With the recent re-approval of Adani’s Carmichael coal mine in Queensland, debate over the future of coal has reached fever pitch again. Green groups have argued that Australia should account for the climate impacts of burning coal produced in the country.

Meanwhile, the government has once again come out in support of coal to provide cheap power to developing nations.

It can be hard to make sense of the different sides. In a paper recently published in Energy Research and Social Science, I looked at the long-term future for coal in Australia. My research suggests the current coal woes are just the beginning.

Australia’s failure to reassess its commitment to coal will have serious negative consequences, not only for Australia’s economy, but for the health and well being of millions of people and the global environment.

Boom and bust

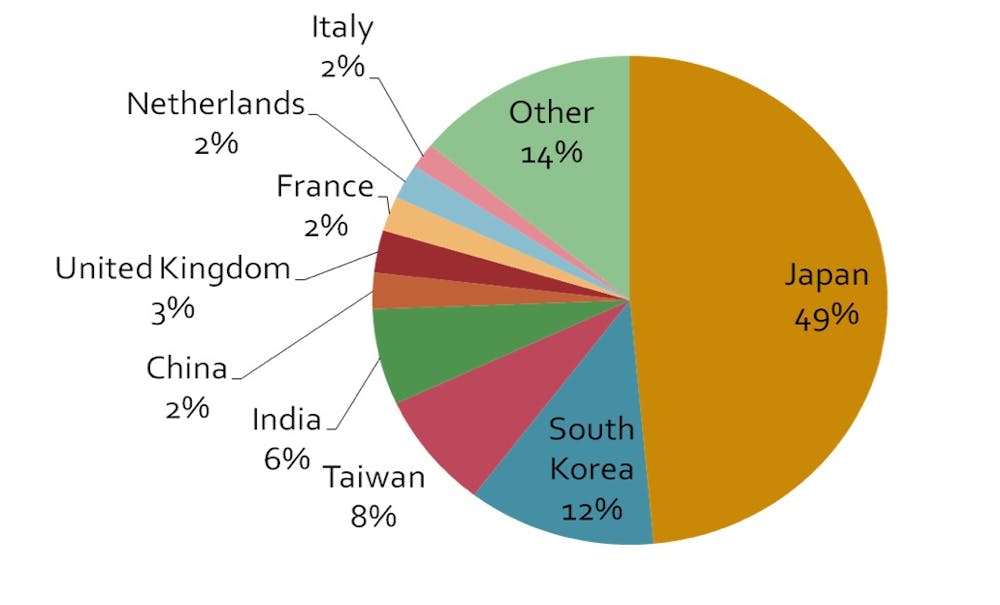

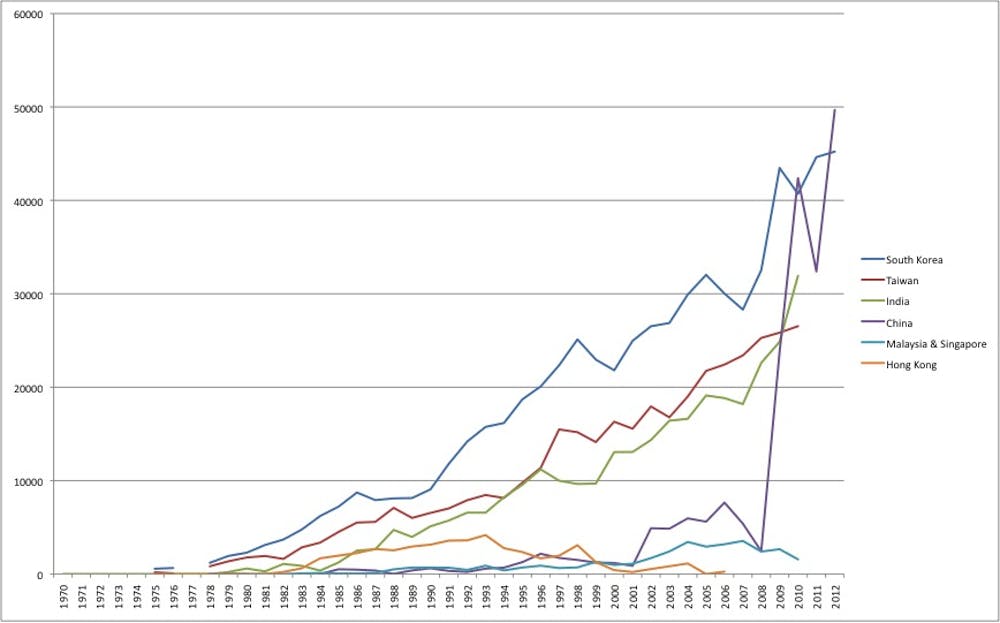

The Australian coal industry has been on an inexorable and seemingly unstoppable upswing since it first began to export coal to East Asia in the late 1950s. Between 1970 and 2010 it provided three-quarters of its coal exports by volume to Japan, South Korea, Taiwan and India.

