Any government rules out tax rises at its peril, but elections have to be won and so Britain has plumped for a commitment that income tax, national insurance and VAT sales tax will remain unmolested for the next five years. Any government, however, also wants to boost its revenues. The fear is that we will see yet another under-the-radar raid on savings and pensions which leaves people struggling to understand how they are affected.

Hidden in the wings of the new government’s financial plans are measures that should put savers on alert. The first is a major change to the taxation of dividends from April 2016 that is expected to yield the government around £2 billion a year. Given only a fleeting mention in George Osborne’s budget speech, it mainly targets small business owners but could also affect up to 4m UK households that invest directly in shares or indirectly through investment funds, though only those with large investment portfolios will see their tax bill rise for now.

Dividend and rule

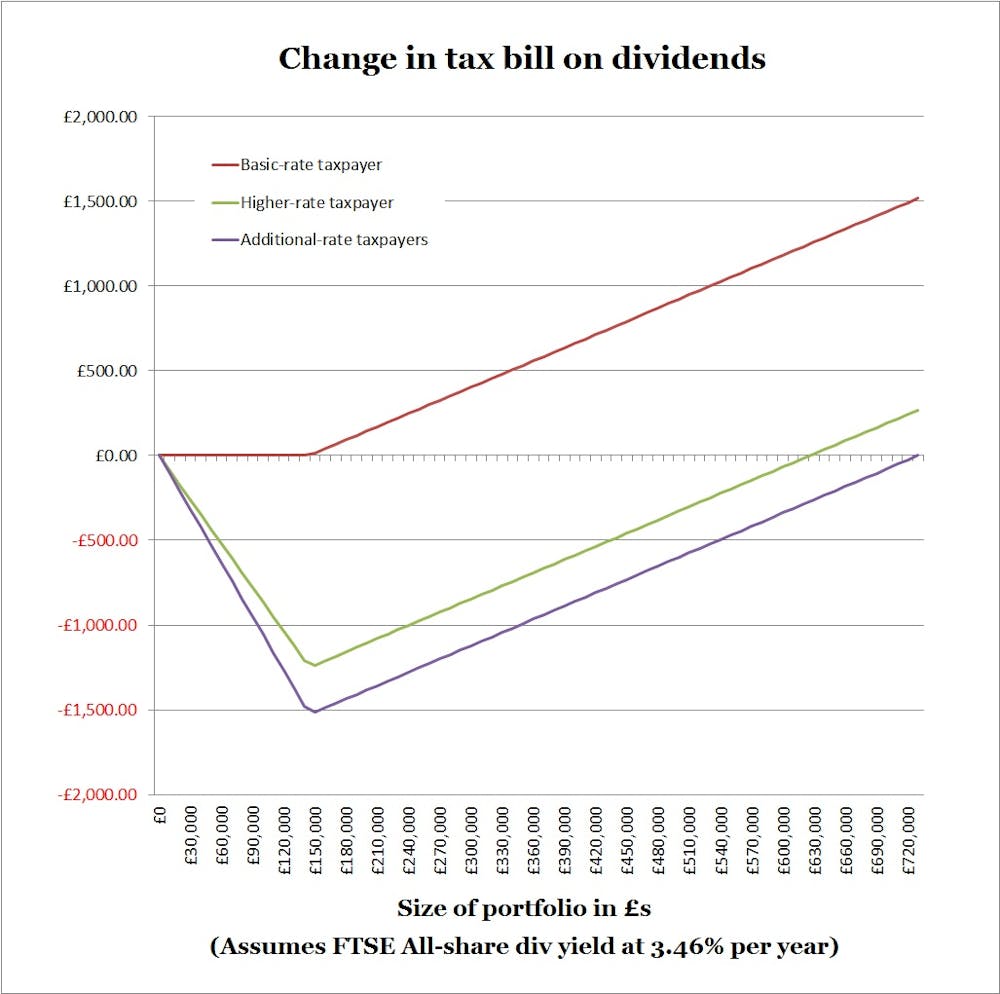

Dividends are the part of a company’s profits that it pays out to its shareholders. The company has already paid tax on the profits and the dividend comes with a tax credit in recognition of that. Basic rate taxpayers pay nothing more under current rules; higher rate taxpayers pay 25% of the dividends received; and additional rate taxpayers – those are the people paying 45 pence in the pound – 30.6%.

