The Shadow Reserve Board, an initiative of the Centre for Applied Macroeconomic Analysis (CAMA) made up of eminent industry and academic economists, returns this month.

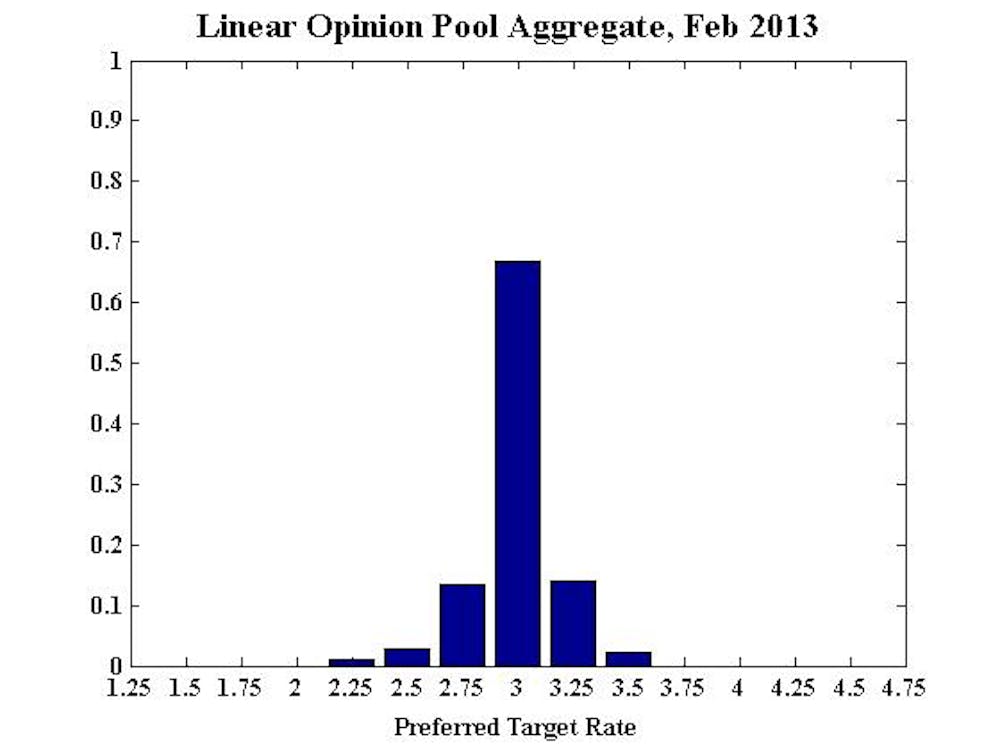

Reserve Bank of Australia board members should leave the cash rate unchanged at 3% tomorrow. But a persistently high Australian dollar and climbing unemployment could see rates trending upward in the next six to 12 months.

The Shadow Board assessed the probability that rates should be higher in six months at around 1/3, approximately balanced by the risk that rates should be lower.

In contrast, the nine experts on the Shadow Board assessed the probability that rates should increase over the next twelve months at over ½, with just under 1/3 probability that rates should fall.

Although there is greater uncertainty about interest rates in the longer term, the balance of risks has shifted towards higher rates in the future.

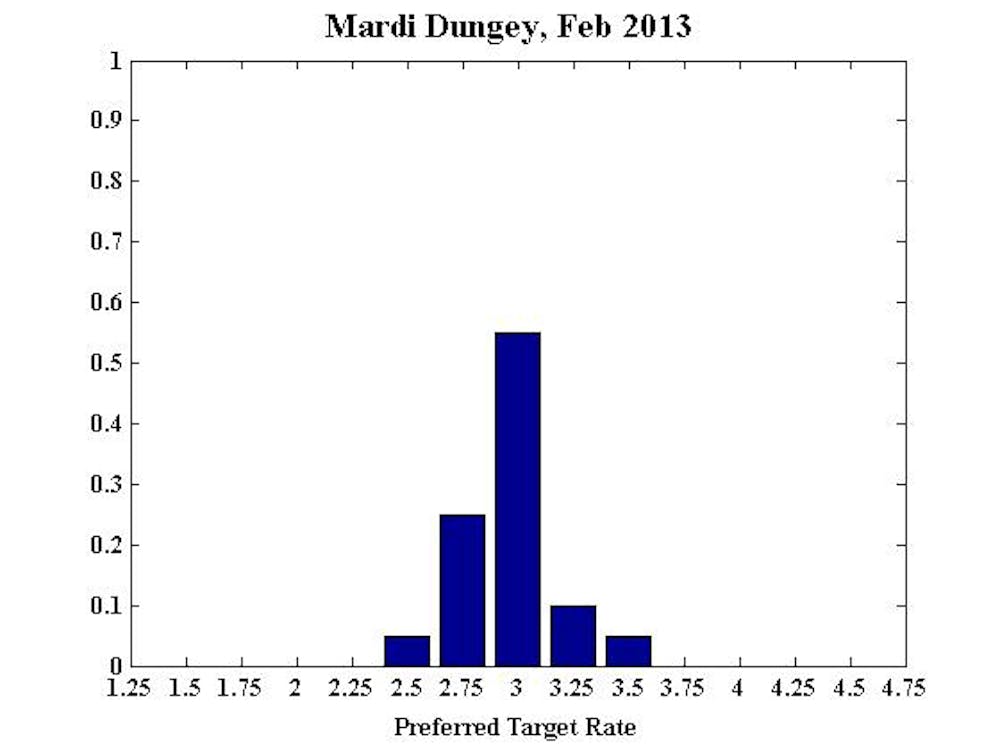

University of Tasmania Professor Mardi Dungey noted that “the blunt instrument of monetary policy will not achieve redistribution between areas which are doing better than others”.