It remained confident until very recently that it could expand even more quickly than it had in earlier decades as the Asian “tiger economies” continued to grow, and demand from China and India surged.

By the end of 2012, at the peak of the recent mining boom, the industry had announced plans to triple or even quadruple Australian black coal production on 2010 levels by 2030. Less than three years after many of these announcements were made, however, a number of the relevant projects have become financially unviable, such as the Wiggins Island, Balaclava Island and Dudgeon Point coal terminals and the Wandoan coal mine in Queensland.

Several prominent energy analysts have warned that those that remain face the prospect of becoming stranded assets, risking tens of billions of dollars of investor capital.

The industry’s plans to triple 2010 production levels by 2030 were almost certainly premised on its awareness that global coal production would most likely peak by the end of next decade, enabling Australia to “fill the gap” in global coal supply post-2030 by exploiting its huge untapped coal resources in Queensland.

Climate change and renewables

Then a few weeks ago major multinational mining companies such as Glencore, BHP Billiton and Rio Tinto, all of which have substantial coal interests, suffered a radical reduction in share prices. This clearly reflects a growing awareness in the international financial community that the continued expansion of the Australian coal industry faces a number of structural obstacles.

These include decreased international demand, lower coal prices, carbon risk, and competition from renewables and other coal-exporting nations.

Arguably, the combined impact of these factors has not been adequately grasped by some coal industry analysts, who continue to remain cautiously optimistic about Australian coal’s long-term prospects.

There appear to be two key factors in the declining market fortunes of coal: the growing recognition that mining and burning coal is one of the main contributors to climate change, and the rapid decline in the costs of renewable energy relative to new coal and gas plants.

While the first issue is arguably the most important from an existential and equity perspective, it is the second issue which has largely focused the minds of governments, energy companies and the financial community in recent months. Perhaps unsurprisingly, altruistic concerns about the environmental and social costs of climate change continue to be trumped by economic calculations about the relative costs of different energy sources.

It is nevertheless apparent that defenders of a fossil fuel future, or business-as-usual, continue to seriously underestimate the extent to which the reliability of renewable energy technology has improved, its costs have decreased, and it has won market share in many developed and developing countries.

For example, the price at which solar power developers in India are currently pitching new projects is already cheaper than the cost of providing new coal-fired power from imported coal. The much-vaunted interest of the Indian conglomerate, the Adani Group, in exploiting the rich coal resources of the Galilee Basin, appears to be foundering. After more than a dozen major international financial institutions have declined to invest in Adani’s Carmichael coal project, it has recently begun to turn its attention to solar projects in India and Australia.

Although there have been signs over the last few years of a decline in coal demand from some of Australia’s biggest customers, the industry and its political supporters appear to have convinced themselves that Chinese and Indian demand for Australian coal would continue to grow.

This ignores the fact that there has been a significant reduction in Chinese coal imports and consumption more generally over the last few years. Recent signals from India suggest that it, too, is seriously reconsidering its role in coal-led energy growth, anticipating a 20% annual decline in coal imports, beginning this year.

Unburnable coal

If humanity wants to maintain the stable climatic conditions of the past million years of Earth’s history, the world’s leading climate scientists have told us that most of the world’s remaining coal resources will have to remain in the ground for the foreseeable future, and therefore constitute “unburnable carbon”.

The greenhouse gas emissions from burning Australia’s coal overseas have exceeded those from Australia’s domestic emissions for more than a decade now, and its remaining demonstrated black coal resources would contribute 28% of the remaining global carbon budget if burnt. There will almost certainly be growing international pressure on Australia and other fossil-fuel producing nations to extract only a small proportion of those resources over the next few decades.

In the light of these various considerations, one would imagine that the enthusiasm of Australian governments for the ongoing expansion of the Australian coal industry might be on the wane, but there are no clear signs that this is the case. My own research and that of several other Australian scholars such as Chris Riedy, Tom Biegler and the Australia Institute indicates that the combined costs to Australia of subsidies, externalities and foreign ownership outweigh the majority of the economic benefits which the coal industry supposedly provides.

Meanwhile, the major political parties continue to cling to a distorted and largely outdated notion of the industry’s contribution to Australia and the world. The governments of China and India, both of which have substantial coal resources, have clearly recognised the benefits of phasing out the use of fossil fuels in favour of renewables.

The medium- to long-term benefits of embracing such a strategy are very clear. The failure of Australia’s business and political elites to recognise the need for change will cost us dearly.