The international community’s ambition to fight against climate change comes at a cost: between US$50,000 billion and US$90,000 billion over the next 15 years according to the bottom-end estimates of economist Adair Turner, and the top-end figures from economists at the Global Commission on the Economy and Climate and its New Climate Economy project. By comparison, annual world GDP totals nearly US$80,000 billion.

The 2016 New Climate Economy report indicates that, each year, US$2,000 billion will be needed for the global North and US$4,000 billion for the global South to finance the green infrastructure that would help move us closer to a carbon-neutral world early enough to limit global warming to no more than +2°C above the pre-industrial levels.

So can the private sector cope with this level of spending?

What pace for the energy transition?

According to the World Bank, private debt, excluding financial institutions, now totals US$110,000 billion, equivalent to 138% of world GDP. Added to this is public debt bordering on US$60,000 billion, or around 75% of GDP.

Yet, as Bank of England Governor Mark Carney underlined in a now-famous speech, an over-hasty transition to a low-carbon economy could jeopardise financial stability. On the other hand, if the transition is too sluggish, we may run the risk of overshooting the irreversible ecological thresholds (especially for soil erosion).

So, at what speed do the private and public sectors need to move ahead?

In a May 2018 paper, published in the journal Ecological Economics focussing on the GEMMES (General Monetary and Multisectoral Macrodynamics for the Ecological Shift) model, we offer fresh insights into the kind of compromises needed to meet the Paris Agreement goals.

The GEMMES model functions at a planetary scale and combines a financial dynamic, projections for climate disturbances, and the United Nations median demographic scenario (9 billion people in 2050). As with any foresight modelling tool, our figures are only indicative given the still huge uncertainty on how the environment and the economy interact.

The risk of economic collapse is there

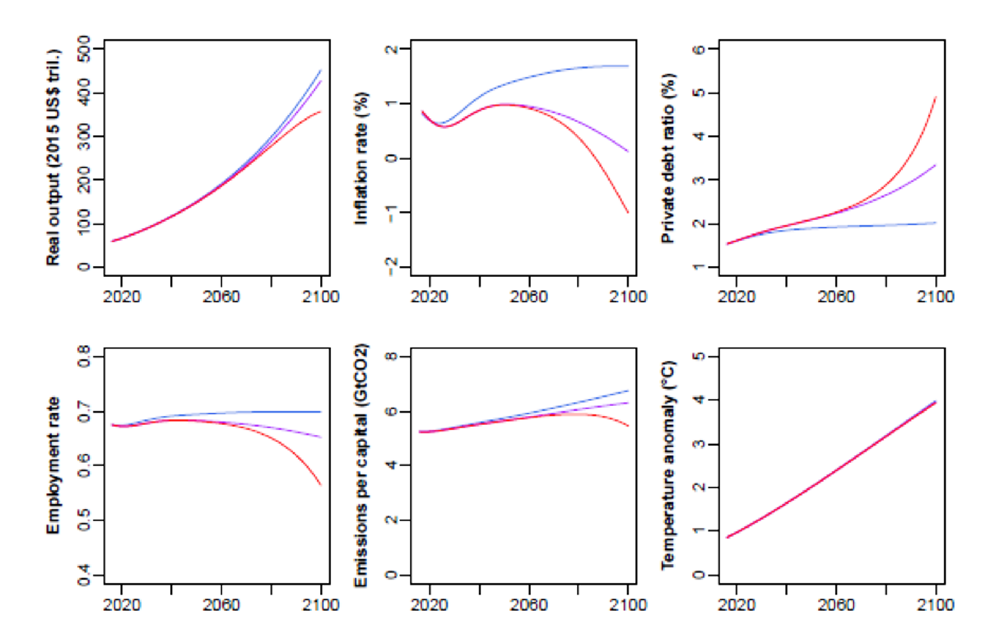

In the “laissez-faire” scenario, where no additional public policy kicks in to encourage the productive sector to accelerate its investment in green infrastructure, we see a global warming of nearly +4°C in 2100. The +2°C threshold is crossed as early as 2050 as no emissions abatement efforts are pursued.

The damages brought on by this warming cause accelerating capital depreciation and a slowdown in economic activity.

According to the consultancy firm, Carbone 4, 2017 is already a record year: the costs of weather-related disasters have never been so high. Those that could be estimated topped US$400 billion. A significant share of these costs is covered by the insurance industry, with a US$135 billion pay-out according to the German reinsurer Munich Re.

Our GEMMES simulations show that the reduction in economic activity linked to both climate and investment in mitigation technologies is reflected in weaker growth, fewer jobs and an increase in private debt.