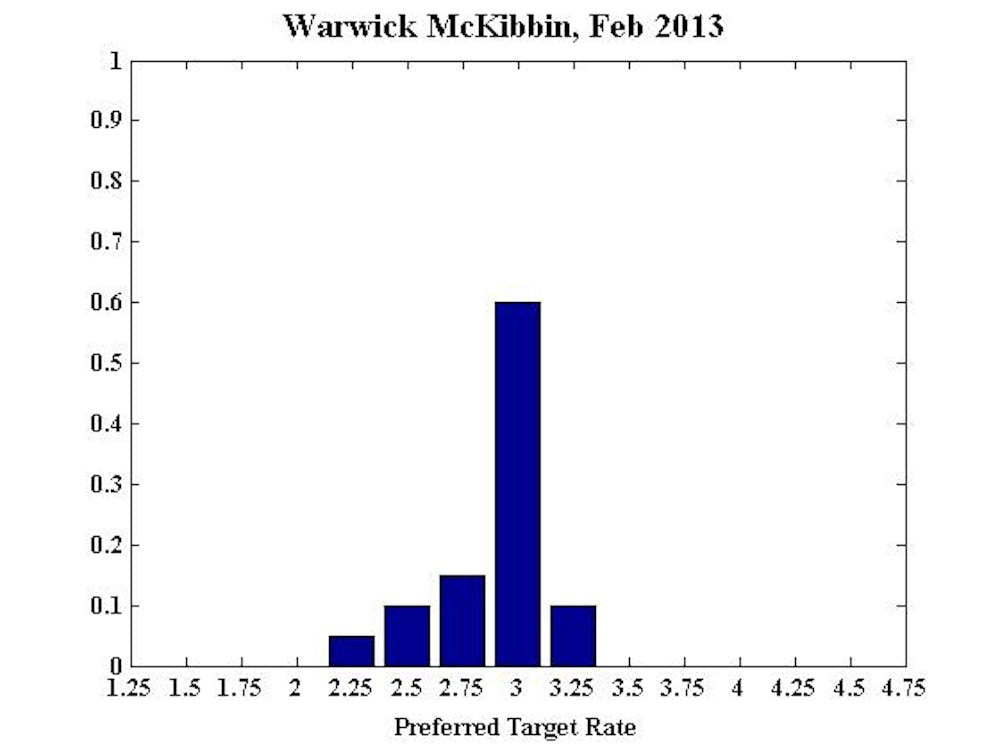

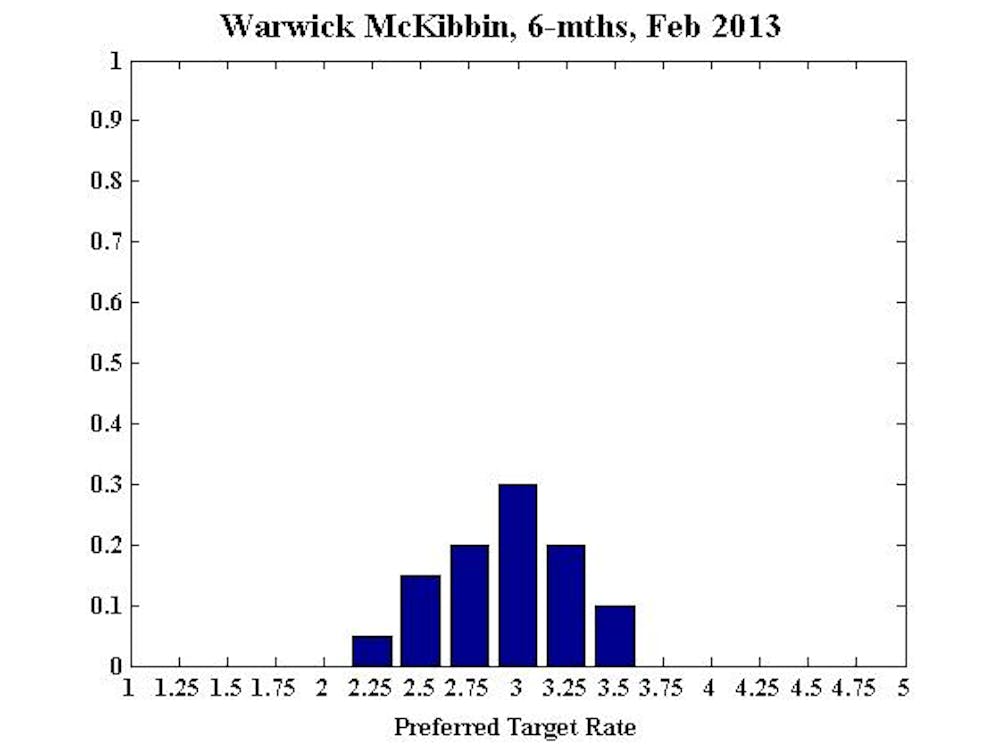

ANU Professor Warwick McKibbin said holding interest rates too low risked “distorting the allocation of capital towards more speculative investments that eventually cause a problem during an unwinding of the policy”.

He argues:

The task of adapting to the changing nature of the commodities boom should be a combination of increased flexibility in the economy, particularly labor markets, to allow the private sector to adjust and a gearing up of government infrastructure spending at historically low costs of borrowing in order to facilitate private sector investments to emerge over time.

