The western US is burning.

This year’s damaging experience is just the latest in a recent series of devastating wildfire seasons, a trend that will only likely increase over the coming years.

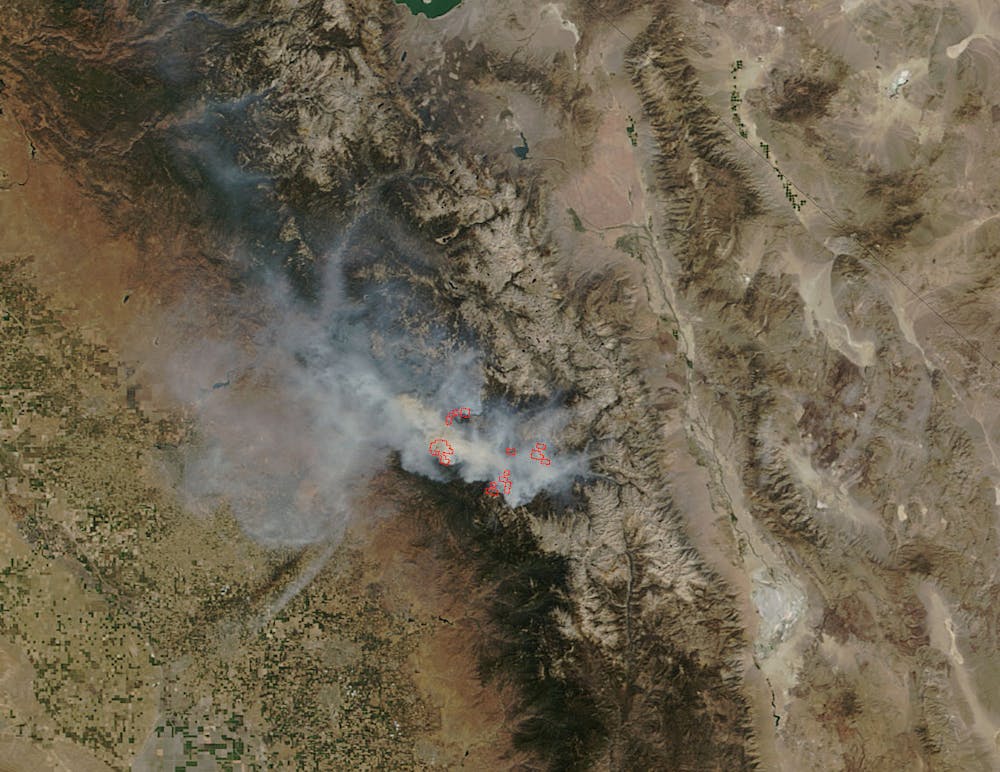

Over the last few decades, and especially since 2000, the wildfire season is getting longer, with more fires, bigger fires and more damaging fires. Even before the end of this year’s season, 600,000 acres have burned in California, and almost a million acres each in Oregon and Washington. More than five million acres were destroyed in the boreal forests of Alaska. We are on track to have the most devastating fire season ever.

More than eight million acres have burned in six of the years since 2000. There are two main reasons behind the growing conflagrations. The first is the legacy of fire suppression polices that snuff out fires as they appear, but leads to the build-up of fuel that is the raw material for larger, more devastating fires.

The second is climate change, which is making the West hotter and drier. The higher temperatures wick away moisture from the trees, making them more combustible. The combination of more combustible material and a hotter, drier climate leads to more fires.

But in contrast to this obvious rise of risk and vulnerability, there are also other forces at work, often ignored in the popular national media. Fires make for great images. The intense media coverage focuses on images of destruction, tales of heroism and narratives of community resiliency. The fires are depicted as malevolent forces emerging from the forest to attack the innocent.

As an academic who studies the environmental stresses on society, I’ve dug into the costs and responses to forest fires. What I’ve found is that discussions on this topic often lack any sense of the social and political context of these fires – and how our policies are worsening the damage and increasing the cost.

Building deeper into the woods

A number of economic practices and social issues are exacerbating our forest fire problems.

The first is the enlargement of what is known as the wildland-urban interface (WUI). More people are building homes in the interface close to the wildlands and forests. Since 1970, there has been a 50% increase in the low-density housing that borders state and federal wildlands. And the majority occurs in areas subject to increasing risk of fire. California has almost five million housing units in the WUI.

Real estate developers are happy to meet the demand for those who can afford and want to live in the semi-wilderness on forested lots. States and local municipalities encourage the process because it boosts the local tax base and generates increased income and new jobs.

So we have more people moving into areas subject to greater risk of fire. But the full costs of these actions are not borne by these local actors. The federal government picks up between one-half and two-thirds of the cost of protecting people and property in the WUI by providing financial and technical assistance to states and volunteer firefighters. In effect, the federal government, the US taxpayer, picks up the tab.

It is classic case of the free rider and a good example of moral hazard. Free riders are those who get something for nothing – in this case the underwriting of fire costs.

While insurers are charging low premiums to property owners living in amenity-rich areas close to the wilderness, developers are cashing in on the demand, and state and local government are pocketing the extra taxes. We are effectively socializing the costs of fires by having the federal government bear much of the fire protection costs. The benefits, meanwhile, occur at the local level for private individuals and developers.

There is also evidence of moral hazard – the pursuit of risky behaviors because someone else carries the cost of the risk. A number of studies show that fire insurance costs are too low and do not reflect the real cost. And while the federal government should protect citizens, should it be underwriting the cost of risky behavior for those who gain from their behaviors?

Perverse incentives

The presence of the direct federal subsidy also reduces the incentive of market forces to undertake fuel reduction, and hence lessen the risk of fire.

Owners want to live in forested environments but do not feel the need to reduce fuel load on their property by cutting down trees, as there is a feeling that fire risk and the costs are covered in large part by the federal government. Would states and municipality allow such development if they had to shoulder a much larger share of the fire costs?

The cost of protecting people and property in the WUI is so expensive it has shifted the priorities of the US Forest Service. So much money is spent on protecting property from megafires that programs for preventing wildfires and for protecting habitats and wildlife are much reduced. In 1990, firefighting accounted for only 13% of the US Forest Service budget; now it eats up more than half.

Paradoxically, the US Forest Service is cutting back on programs that could more effectively deal with the buildup of fuel in the remaining forest. In other words, the costly practice of putting out fires to protect property as the WUI expands makes forest fires more likely. The health and sustainability of our national forest are sacrificed to protect property in the WUI.

Fighting hurricanes?

We are on an unsustainable path as the WUI continues to grow and expand, fuel buildup continues and the climate warms. Dry, tinder-like conditions are the new normal in the West.

What is needed is a complete rethink of the federal underwriting of risk that creates free riders and moral hazards. There are tactical decisions, such as perhaps moving to a hurricane model of disaster relief; that is, tell people to board up and leave rather than assure them that their property will be protected. Property owners in hurricane zones are not assured that someone will risk their lives to “fight” the hurricane. Why should we expect anyone to “fight” the fires?

There are also more strategic decisions needed about creating a national fire risk map, which would allow more transparency into state and local real estate development polices. It would perhaps form the basis for the more rational allocation of federal grants for better land use management practices that minimize the risk of fire with, for example, better building codes and property management practices. Wildfire insurance should not encourage risky behavior and we need to stop underwriting the actions of local actors with federal dollars.

The West is getting drier. The risk of fire is increasing. But the WUI continues to expand. The US taxpayer should not be subsidizing and underwriting such risky behavior.