Russia’s targeting of $A400 million of Australian food exports and the government’s muddled response are just the latest setback for a sector struggling under failed policy approaches.

Agriculture is Australia’s only “strongly competitive industry”, according to recent reports from consulting firm McKinsey and the Business Council of Australia (BCA). Yet, the industry is today characterised by high levels of debt, low farm income, depleted reserves, increasing levels of insolvency and rising poverty. Why the mismatch?

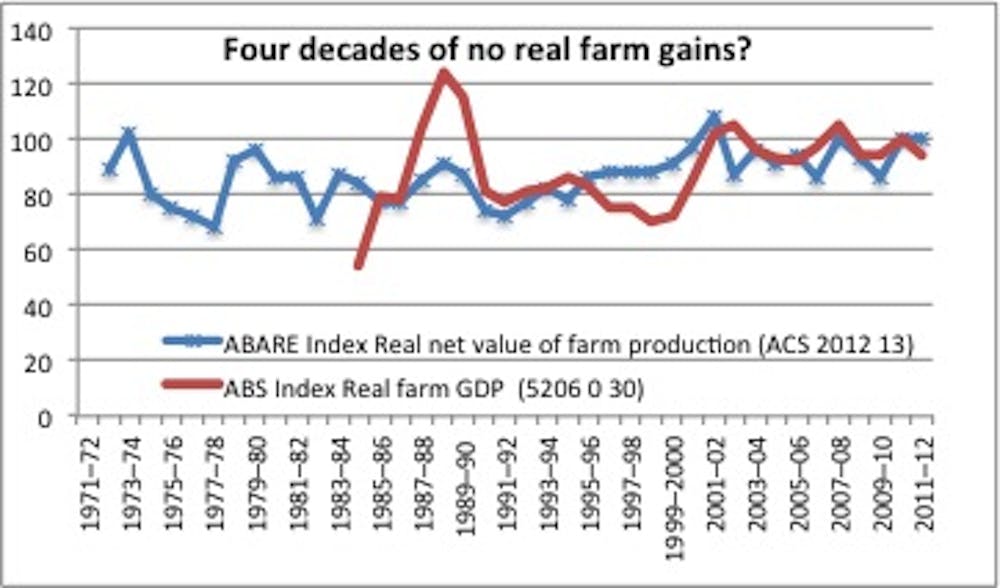

Productivity is high in agriculture. Indeed productivity performance has been outstanding. Yet profits and incomes have been miserable for years. To top it off ABARE reports current Queensland farm incomes as the lowest for 37 years (which is when their figures began).

We’re measuring the wrong things

Measures of both competitiveness and productivity can increase when an industry is in decline. Today, agriculture is not where we hoped it would be. Existing policies and thinking have not delivered gains for agriculture in real terms (as evident in the graph) or Australia (as rising net overseas obligations demonstrate). Continuing them is folly.

Disappointingly, this failed stance sits behind the “new” veneer in the BCA’s “Building Australia’s Comparative Advantage”. Under its dated take on comparative advantage, economies of scale still rule. The productivity mantra is repeated regularly but profit is never mentioned by the BCA, and incidentally mentioned only twice by McKinsey. Yet profit and sustainable incomes lie at the heart of sound business and investment servicing.

It’s 1997 thinking. Then, Minister for Primary Industries John Anderson convened a Rural Finance Summit in Canberra. The thrust was similar. Scale was the saviour and the message was that over a quarter of farmers must go. We overachieved - more than 40% or 103,000 farmers went during the Howard-Anderson era.

The reality is economies of scale require enterprises to increase operational size, utilise the latest technology (such as limited till farming and GPS navigation), employ advanced managerial systems and so on. Increased farm size requires larger machinery and equipment to replace labour intensive farming. All this takes money, yet financial considerations have been essentially absent.

Farm sector reforms have now created a sector with 20% of farmers producing around 80% of output from an increasingly untenable financial basis. Aggregation costs were neglected.

As asset inflation was thought never to end, debt-to-equity loans were not designed to be repaid from income. Capital gains would pick up any shortfall. But as stresses built and the GFC unfolded with pervasive capital losses, the economies of scale arguments and poor lending collapsed. Untenable loan-to-valuation ratios ushered in a financial crisis in national food production.

Large highly mechanised “efficient” enterprises were suddenly expected to repay multi-million dollar debts from insufficient income. Foreign buyers acquired most significant Australian food manufacturers and many farms.

What next?

Untenable financial arrangements need restructuring. The sector needs recapitalisation, new institutional arrangements and, for a time, a hands-on approach from government.

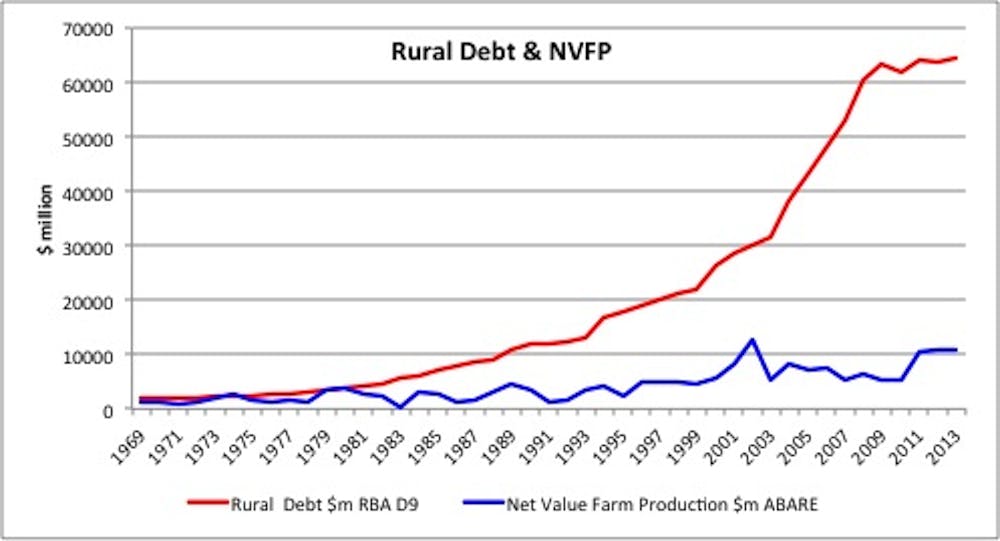

Today, the numbers of bank foreclosures and bankruptcy proceedings challenge the mantra makers. Financial numbers that don’t add up, and often never did, trash empty pseudo-economic rhetoric. Incomes going nowhere will not service the recent debt run up, as is evident in the graph below. Systemic failures allowed this development.

Yet, despite Foreign Minister Julie Bishop stating “the Australian government will do everything in its power to minimise the impact on Australian farmers” of the $400 million disruption from Russia, Agriculture Minister Barnaby Joyce “would hope that we’re able to manage it without direct assistance”. Ongoing “do nothing (but hope)” emptiness is destructive. Why is abject market appeasement still the first preference in Canberra - but not elsewhere?

The real structural reform needed is in industry, governmental and BCA thinking. Scale and competitiveness policies that have failed to deliver need to be discarded, not re-veneered.

Real solutions require substantial considerations of income, investment and profitability under uncertainty. Finance matters as do market and supply chain realities. Policy makers have avoided these things for too long, to the great cost to agriculture, other infected industries and Australia.

Ironically today, the despised low-productivity small farmer with household off-farm employment may be more solvent than the aggregator or the competitive.