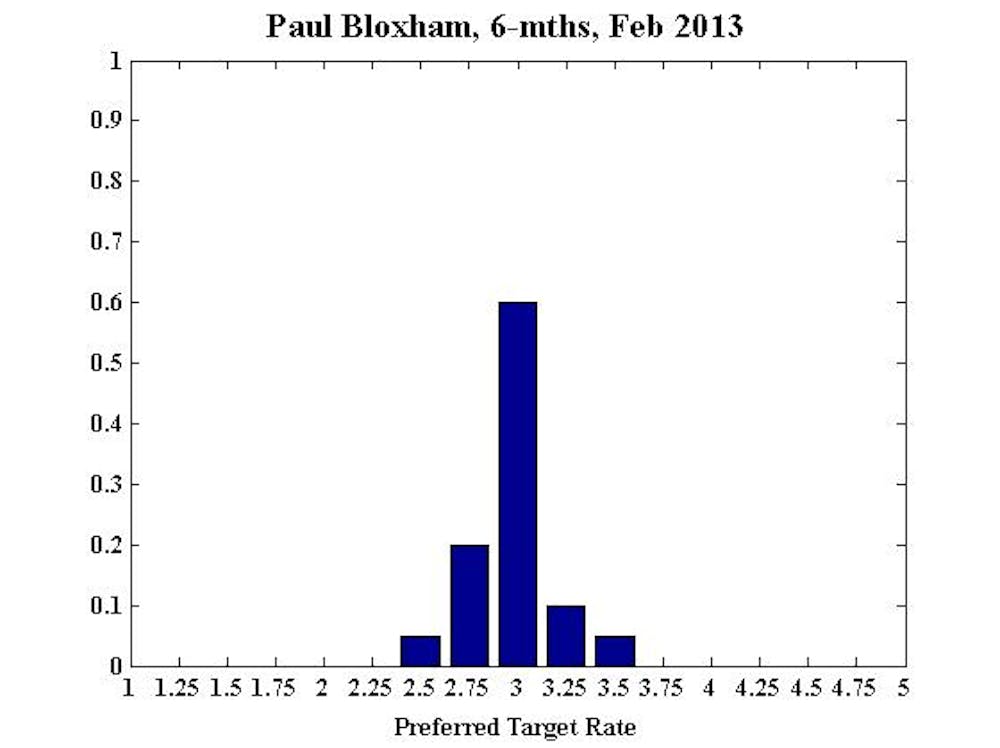

However, HSBC economist Paul Bloxham said “very timely indicators of conditions suggest that monetary policy is working, with consumer sentiment rising in recent weeks and housing prices also edging upwards”.

Paul Bloxham, Chief Economist (Australia and New Zealand), HSBC Bank Australia Ltd:

Since the last meeting there has been a distinct improvement in financial market sentiment, largely reflecting improved global conditions. A number of the key global down-side risks to growth have been reduced, with the US fiscal cliff issue having been somewhat resolved and markets no longer pricing a significant risk of a break-up of the euro.

Global monetary policy has loosened further, with Japan extending its quantitative easing programme and adopting an inflation target. Most importantly for Australia, the economic upswing in China has gathered further momentum and industrial commodity prices have risen solidly as a result.

Locally, much of the official data have been on the weaker side, but, critically, they almost all pre-date the RBA’s last cut and certainly pre-date its impact. Very timely indicators of conditions suggest that monetary policy is working, with consumer sentiment rising in recent weeks and housing prices also edging upwards.

The government’s pre-Christmas announcement, that it is no longer committed to pursuing a budget surplus in 2012/13, also means that fiscal policy is likely to be looser than the board had previously anticipated.

While inflation remains well contained for the moment, local monetary and fiscal policy settings and the global environment are already conducive for a pick up in Australian growth. I recommend the cash rate is held steady at 3.00%.

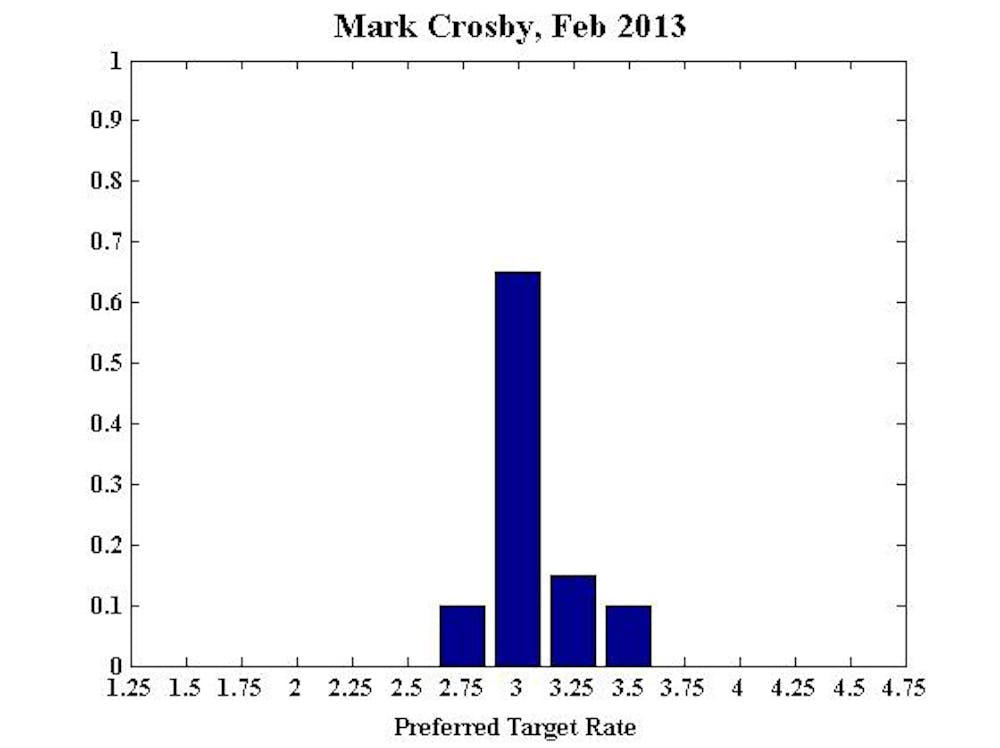

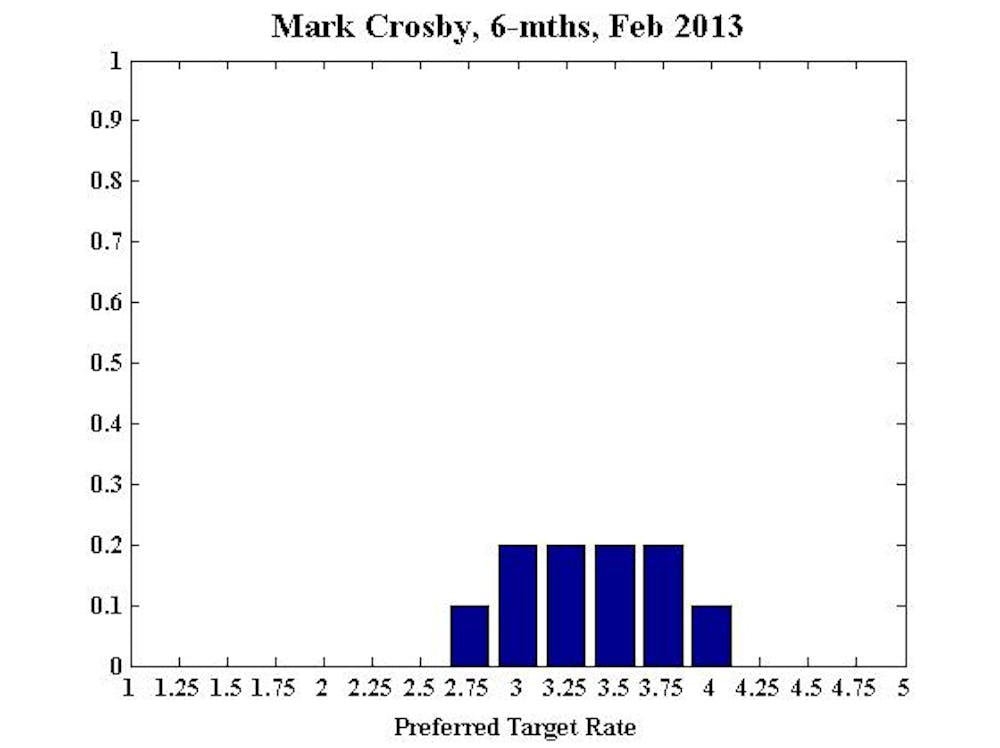

Mark Crosby, Dean of the Global MBA Program, Acting Dean of the Global BBA Program, and Professor of Economics, S P Jain Center of Management in Singapore:

No comment.