Given the margins of uncertainty when it comes to quantifying the economic impact of global warming, we tested several hypotheses for the expected extent of damages.

Taking the most pessimistic hypotheses – generally viewed as the most realistic by climatologists – we even observe scenarios of economic collapses absent any proactive public intervention. These are similar to the scenarios that emerged in the foresight analysis, built on reasons other than global warming, by Donald Meadows’ team for their 1972 report to the Club of Rome.

Carbon pricing is not a cure-all

So how can we avoid such a catastrophic scenario?

Carbon pricing could send the productive sector a price signal to spur investment that would help reduce the carbon intensity of the economy. On this count, one thing appears certain: if industry fails to deploy parallel efforts on carbon sequestration, carbon pricing – at whatever level – will not keep the planet under the 2°C threshold.

Without negative emissions, meaning the artificial re-absorption of greenhouse gases already emitted into the atmosphere, it is likely already too late to keep the Paris Agreement on track – an opinion widely upheld by the climatologist community. In fact, achieving this objective would require completing the energy transition around the year 2020 with a carbon price in the region of US$540. If the transition were wholly financed by the private sector, this would trigger an economic recession of around -5% of world GDP – which is a tough situation politically speaking. This would be accompanied by a sharp hike in the level of private debt, which would rise to almost +130 percentage points of GDP compared to 2016.

On the other hand, a more measured carbon-price trajectory in the short run, in the vicinity of US$100 in 2040 rising to around US$450 in the 2050s, would certainly safeguard the global economy against excessive forced degrowth during the transition. However, it would also push up global warming to around+3°C by the end of the century, and entail some consequences that are partly incalculable.

What’s more, this trajectory would not do away with a still hefty level of private debt, since it advocates proactive public policies such as subsidies for green investment as recommended in the Stern-Stiglitz Commission’s report on carbon prices.

The choice between GDP growth and the fight against global warming

The temporary trade-offs between GDP growth and the fight against global warming reappear in all of our scenarios. This is visible, for instance, in the figure below showing a median hypothesis of the severity of weather-related damages: each pair of parameters (a, b) corresponds to a carbon price trajectory, where parameter (a) drives the long-run increase of the carbon price and parameter (b) reflects the intensity of the short-run increase (at the start of the simulation) of the carbon price.

Parameters (a) and (b) should be chosen so as to keep as close as possible to the +2°C, i.e. in the area closest to the dark green in the top right corner of the left-hand panel. Unfortunately, this is also the red-grey area in the right-hand panel, which indicates a forced degrowth of the world economy during the energy transition.

Here, the dilemma pointed up by Mark Carney is illustrated by the need to implement a carbon trajectory that will keep the economy in the yellow area of the left-hand panel, which corresponds to a temperature increase of between +2°C et +2.5°C.

However fast we transition to a carbon-neutral world, these graphs show that trade-offs between growth and climate change have to be made during the energy transition.

Keep in mind, however, that productivity gains, like job creation in the renewable energy sectors and the circular economy (recycling, repair, rental), are to be expected from this transformation, and could temper these trade-offs.

Warding off deflation, promoting “green” public spending

In all of the cases studied, the world economy turns out to be more resilient to global warming if there is less private debt, less unemployment and a higher share of wages in GDP.

The latter finding suggests that the debate on the distribution of value-added between capital and labour is not disconnected from the climate issue. As far as we know, the mechanism underlying this finding is new. In fact, climate disruption seems to push the world economy toward deflation, in line with a well-known macroeconomic pattern: stagnation brings about a decrease in prices and real GDP, which leads to a rise in under-employment and debt, then to an erosion of the share of wages in national income. In our analysis, a redistribution policy favouring labour income seems a natural response to this deflationary spiral, and thus to the impact of global warming.

The final lesson from our simulations: if public financing contributes to some of the green investment expenditure, carbon pricing in the spirit of the Stern-Stiglitz report (with a price corridor centred around US$44 per tonne in 2020, US$140 in 2030 and US$300 in 2040) would not only enable us to remain close to +2.5°C by the end of the century, but also avoid the slippery slope of deflation.

With no additional public spending, on the other hand, this macro-climatic trajectory seems already out of reach: carbon pricing certainly provides the private sector with an incentive to finance the green infrastructure we need, but it does not lighten the burden of the corresponding private debt. Were the State to bear of this burden, even partly, this would of course be to the detriment of public finances. But, as we have seen, their situation is currently less degraded than that of the private sector.

To boot, should deflation threaten, public debt is not necessarily the problem and may actually be part of the solution. By combating both the macro-financial impact of global warming and its anthropogenic causes, a public contribution to financing the transition would achieve both objectives in one fell swoop.