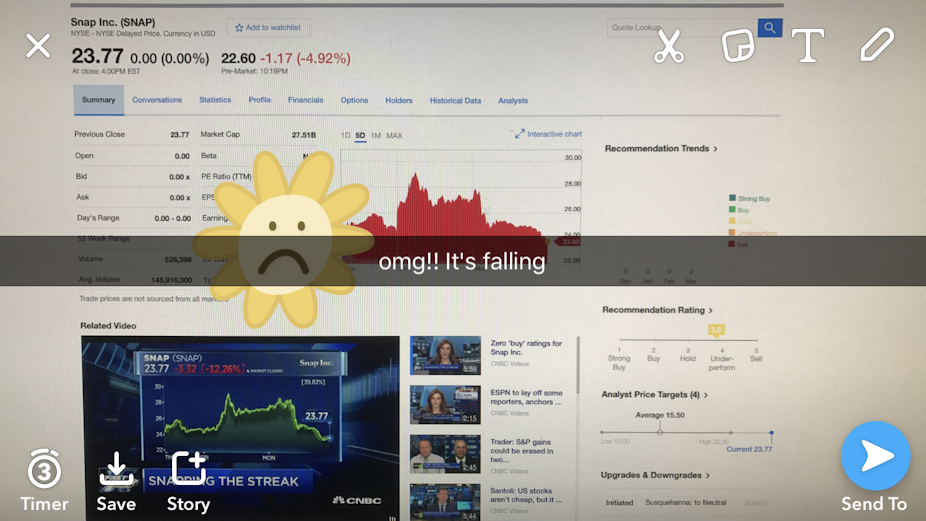

Snapchat’s lofty valuation on the stock market lasted just a little bit longer than one of its user’s disappearing photos. On its third day of trading on the NY Stock Exchange, Snapchat’s parent company Snap’s share price, fell over 12% to below its IPO launch price of US $24 last Thursday. At the time of publication, the price opened a further 9% down at US $21.60.

The reason for the fall was the fact that Wall Street analysts began giving their opinions of the price of Snap shares. Of six companies that began “covering” the stock, 4 rated the shares a “sell”, with the other 2 rating it a hold. Needham analyst Laura Martin was particularly forthright in declaring it overpriced and buying it as being the same as buying a lottery ticket.

It could have been possible that Snap would have lasted at least until it needed to report its first quarter of earnings before the market started looking at the company more realistically than was reflected by a hugely over-inflated debut on the stock market. The movements now simply show that original investors are the main group to have achieved what they set out to do which is to capitalise and cash out their initial investments, estimated at US $1 billion for the founders and initial investors.

The other group of investors who stood to gain from the hype were those investors who decided to “short sell” the stock. Short selling, or shorting, a stock involves an investor selling a stock that they don’t own, usually by borrowing it at a price. They are betting on the stock price dropping at which point they buy the stock to “cover” the original sale.

With an IPO, borrowing shares is harder and more expensive but is certainly possible. It has been estimated that up to a US $1 billion of Snap stock may have been shorted right from the start of the IPO.

Laura Martin’s assessment of Snap’s share’s being a lottery ticket was accurate. The value of the company has no bearing on its current performance and one has to delve into the realms of fantasy to believe it is going to somehow take significant advertising market share from Facebook or Google. But essentially that is what Snap’s founders and investment advisers told investors to do. If you didn’t understand Snap’s potential it was because you were too old to get what young people saw in the platform.

Companies’ shares are usually priced as a multiple of their earnings. When Snap’s shares hit US $27 it meant the company was valued at 34 times the US $1 billion it is predicted to earn in 2017. Facebook by comparison is valued at around 10 times its sales.

There are a range of other indicators that suggest on the basis of historic performance of other companies are acting against Snap succeeding. Snap controversially decided to not allow people buying shares to have voting rights in the company. Having a say in how the company is run would remain solely with the founders and some initial investors. The data shows that companies that used this approach to share ownership performed significantly worse than companies that didn’t. This practice has even drawn recommendations that Snap should not be included in indices of public companies like the S&P Index.

For Snap, the share price is actually not so much of an issue in the short term because it achieved the objective of raising US $2.5 billion in cash from its IPO. At some point the share price will reflect the real performance of the company and that will be more of the issue. If it fails to grow its market and revenues, or even make a profit, it will eventually languish like Fitbit, Twitter, Groupon, Zynga and Twilio, to name but a few.