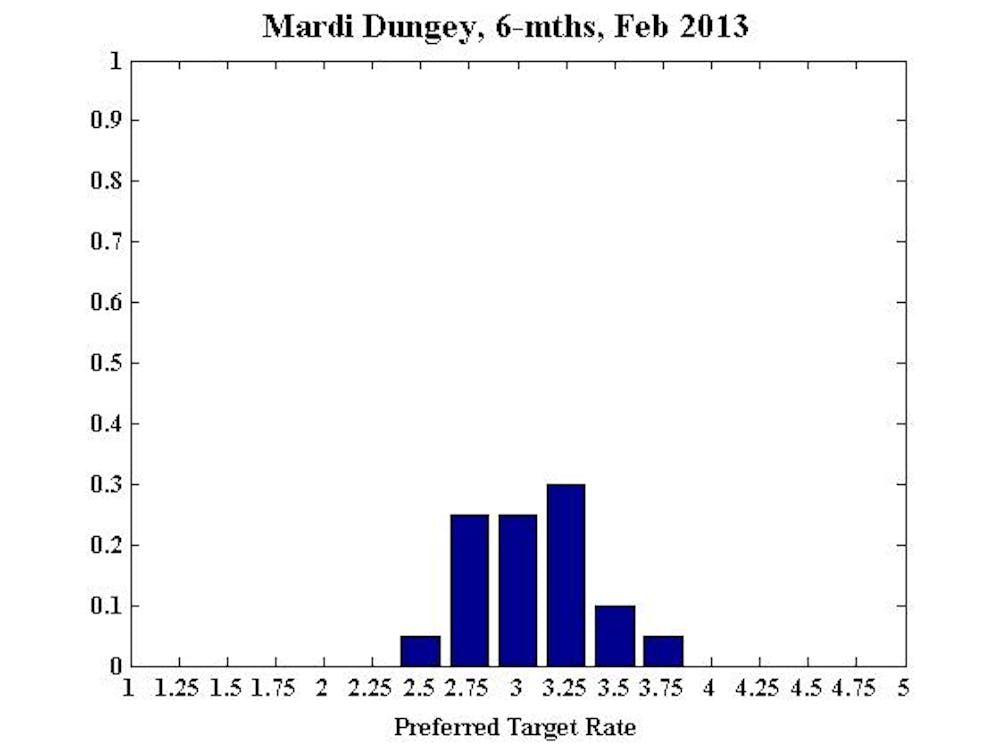

Mardi Dungey, Professor, University of Tasmania, CFAP University of Cambridge, CAMA

The domestic economy remains weaker than desirable. However, the economy does not appear to be in immediate danger of a recession. The blunt instrument of monetary policy will not achieve redistribution between areas which are doing better than others. It is important that the economy retains some room to move interest rates downwards in the future, and retains positive real interest rates at this stage. Thus my recommendation is that the policy stance remains unchanged this month.

