With oil prices on the slide, members of the once-dominant Organization of the Petroleum Exporting Countries (OPEC) decided last week not to attempt to rally them by cutting production, leaving the Brent Crude price hovering at about US$70 (A$83) per barrel.

A curious decision, perhaps, by a 12-nation bloc that has previously kept an iron grip on the world’s oil trade. But not so curious when you consider that OPEC is no longer an all-powerful cartel – now it has plenty of competition.

For the first time since its formation in 1960, two of the top three oil-producing countries (the United States and Russia) are outside OPEC. While OPEC controls low-cost oil, it has lost supply control at higher prices and cannot push prices up like it could in the 1970s – or at least, not without stimulating a lot more supply from elsewhere.

According to the US Energy Information Agency, the United States now produces 11.1 million barrels of oil per day – about the same as Saudi Arabia (11.7 million barrels) and Russia (10.4 million barrels).

This new situation is a free-for-all between the three major players: OPEC (led by Saudi Arabia), US-based private oil companies, and Russian state-controlled oil firms. All three groups have the same reason for wanting to produce more – they need or want more money in the short-medium term to satisfy their current spending, shareholder and salary expectations. Amid this competition, cutting production on purpose isn’t such an attractive move.

Price plunge

The drop in oil prices over the past year is the result of years of over-investment in oil production. Companies and governments, expecting sustained high prices, have made investment decisions at break-even prices of US$60-80 a barrel and above. With oil prices over the past decade averaging more than US$100 a barrel, even a US$80 break-even sounds conservative, especially for projects with a quick return.

But the sustained high prices had another effect: they encouraged the development of new technologies such as deep and ultra-deep water oil drilling, and the recovery of shale oil through improved horizontal drilling and fracking. These technologies have been advanced due to high prices, but ironically, once deployed they drive the price down again as more supply comes online.

A good example is the Bakken Formation in the US state of North Dakota. Discovered in the 1950s and estimated to hold more than 200 billion barrels of shale oil, it became a very attractive prospect at US$100 a barrel. With US$20 trillion in untapped oil, there was a strong incentive to develop the technology to extract it, which is happening now.

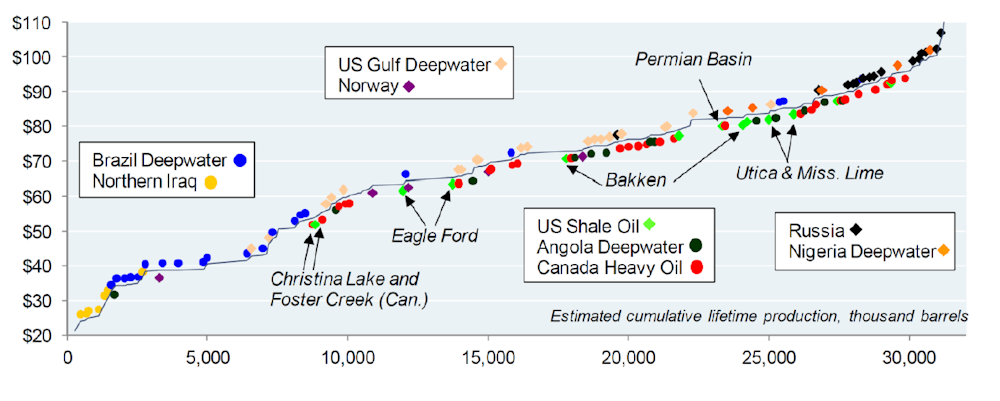

Over the past decade, oil companies have invested trillions of dollars in new projects based on high oil price assumptions, in ever more remote locations and with consequently higher production costs. There are now deep-water oil projects in the Black Sea off Romania, and off Brazil’s coast, and oil sands projects in Canada.

Oil firm McMoRan spent US$1.2 billion to drill six wells in ultra-deep waters in the Gulf of Mexico – US$200m per well. At US$70 a barrel, it would take more than 17 million barrels (nearly an entire day of US demand) to recover the cost of drilling these wells. Once oil is found and under production, the tap is not going to be turned off until the cost of marginal production is greater than the oil price.

Multiply this by oil basins all around the world (see below), and all of this sunk capital needs to generate a return on investment, even if less profitable. Given that the extra cost of producing oil from these unconventional assets is US$10-20 barrel, oil companies are putting these assets to work as hard and as fast as the reservoir allows. This improves their cashflows in the short term, but reduces their return on investment and profitability. These financial issues will reveal themselves more over time.

You would think that global population growth would drive prices higher, but high energy costs and concern for the environment has also driven improvements in energy efficiency, especially for planes and cars. Even with the rise of the middle class in China, global oil consumption has actually gone down relative to population growth over the past decade (global population has grown by 11.3% while oil demand has increased by 9.3%).

Car use has also peaked in most countries around the world as commuter speeds have hit the wall due to higher populations and workers gravitate back to dense urban centres. This is causing a massive amount of passenger rail to be installed around the world. China has installed 8,500 km of intercity fast rail and 86 metro systems in cities in the past decade. These are all powered by electricity rather than oil.

Electric performance

High-cost assets may continue to produce at current oil prices, but there will come a point if they decline further where they become unviable to continue producing. Oil-based transport assets are at a greater risk of becoming stranded.

Given that 97% of oil production is used for transport, and the majority of this is for passenger and commercial vehicles, oil demand could fall significantly as people choose to drive lower-emission vehicles.

Of the 18 million barrels per day used in the United States, 9.7 million barrels is for vehicle transport. Extrapolating that globally means that for every 10% of petrol cars that are replaced with electric ones, global oil demand would drop by more than 5%.

Improvements to car efficiency would have a similar effect, with a 10% improvement in overall average vehicle efficiency causing a 5% drop in oil demand.

At US$70 a barrel, this 5% reduction in annual oil demand would wipe US$116 billion off annual global oil sales.

By 2020, hybrid and electric vehicles are expected to account for more than 5% of the global new car market. The United States has more than 240,000 electric vehicles (a small but fast-growing fraction of the 250 million US cars in total), and in Norway, the world leader in electric vehicles per capita, 12.9% of new cars sold in the first half of 2014 were electric.

Where does this leave OPEC?

OPEC members know that cutting their own production would no longer have a big effect on the global supply of oil. Even if they could drive up the oil price, this would only invite more competition that would hurt their revenue, by making expensive projects such as Canadian oil sands more viable.

OPEC also knows that private oil firms won’t be scaling back production either. After more than a decade of high-cost investments, it’s in the private players’ interests to keep working existing assets to claw back capital. Cash flow at a lower oil price is better than no cash flow at all.

Given these assets have a typical life span of at least 10 years, this situation is likely to endure for some time. We have probably seen a step change in oil prices, which are likely to stay low.

This is why it’s off the mark to suggest that OPEC has deliberately chosen to keep the price low to compete with renewable energy. The far less sinister reality is that OPEC no longer has much choice at all.

This article was amended on December 4, 2014, to correct an error in the amount of oil production required to recover the cost of McMoRan’s oil drilling in the Gulf of Mexico. Thanks to Terry Reynolds in the comments for spotting it.