But from April 2016 that will change. The tax credit will be abolished and a new Dividend Tax Allowance of £5,000 will be introduced. But when your dividend income heads above that amount, basic-rate taxpayers will pay tax at 7.5%, higher-rate taxpayers 32.5% and additional-rate taxpayers 38.1%.

As the chart below shows, the impact is mixed. Some people in the top two tax brackets will pay less tax because of the new £5,000 allowance. However, the changes amount to a significant tax hike for basic-rate taxpayers with portfolios above around £140,000 and other taxpayers with very large portfolios. Anyone affected by these changes should look carefully at shifting savings into tax-efficient Individual Savings Accounts (ISAs) and pension schemes, if they can, since these are unaffected by the change.

This shift in the way dividends are taxed is a marked departure from the principle of not taxing the same income twice and creates the tempting opportunity for the government to cut the Dividend Tax Allowance or increase the new tax rates in future without breaching that new “triple lock” which applies only to a narrow range of main tax rates.

Pension tax relief

The government has long given tax reliefs designed to encourage you to save for retirement. These include tax relief on money you pay into your pension and on gains and most income made through your pension investments. Once you decide to retire, you can also withdraw a quarter of your savings tax-free, but the rest (whether drawn as pension or lump sums) is taxable. This system is sometimes described at EET, meaning the stages are: Exempt, Exempt, Taxed.

Since April 2015, many savers have complete freedom to draw out their pension savings from age 55 onwards and use them for any purpose (including Lamborghinis). Many pension experts have been questioning whether tax incentives make sense when the requirement to use the savings for retirement has gone. So, perhaps unsurprisingly, alongside the summer budget, the government issued a consultation paper floating ideas for different ways to treat pension tax reliefs, on the grounds of “strengthening the incentive to save”.

The main suggestion is that pensions could be taxed like ISA savings products. This would mean abolishing contribution tax relief, but still allowing the pension pot to build up largely tax-free and charging no tax on any withdrawals. This system could be characterised as TEE using the same system as before.

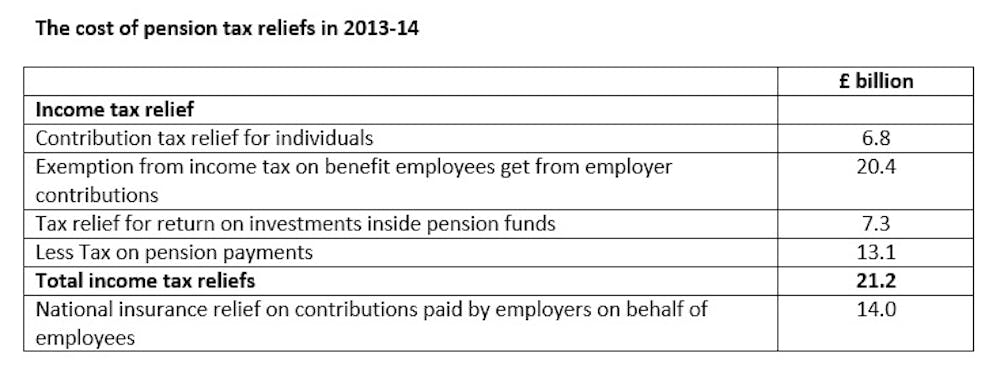

The table reveals a couple of reasons why a government might be interested in such a change. First, the amount paid out in income tax reliefs on contributions would be more than double the tax recouped on pensions currently. Second, a shift to a TEE system would reduce government spending now, even though there would be a fall in tax revenues many years later. That could clearly be attractive to a government struggling to make budget cuts today.

Savers, however, would lose out. This is partly because many will have a lower top tax rate in retirement and so will save less tax than they lose in contribution tax relief. The current system also provides extra help for savers on low incomes by giving contribution tax relief at the basic rate even to non-taxpayers. Less obviously, savers would lose because a switch to the TEE system removes the quarter of the savings that currently gets tax relief on the way in, as well as being tax-free on the way out.

There are good reasons to strengthen incentives to save for retirement, to simplify the system of pension tax reliefs and to ensure that tax reliefs are distributed fairly. It is to be hoped that the consultation will genuinely keep these aims at the forefront and resist the opportunity simply to make a tax raid.

The change to dividend taxation and proposals for pension tax reliefs demonstrate how a government that publicly stands for lower taxation can nonetheless find ingenious ways to raise extra tax revenues. Raising taxes is to be welcomed if it reduces the scale of cuts to benefits and public services, but tax increases need to be made openly and honestly with full debate about who is affected and how, not hidden in a cloak of political grandstanding.