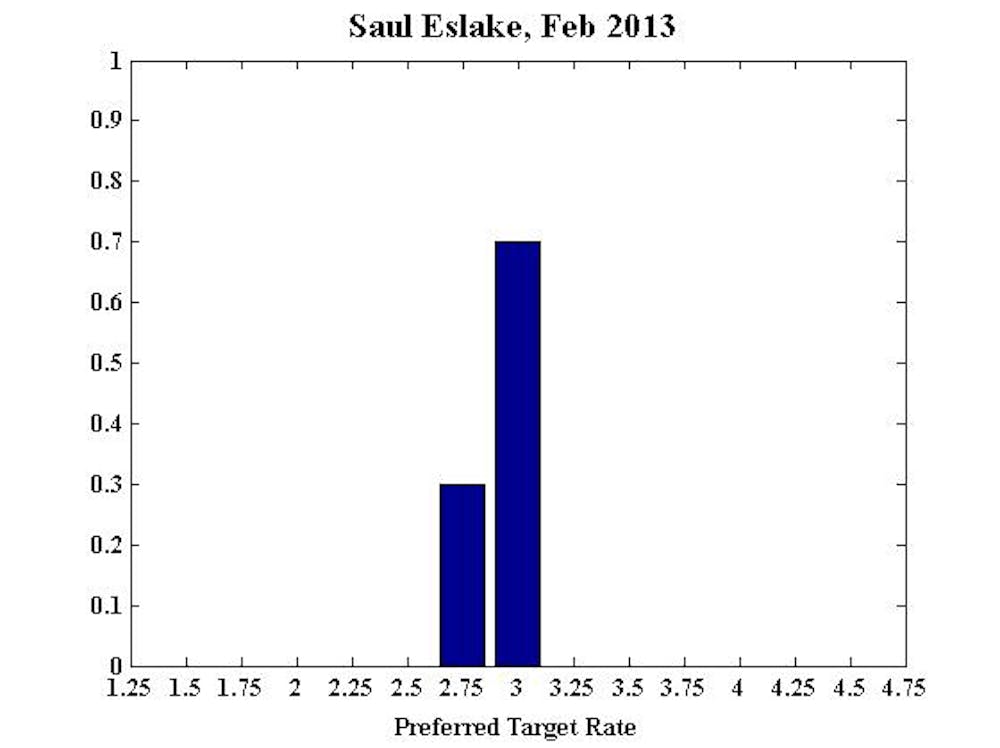

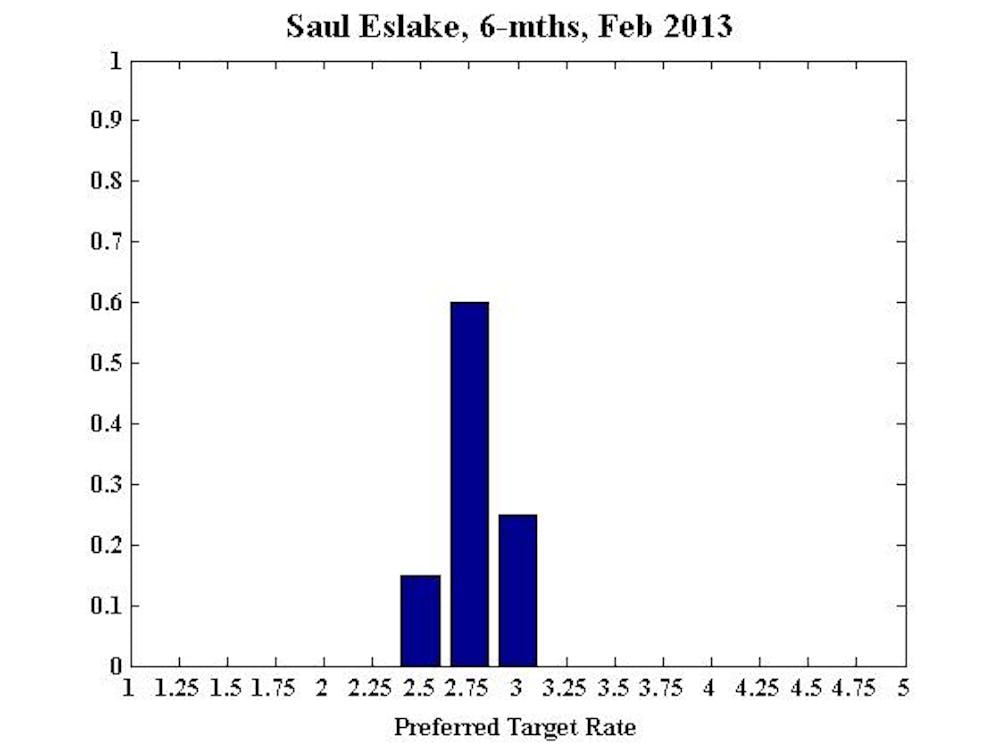

Saul Eslake, Chief Economist, Bank of America Merrill Lynch Australia

Current: Having cut rates in December, and given that February is a short month, the RBA can probably afford to wait for more information as to the condition of the economy at the end of 2012 and the beginning of 2013 before deciding on their next move.

The international climate appears to have improved since the December meeting: commodity prices are higher, the US avoided going over the “fiscal cliff” (albeit that the New Year’s Eve “deal” nonetheless embodies a significant amount of fiscal tightening), “tail risks” in Europe appear to have diminished, and the Chinese economy is picking up. Against that, the Australian dollar is still “uncomfortably high”, and there have been a number of major layoff announcements which along with other indicators of softness in hiring intentions signals a rise in unemployment in the months ahead.

Six-months: Persistent strength in the exchange rate and rising unemployment warrant rates being lower than present levels by June.

