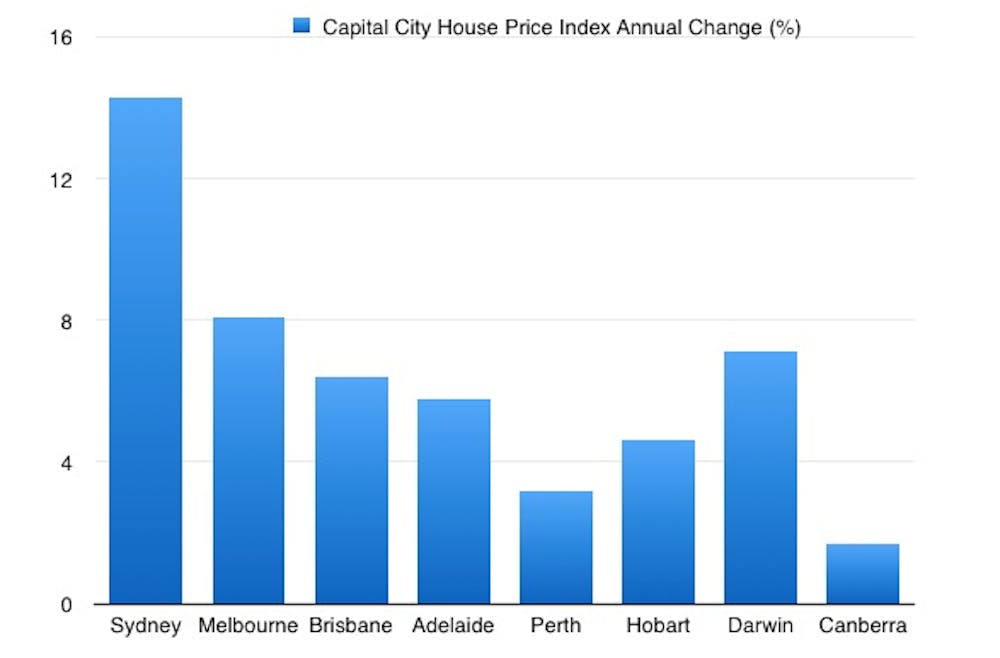

The latest house price index figures released by RP Data earlier this week show a year-on-year increase in property values in Sydney of 14.3%. This has sparked the current hot debate on property prices and speculation of a price bubble. Though, it seems many people have forgotten what house price indices represent.

The All Ordinaries, the index of broad Australian equities market movements, increased by around 9% in the 12 months to the start of September. As investors understand, this doesn’t equate to all stocks on the market increasing in price by 9% over that period.

For example, shareholders in BHP, one of the largest ASX companies by market capitalisation, have suffered a modest loss over that period, even after dividend payments are considered. And as the All Ordinaries Index value has fallen 6% over the past month, there have been some stocks that have fallen more (Myer shares tumbled nearly 20% in the month) and others that have gone against the trend (insurer QBE was up 1.2% in September).

Similarly, a house price index gives a measure of the broad property market movement. In the case of the RP Data-Rismark Index, the change in the index value reflects the average increase or decrease in property prices.

Prices in Australian capital cities, the typical benchmark measure of the Australian residential real estate market, increased by 9.3% in the year to September.

In Canberra and Perth, however, the reported growth in real estate prices was significantly lower at 3.2% and 1.7% respectively. Outside of capital cities property price growth was also a modest 3.3%.

Even in Sydney, which has experienced the strongest price growth of any capital city, there are marked differences in the rate of price appreciation between different suburbs. Western Sydney clearly captures this with residents in South Granville enjoying an increase in median property price of around 17.5%, while reported median prices have shown virtually no annual change in Auburn.

Blunt policy tools are not the answer

It wasn’t so long ago that the average price of Perth’s houses surpassed Sydney’s on the back of a mining industry-led boom in the West. At the national level, these differences in property price growth are the result of shifting labour and economic factors, and to a lesser extent state-specific regulation.

Within a city, local amenities and employment, as well as the preferences of the potential home buyers are reflected in price growth variation.

This is a key point that needs to be remembered when blunt policy tools are debated. Measures to tighten home loan lending, increase borrowing costs or remove negative gearing affect the market as a whole, whether in Sydney, Perth, or a regional centre.

For policy to be effective it needs to firstly identify what it aims to achieve. Housing policy is a double-edged sword. Rapidly rising house prices can put home ownership beyond the reach of younger and lower-income Australians. But policy designed to lower house prices can put existing homeowners at risk of falling “underwater” - holding negative equity in their property. Again, it is typically lower-income households that are most at risk in this scenario.

Cooling the bubble talk

The growing pressure for a policy response to rising house prices is in part due to fears of a price bubble. The last time the Australian or Sydney house price index increased at more than 10% in a year was 2009. Unsurprisingly, there were calls then too that increased regulation was required to prevent a property bubble burst and housing crisis.

Since 1996, Sydney real estate prices have grown at an average annual rate of 7.26% though, with considerable variation in that time. A growth rate in a single year of 10% in any other asset market with these dynamics would not be cause for alarm. Yet housing has this perception of being low risk, pervading our cultural psyche. Something idiomatically described as “safe as houses” is viewed as guaranteed or risk-free.

When faced with the reality that property prices go up and down, sometimes fast and sometimes slow, we seek ways to explain the conflict with these cultural expectations. Assigning the label or “price bubble” shifts the responsibility for our own irrationalities back on the market.