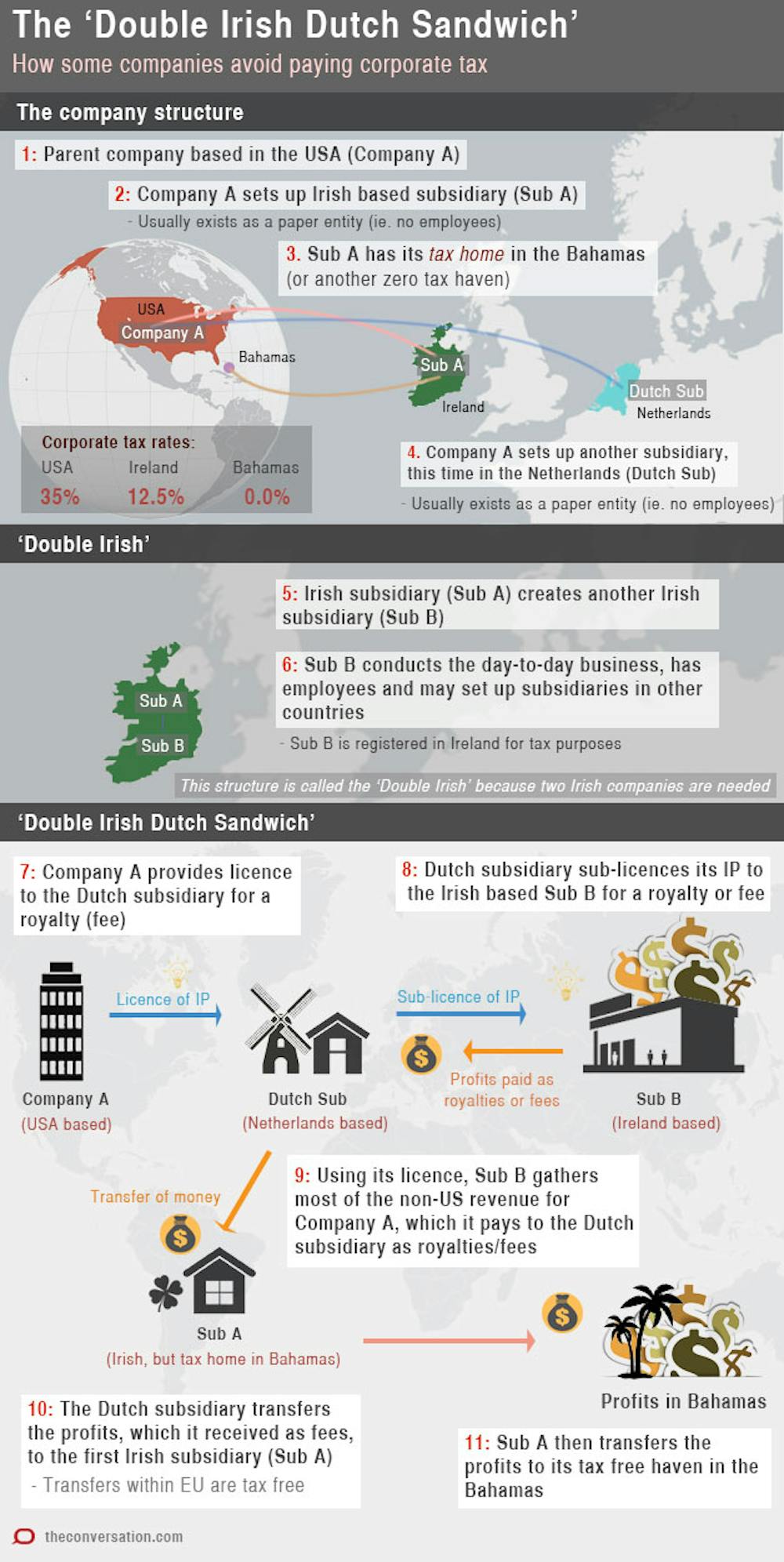

Ireland has this week moved to change its tax law, closing the “double Irish” tax avoidance technique widely used by multinational enterprises including Google and Microsoft.

In very broad terms, the current Irish tax law allows a company incorporated in Ireland to be a tax resident of another country, typically a tax haven. It works as the perfect complement of the US tax law, as a subsidiary of a US multinational incorporated in Ireland can avoid taxation in both the US and Ireland.