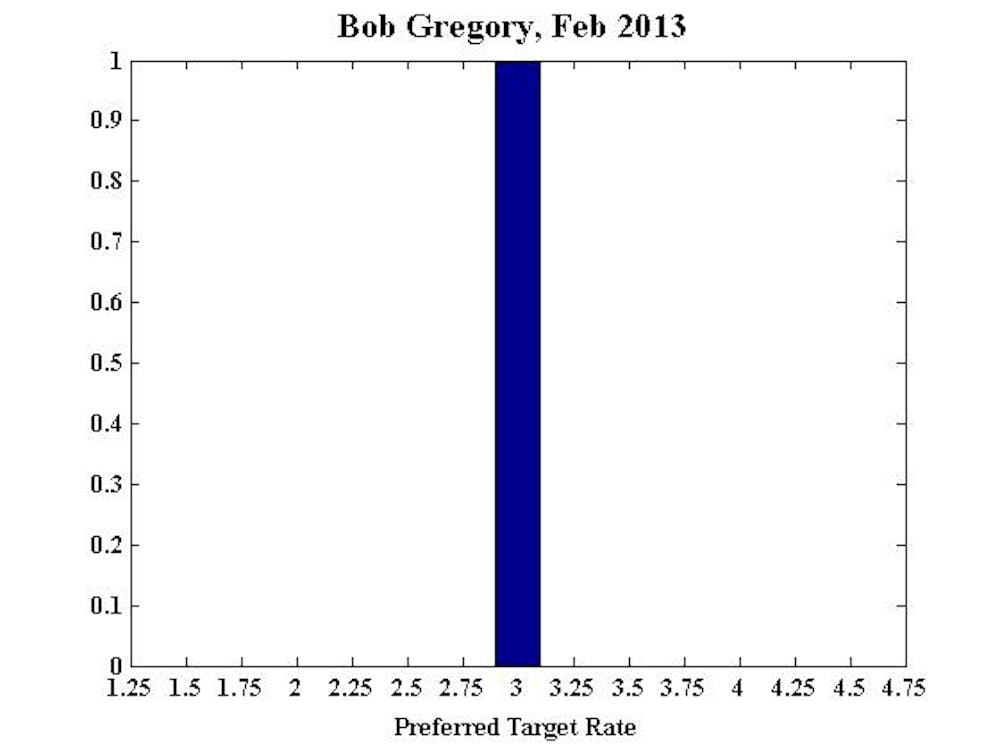

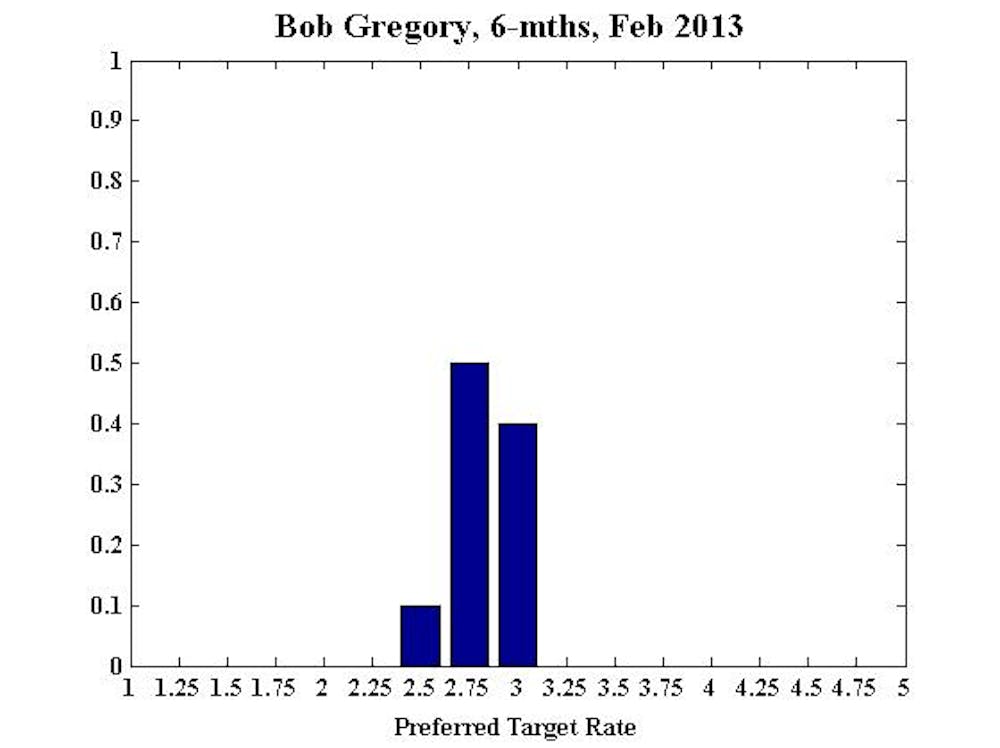

Bob Gregory, Professor Emeritus, RSE, ANU, Professorial Fellow, Centre for Strategic Economic Studies, Victoria University, Adjunct Professor, School of Economics & Finance, Queensland University of Technology

No comment.

Warwick McKibbin, Chair in Public Policy in the ANU Centre for Applied Macroeconomic Analysis (CAMA) in the Crawford School of Public Policy at the Australian National University

There are two main reasons why interest rates should not be reduced any further and should probably rise over the year. First, moving interest rates below 3% during a global shift in portfolio preference towards Australia will not result in the usual stimulus to the Australian economy because the exchange rate channel is being diminished through external forces.

The task of adapting to the changing nature of the commodities boom should be a combination of increased flexibility in the economy, particularly labor markets, to allow the private sector to adjust and a gearing up of government infrastructure spending at historically low costs of borrowing in order to facilitate private sector investments to emerge over time.

Monetary policy is not the correct instrument for a structural adjustment and excessively low interest rates risk distorting the allocation of capital towards more speculative investments that eventually cause a problem during an unwinding of the policy.

Second, it is important to keep in mind that the appropriate nominal interest rate for an economy with low inflation and low unemployment is thought by many to be the nominal growth rates plus a few percent, interest rates are already too low in the Australian economy given the aggregate economic outcomes with nominal growth at least at 5%. Current interest rates are well below this rule of thumb.

There are real risks in the global economy. The largest is Europe followed by a crisis in global bond markets as major central banks unwind their quantitative easy policies that have highly distorted bond rates to a point that has caused asset price bubbles to sprout in emerging market economies that are adopting the monetary policies of the core economies.

Monetary policy in Australia should be focused on what is happening now and in this country and be ready to respond if needed when the next crisis occurs.

