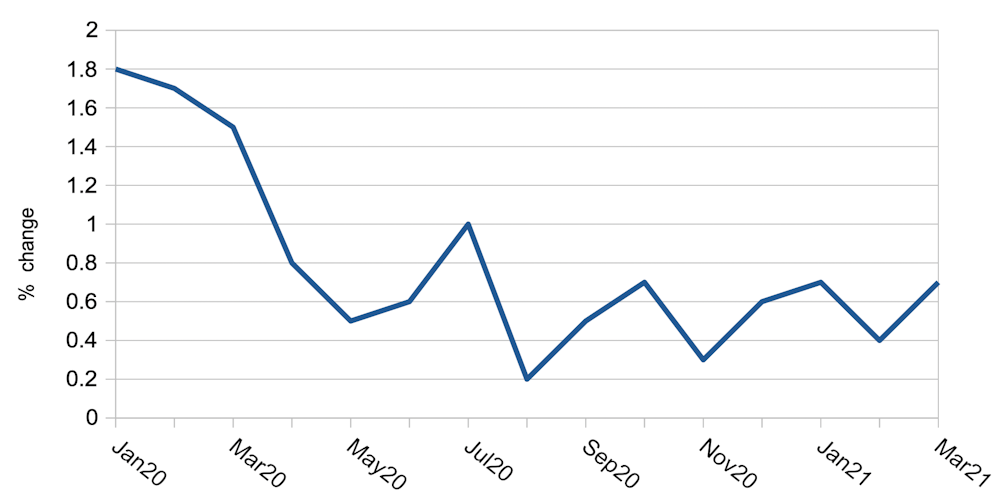

The Bank has a duty to maintain consumer price inflation at 2%. Inflation measures how much prices for goods and services are rising – or the rate at which the pound is falling in purchasing power, therefore making goods more expensive. Since the pandemic began, inflation has undershot this target, as you can see from the graph below.

UK annual inflation 2020-21

To understand where inflation might go next, it helps to compare the responses by the authorities to the pandemic and the financial crisis of 2007-09. After the financial crisis, the Bank of England and other central banks used QE to increase the amount of money in the economy (also known as the monetary base). They did this by using digitally created money to buy mostly short-term government bonds from investors such as banks and pension funds.

The aim was to stimulate growth and recovery, since increased demand for bonds pushes interest rates down and encourages people to borrow and to put more money into riskier assets like the stock market. The UK monetary base grew fourfold, but only in the broadest sense of money that includes things like pension funds and large bank deposits that can’t be accessed for a long period of time. On the other hand, the most common measure of money in the economy, M2, which is mainly cash and bank deposits, remained flat.

The reason for this difference is that much of the QE money ended up on bank balance sheets to shore up the amount of capital they have to protect themselves from bad debts and periods like 2007-09 when money does not circulate properly. In other words, the banks didn’t lend much of the money to businesses and consumers so it didn’t reach the wider economy. This is why a fourfold expansion in money produced little inflation.

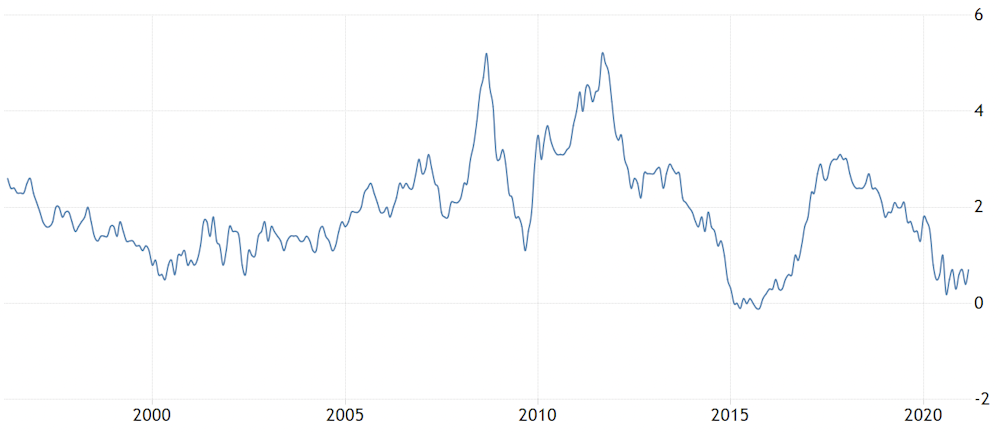

UK inflation 1996-2021

At the time of this programme, the government was cutting back spending to try and bring its deficit down. During the pandemic, it has been doing the opposite: raising money by issuing bonds to pay for the COVID furlough scheme and the various other support measures.