Ireland’s Treasurer Michael Noonan claimed in the Budget speech that the corporate residency rule would be changed “to require all companies registered in Ireland to … be tax resident” of the country. The detailed legislation to implement the new rule will not been known until the government introduces its 2014 Finance Bill. However, based on available information, there are at least two catches.

Loopholes remain

First, existing companies incorporated in Ireland will enjoy a long “grandfather” period. In particular, the new rule will not be applicable to these companies – including the Irish subsidiaries of Google and Microsoft – until 2021. The long time lag provides ample opportunities for multinationals to respond and restructure their tax avoidance transactions.

Second, the devil may be in the detail. The Budget is accompanied by a document published by the Irish Treasury, titled: “Competing in a Changing World: A Road Map for Ireland’s Tax Competitiveness.” According to the document, the proposed new rule will be introduced as a “default” corporate tax residence rule. In the tax world, a default rule means there will be alternative rules, or the default rule will be subject to exceptions and/or exclusions. The actual effect of the new rule will remain a mystery until the detailed provisions of the new rule are released.

The proposed change to close the “double Irish” loophole brings a feeling of déjà vu. Ireland has made similar moves in the past when international anger over its tax law became too much to bear.

Before 1999, Ireland had no statutory definition of corporate residence in its tax law. This has led to an international perception of Ireland as a tax haven. In response, the country enacted a statutory definition of corporate residence in 1999 and adopted the incorporation test. However, the definition incorporates a couple of easy escape routes for multinationals. In practice a subsidiary of a US multinational that is incorporated in Ireland will find it embarrassingly easy to avoid being regarded as an Irish resident.

Ireland reacted to international pressure again in 2013, when it amended its definition of corporate residence by inserting a provision to address the issue of “stateless” companies, which refer to companies that are not residents of any country. This change was designed specifically to target Apple’s Irish subsidiaries, and will not apply until 2015. These companies were not tax residents of any country in the world, thanks to the perfectly complementary definitions of corporate residence in Ireland and the US.

However, the scope of this provision is so limited that it does not affect the more common structure of “double Irish Dutch sandwich” adopted by many US multinationals including Google and Microsoft.

Ireland’s primary tax policy driver

The “Road Map for Ireland’s Tax Competitiveness” document says much about the country’s primary tax policy objective. The document reaffirms the determination of Ireland “to become the country of choice for mobile foreign direct investment in a post-BEPS environment”.

BEPS, or Base Erosion and Profit Shifting, is a current target for both the OECD, and the G20 leaders.

Ireland’s plan to continue to facilitate tax avoidance is readily apparent in Noonan’s Budge speech. He claimed that:

“For over 60 years, foreign direct investment has been a cornerstone of Ireland’s economic development … Our competitive corporate tax system plays a key role.”

Noonan was quite eager to emphasise in his speech that the new rule of corporate tax residency “will not bring an end to international tax planning”.

Tax law needs a paradigm shift

Even if the new rule in Ireland will effectively close the “double Irish” loophole, the army of thousands of highly intelligent tax advisers will work diligently to explore other loopholes. This exercise may become a bit more difficult, but definitely far from impossible. This will remain so until the tax law undergoes a paradigm shift.

Tax law should be able to look through intra-group tax avoidance transactions, and to treat a corporate group as one single enterprise. A recent tax case in Australia illustrates this issue well.

The Chevron case basically involved an Australian company (“Chevron Australia”) which borrowed from its own wholly-owned subsidiary incorporated in the US (“Chevron CFC”) at 9% interest rate. Chevron CFC has no other business. It is a special purpose vehicle established solely for the intra-group loan structure.

Chevron Australia is a wholly-owned subsidiary of its parent company in the US (“Chevron US”). Chevron US can borrow at a rate of 1.2%. This is precisely the rate that Chevron CFC borrows from third parties, because of a guarantee provided by Chevron US.

The substantial interest margin paid by Chevron Australia effectively eroded the tax base in Australia. The arguments of this case involved highly complex and technical tax rules, and the court decision will not be known for a while.

However, this case highlights a critical issue. Why should the tax law in the first place allow a group company to be charged interest at 9% when the group as a whole can borrow at 1.2%?

The current tax law arguably is detached from the economic reality that a group in practice operates as one single enterprise. Tax authorities, as a result, are in general bounded to respect intra-group transactions, despite the fact that they do not represent genuine shifts of economic risk outside the group.

Until the tax law in general empowers tax authorities to look through intra-group tax avoidance transactions, the war on BEPS is likely to be in the favour of multinationals.