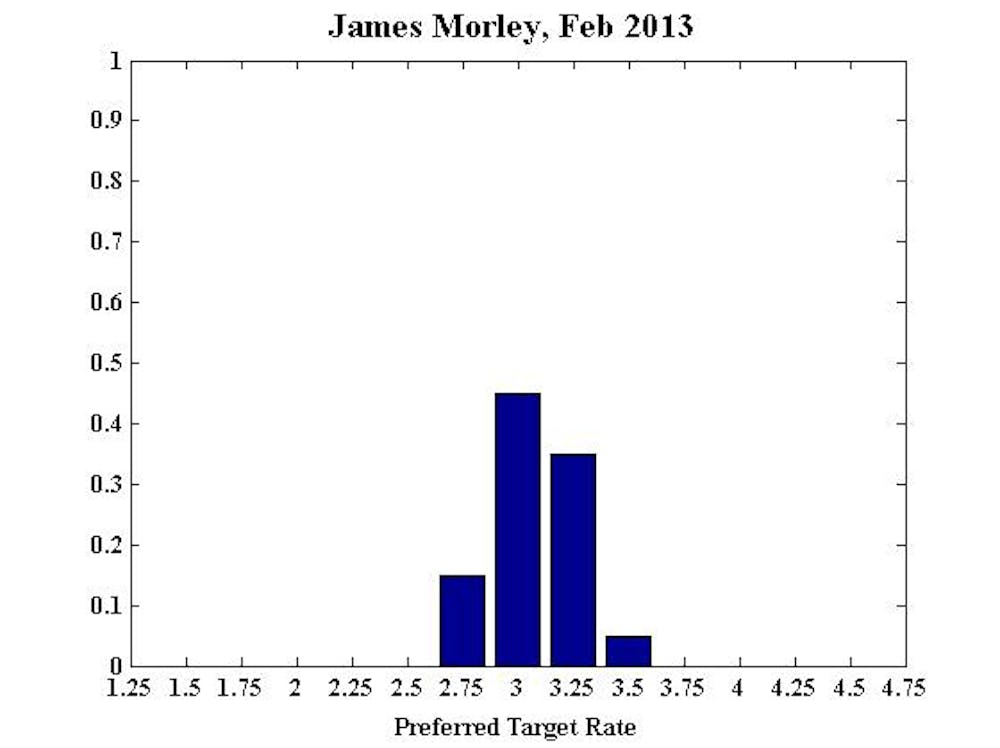

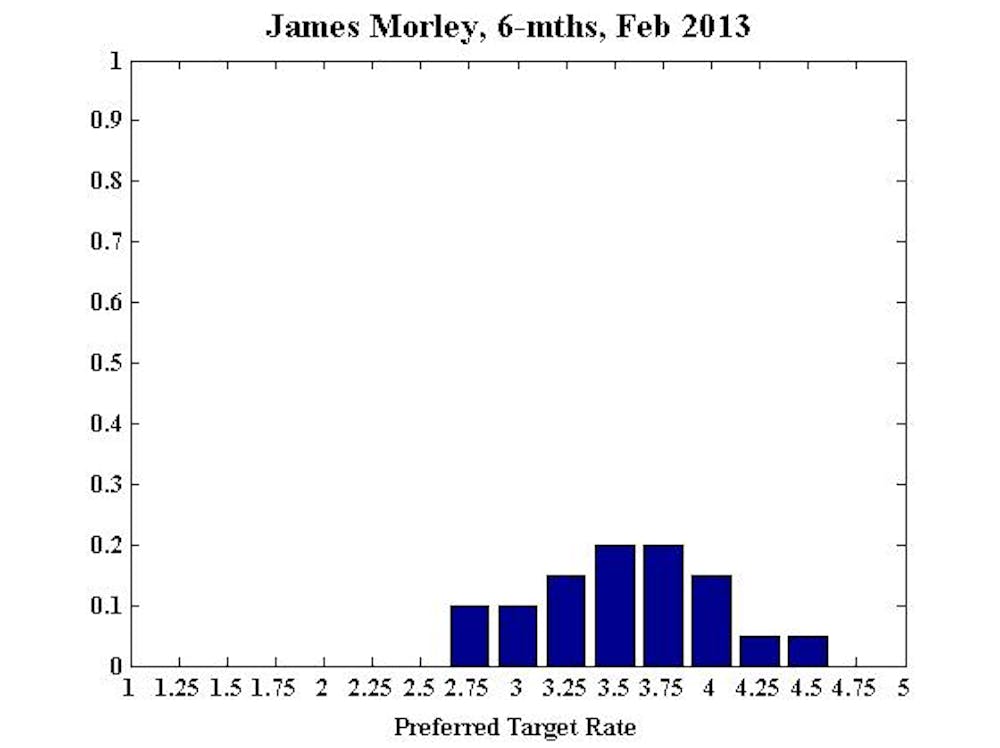

James Morley, Professor, University of New South Wales, CAMA:

Conditions balanced, policy accommodative: The unemployment rate is still reasonably low at 5.4% and inflation is in the middle of the target range of 2-3%. Thus, there is no strong impetus for an immediate change in the policy rate in either direction. However, policy is quite accommodative and policymakers will have to start thinking about returning policy to neutral over the medium term.

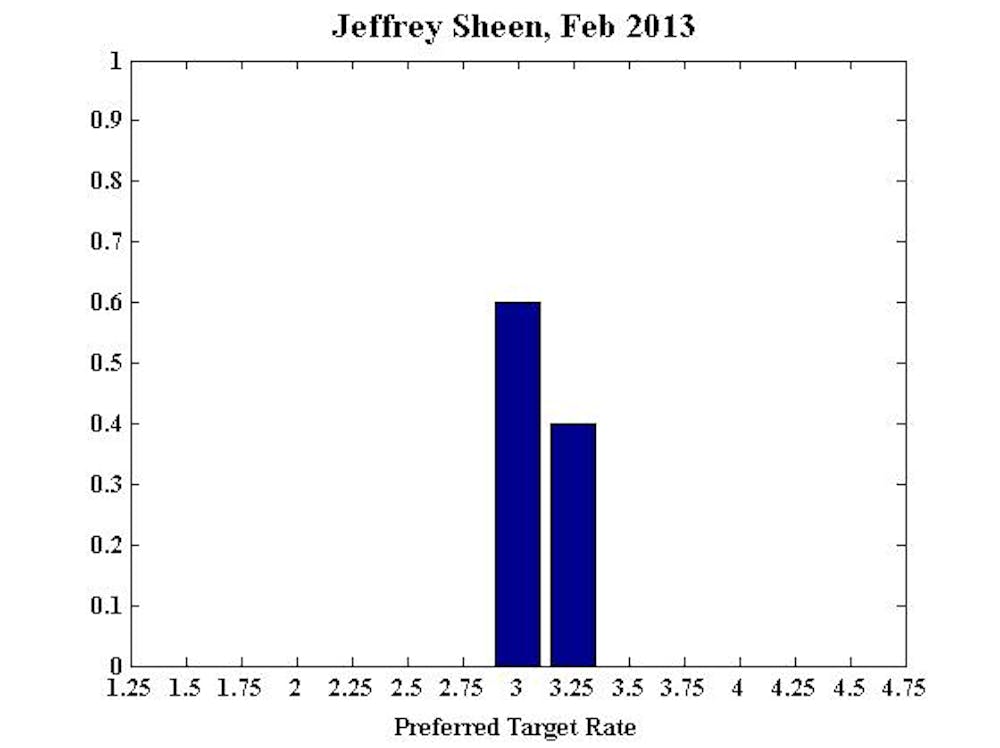

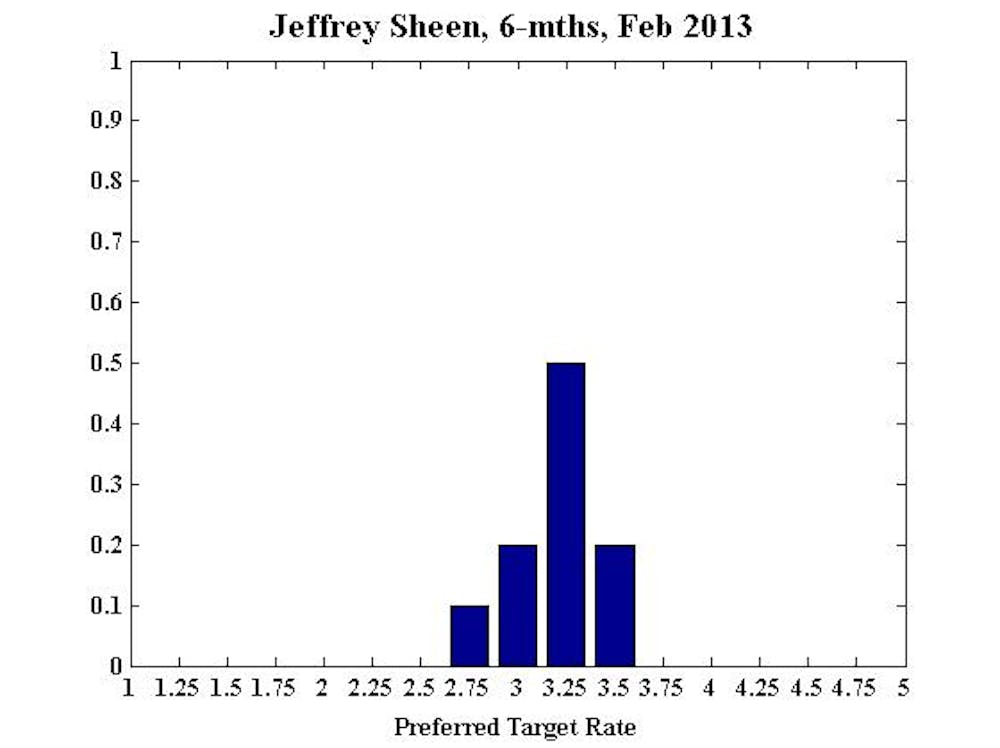

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

The cash rate was cut four times in 2012, mostly based on the possible implications of various uncertainties such as the euro area crisis, the US fiscal cliff, the Chinese slowdown, and the Australian government’s planned fiscal consolidation.