The Bank has been running its latest QE programme in tandem, potentially taking it to £895 billion by the end of the year. This has kept interest rates low, which has enabled the government to borrow more cheaply.

Because of this monetary (central bank) and fiscal (government) stimulus, the effect on the money supply has been different. I estimate that the total monetary base has grown 50% since March 2020, while M2 has grown by around 25%. This should create much more inflationary pressure than after 2007-09.

How high?

Like in the 2010s, today some of the extra money has been spent on speculative investments like the stock market – if speculative asset prices were included in CPI, it would be well over 2% already. But the rest is being sat on by businesses and consumers, waiting for the COVID restrictions to be lifted. Of particular risk to prices is that this pent-up money leads to excessive demand before the supply of goods and services has returned to pre-pandemic levels.

The Bank thinks it most likely that the pent-up demand will increase inflation to nearer 2% over the spring, and broadly keep it there into 2022 and 2023. However, its projections are actually much more uncertain than usual, despite claiming inflation is “well anchored”.

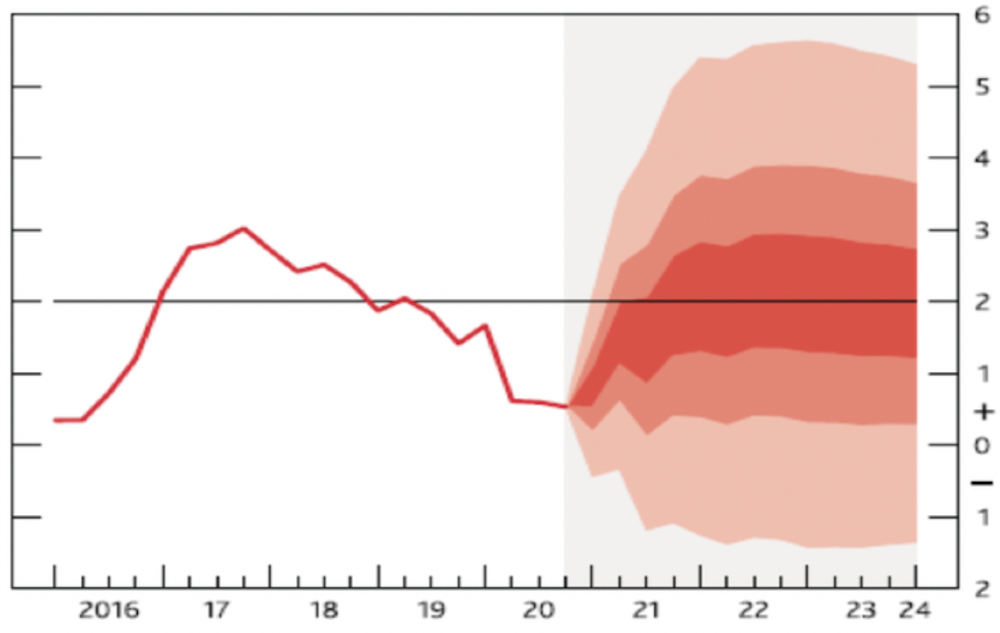

When you look at the Bank’s more detailed projections, it sees a one in three chance of inflation below zero or above 4% over the next couple of years – in other words, it simply doesn’t know. You can see this in the fan graph below, which displays the central projection in the darkest shade and the least likely in the lightest.

Bank of England inflation forecasts

The Bank’s outgoing chief economist, Andy Haldane, has said that QE has left the UK and other countries in “deep and uncharted waters”. Haldane believes the long-term effects of the pandemic recession are likely to be towards the top end of expectations. If so, the Bank’s inflation forecasts are likely to be too low.

Economists, and more specifically monetarists, fear that the Bank is underestimating the effects of inflation. These people are likely to be correct, since increasing M2 has always led to inflationary pressure in the past.

It may be a fool’s errand to predict future inflation, but there is genuine reason to believe it could surge past its 2% target to rise beyond 4% by the second half of 2022. By then, the government may be helping to curb it by reining in spending and raising taxes, both of which would reduce the money supply.

But mainly it would fall to the Bank to raise interest rates to stop consumers from spending to the same extent (while presumably also insisting the extra inflation was outwith its control and not due to QE or the fiscal stimulus). This would cause economic contraction and cause businesses and consumers to struggle with debts that are already at very high levels.

In other words, we could be looking at an old-fashioned boom and bust phase of expansion and contraction within the next 18 months, and more challenging times ahead as a result. Much may depend on coronavirus in Europe and whether a new wave arrives, since this could potentially choke off the recovery and keep inflation under wraps.