Intel’s proposed US$30 billion (£23 billion) investment in semiconductor manufacturing capacity across Europe has the potential to significantly boost the continent’s struggling chip industry.

The US giant is poised to invest an initial US$17 billion to build a cutting-edge semiconductor factory (known as a fab) in Germany, along with associated R&D facilities to develop new generations of chips in France, Ireland and Poland. It is also in negotiations with the Italian government to develop a manufacturing facility in that country.

If such proposals come to fruition, the overall investment could top US$80 billion and create over 3,000 high-tech jobs and many more across the digital supply chain. Intel, the relevant national governments and the European Commission argue that these investments will transform Europe’s semiconductor supply chain and make it more competitive. The role of national governments and the European Commission is important to note as Intel’s investment is likely to be underpinned by billions of euros worth of public subsidies.

Chip production has been high on Europe’s agenda as many high-technology companies have been struggling to source chips because the COVID-19 pandemic has disrupted worldwide supplies. Europe’s automotive industry has been particularly hindered as a result. Russia’s invasion of Ukraine has accentuated the problem because the industry relies on both nations for neon, which is vital for the lasers used to cut state-of-the-art chips.

Intel’s investment in new capacity is not going to address these current issues, given that production is not expected to begin until 2027. But it could eventually ease Europe’s dependency on sourcing chips from afar and revitalise the continent’s increasingly uncompetitive operations.

The world market

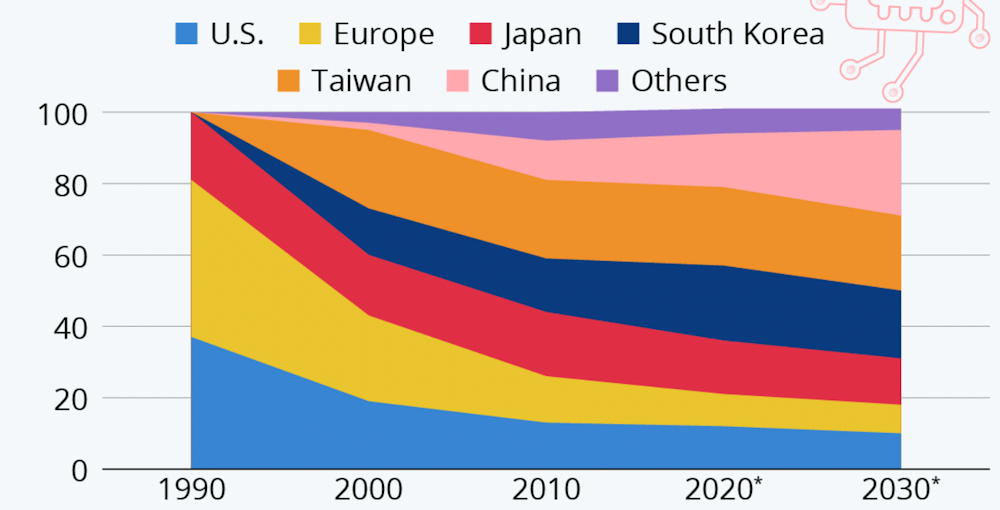

The semiconductor industry is global in scope, with nearly two-thirds of chips manufactured in Asia – particularly South Korea, Taiwan, Japan and China. This dominance has come at the expense of European producers, which now account for only around 8% of the world market, compared to 44% in 1990. This is largely the result of under-investment.

Principally as a result of heightened geopolitical instability, the EU has recently become concerned about “digital sovereignty”. Its recent European Chips Act set out a range of measures to boost European production by pooling different countries’ resources to complement their individual research strengths. It also supports developing new production facilities with a view to increase Europe’s share of the global market to 20% by 2030.

Intel’s announced investment is the most tangible outcome to date and is certainly welcome, though it is unlikely to fully rekindle the European industry alone. The industry tends to be populated by SMEs (smaller businesses) and clustered in a small number of locations, including Leuven (Belgium), Dresden (Germany), Eindhoven (Netherlands), Grenoble (France) and Cardiff (UK).

Our recent research into these clusters suggests that many companies have been starved of investment from either private or public sources to expand and innovate. This is compounded by a lack of demand from European technology companies.

For example, with the demise of Nokia, Europe no longer has a giant company such as Apple or Samsung that demands the most sophisticated chips. For many of Europe’s semiconductor companies, which are engaged in chip design rather than production, these issues are stifling the growth of the industry more than a lack of manufacturing capacity.

What needs to happen

To address this, the Intel intervention needs to form part of a coherent and integrated strategy to boost the competitiveness and innovation capacity of the European sector as a whole. Like other deep tech sectors, the chip industry is increasingly an entrepreneurial one. New and innovative ideas are sparked by start-up companies that are able to commercialise these ideas and create value.

There is a very real need to provide business and infrastructure support, as well as skills development and commercialisation routes to allow start-ups to enter the industry and current incumbents to upgrade and scale up.

Innovation is clearly the name of the game when it comes to competitiveness in chip-making. To give the European Commission its due, it has provided significant funding for semiconductor research over a number of years through the Framework and Horizon programmes. However, successful commercialisable innovations stemming from this research have been relatively sparse.

Therefore, alongside supporting large, foreign direct investment projects there must be an enhanced focus on improving the entrepreneurial and innovative capabilities and capacity across Europe’s semiconductor industry. Without this, there is a real danger that due to a lack of significant viable demand in future, we will be reading news of the mothballing of the proposed new manufacturing facilities.