All of these problems would appear to have eased, if not fully resolved. Meantime inflation is well within the target band, output growth is close to normal (though slowing a little), unemployment has risen a small amount though the unemployment gap is probably steady, hours worked is also steady, there are signs of improvement in productivity, and share and house prices have begun to strengthen.

All of this does not provide a case for further fine-tuning cuts in the cash rate now, which is at a 30-year low. Any cuts may feed unnecessary pessimism about the Australian economy.

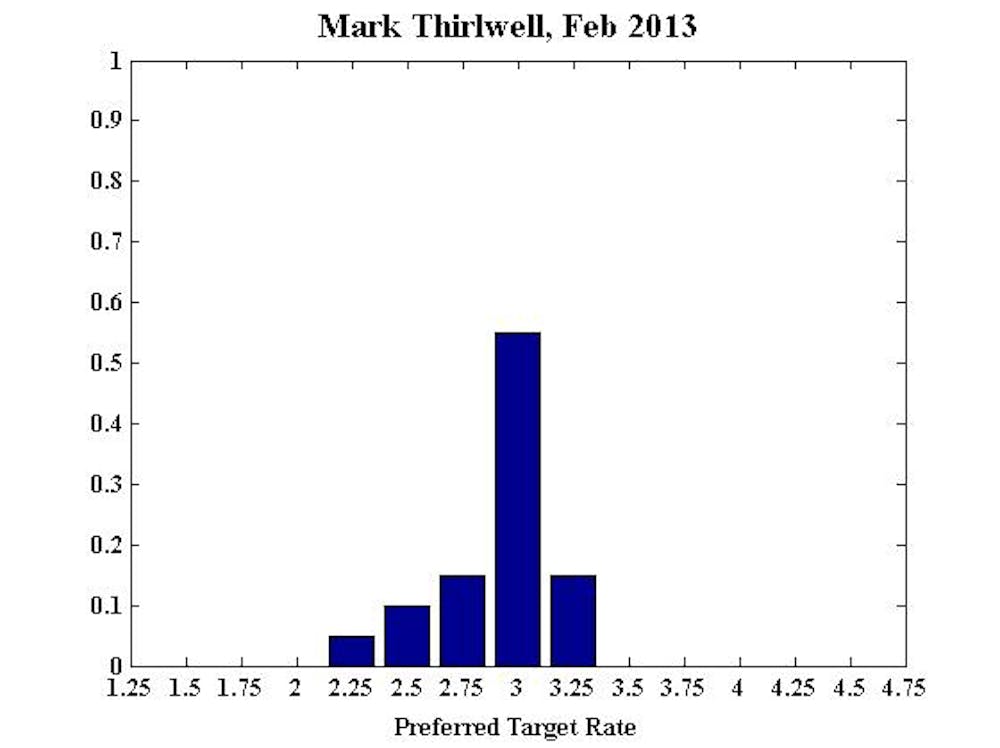

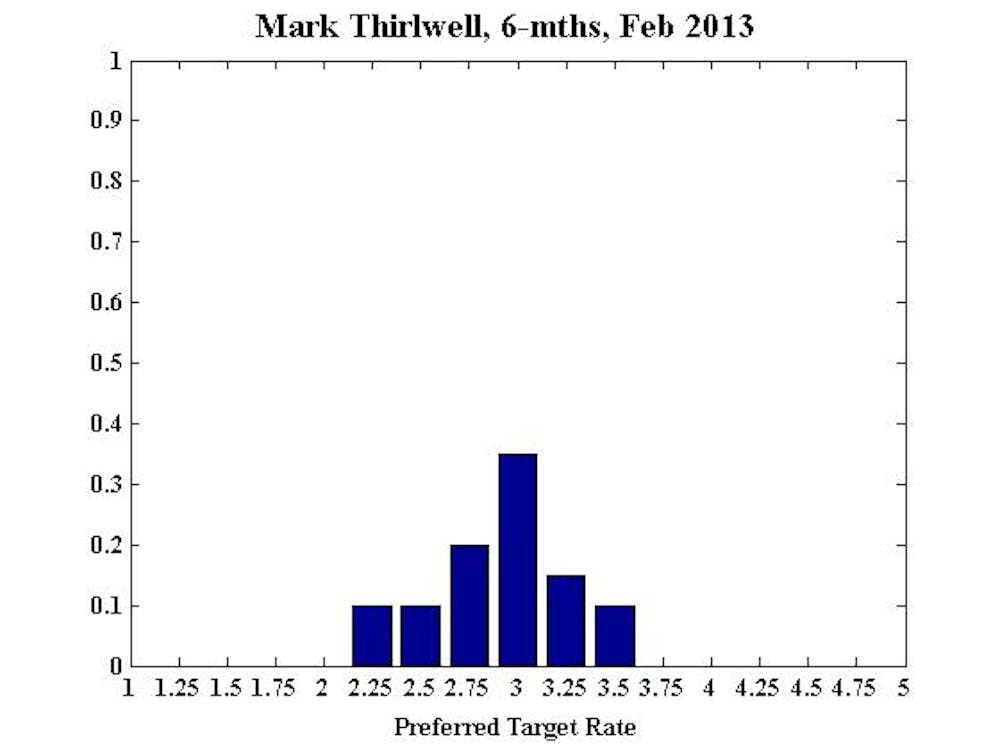

Mark Thirlwell, Director, International Economy Program, Lowy Institute for International Policy

No comment.